Key Stats for COST Stock

- Year-to-Date Performance: 16%

- 52-Week Range: $844 to $1,067

- Valuation Model Target Price: $1,192

- Implied Upside: 19%

Value your favorite stocks like Costco Wholesale with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Costco Wholesale Corporation stock is up about 16% year to date, recently trading near $1,003 per share as strong monthly sales results and continued institutional demand supported the rally.

Shares remain near the upper half of their $844 to $1,067 52 week range, reflecting sustained buying momentum rather than a short lived spike.

The stock has advanced this year following stronger January sales results that reinforced confidence in traffic growth and comparable sales momentum.

This week, Costco reported January net sales of $21.33 billion, up 9.3% year over year, with total company comparable sales rising 7.1% and digitally enabled comps surging 34.4%.

U.S. comps increased 5.8%, while traffic rose 2.4% worldwide and 2.2% in the U.S., showing steady demand even as gas price deflation reduced reported comps by about 100 basis points.

CFO Andrew Yoon stated, “net sales for the month came in at $21.33 billion,” highlighting strength across foods, fresh categories, and low double digit growth in nonfoods, despite a Lunar New Year timing shift that reduced Other International and total company sales by approximately 4% and 0.5%, respectively.

Institutional positioning remained active in Q3 filings. American Century Companies increased its stake by 8.5%, adding 127,495 shares to reach 1,619,703 shares worth about $1.5 billion.

Harvest Portfolios Group raised its position by 72.6% to 55,045 shares valued at $50.95 million, while Rafferty Asset Management increased holdings by 2.1% to 51,028 shares worth $47.23 million. Banco Santander boosted its position by 41% to 31,367 shares valued at $29.03 million.

At the same time, Aster Capital reduced its stake by 80.5%, Ibex Wealth Advisors cut 83.8%, and Westfield Capital trimmed 36.3%, reflecting selective profit taking after the stock’s strong run.

Collectively, institutional investors own approximately 68.5% of Costco’s shares, reinforcing its role as a core long term holding across portfolios.

The stock’s advance this year appears supported by consistent traffic gains, digital acceleration, and durable comparable sales growth rather than short term speculation.

See analysts’ growth forecasts and price targets for Costco Wholesale (It’s free) >>>

Is COST Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 7.8%

- Operating Margins: 4.0%

- Exit P/E Multiple: 45x

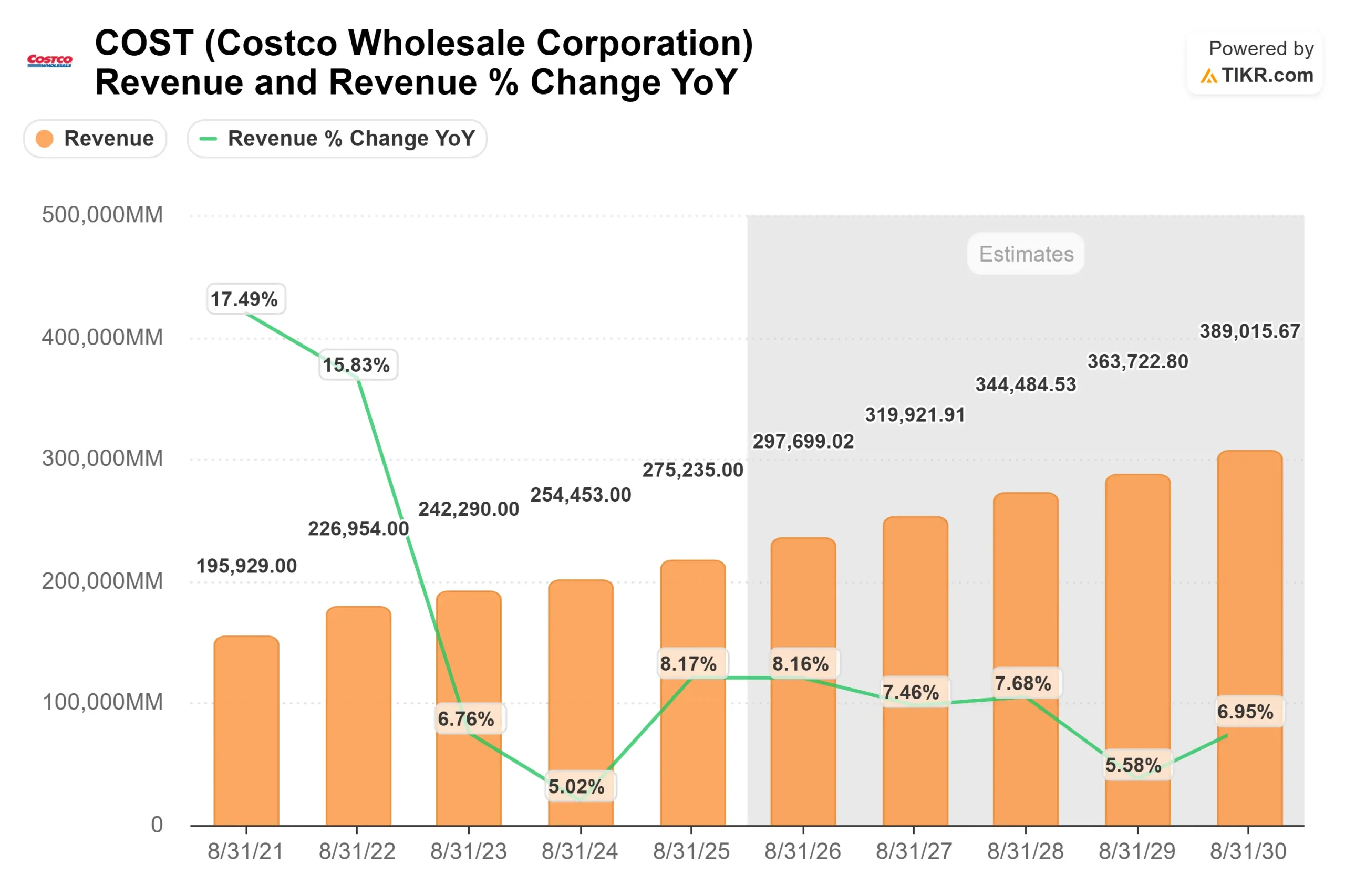

Revenue is projected to expand from about $255 billion in fiscal 2024 to roughly $389 billion by fiscal 2030, supported by steady mid single digit comparable sales growth, continued warehouse expansion, and incremental contribution from membership fee income.

Costco’s model prioritizes traffic and volume over aggressive pricing, which supports resilient demand even in mixed consumer environments.

Operating margins near 4.0% may appear thin, but small improvements can meaningfully impact earnings. Higher private label penetration through the Kirkland brand, improved supply chain efficiency, and SG&A leverage as new warehouses mature can drive EPS growth faster than revenue.

Membership fee income remains a critical driver, as it flows through at high incremental margins and supports overall profit stability.

Over the next 12 months, performance will likely hinge on comparable sales momentum, international warehouse openings, and renewal rates staying near historic highs above 90%. Strength in discretionary categories would signal healthy consumer demand, while continued growth in digital sales reinforces Costco’s competitive positioning.

A future membership fee increase would also serve as a direct earnings lever, as prior increases have meaningfully lifted operating income without hurting retention.

Based on these inputs, the model estimates a target price of $1,192, implying about 19% total upside over roughly 2.5 years, suggesting the stock appears modestly undervalued at current levels near $1,003.

At current levels, Costco appears slightly undervalued, with future returns driven by steady comparable sales growth, disciplined warehouse expansion, and durable membership economics rather than multiple expansion alone.

Estimate a company’s fair value instantly (Free with TIKR) >>>

How Much Upside Does COST Stock Have From Here?

Investors can estimate Costco Wholesale potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See Costco Wholesale true value, or any stock’s, in under 60 seconds (Free with TIKR) >>>