Key Stats for AbbVie Stock

- Past-Week Performance: +3%

- 52-Week Range: $164.4 to $244.8

- Current Price: $234.3

What Happened?

Skyrizi just proved it can replace its own delivery method and still beat placebo by 25 percentage points in Crohn’s remission, a result that cements AbbVie’s IBD dominance at $234.26 and removes the last remaining IV-versus-subcutaneous competitive overhang.

Just yesterday, AbbVie reported Phase 3 AFFIRM results showing risankizumab subcutaneous induction achieved 55% CDAI clinical remission versus 30% for placebo, with 44% endoscopic response versus 14%, driving immediate positive sentiment across the immunology desk.

The mechanics behind this move run deeper than one trial win, as Skyrizi and Rinvoq already delivered $25.9 billion in combined 2025 revenue, surpassing AbbVie’s own 2027 long-term guidance target by $500 million a full two years early.

The market is visibly re-rating AbbVie from a Humira-replacement story into a multi-franchise compounder, with 2026 guidance of $67 billion in revenue and $14.37 to $14.57 adjusted EPS representing nearly 9.5% top-line growth despite continued biosimilar headwinds.

CEO Robert Michael stated on the Q4 earnings call that “Skyrizi and Rinvoq with combined sales of more than $31 billion, already surpassing our 2027 long-term guidance by $0.5 billion,” as the company simultaneously guided Vyalev to blockbuster status and the migraine franchise toward a $5 billion-plus peak.

Further reinforcing conviction, RBC initiated coverage on February 25 with an Outperform rating and a $260 price target, while AbbVie’s $8 billion senior notes offering filed February 26 signals financial firepower for continued pipeline investment and debt refinancing.

Over the next three to five years, AbbVie’s subcutaneous Skyrizi approval in Crohn’s, combined with Rinvoq’s expanding label and a 90-program pipeline spanning obesity, neuroscience, and oncology, positions it to sustain double-digit earnings growth well beyond Humira’s shadow.

Wall Street’s Take on ABBV Stock

The Phase 3 AFFIRM win for subcutaneous Skyrizi in Crohn’s directly removes the last structural competitive risk, confirming that AbbVie’s $21.5 billion Skyrizi revenue target for 2026 rests on an even more defensible clinical foundation.

The fundamental acceleration is undeniable: forward revenue is projected to reach $67.1 billion in 2026, growing 9.7%, while normalized EPS is forecast to surge 45.3% to $14.53, snapping three consecutive years of EPS contraction.

Currently, 13 analysts rate ABBV a Buy, 8 rate it Outperform, 9 rate it Hold, and 1 rates it Underperform, with a mean price target of $248.7, implying 6.2% upside from the March 2 close of $234.26.

The target range spans $184.0 on the low end to $299.0 on the high end, with the high case hinging on Skyrizi IBD dominance holding through subcutaneous approval and Rinvoq’s new indications delivering on their combined $2 billion-plus incremental peak sales estimate.

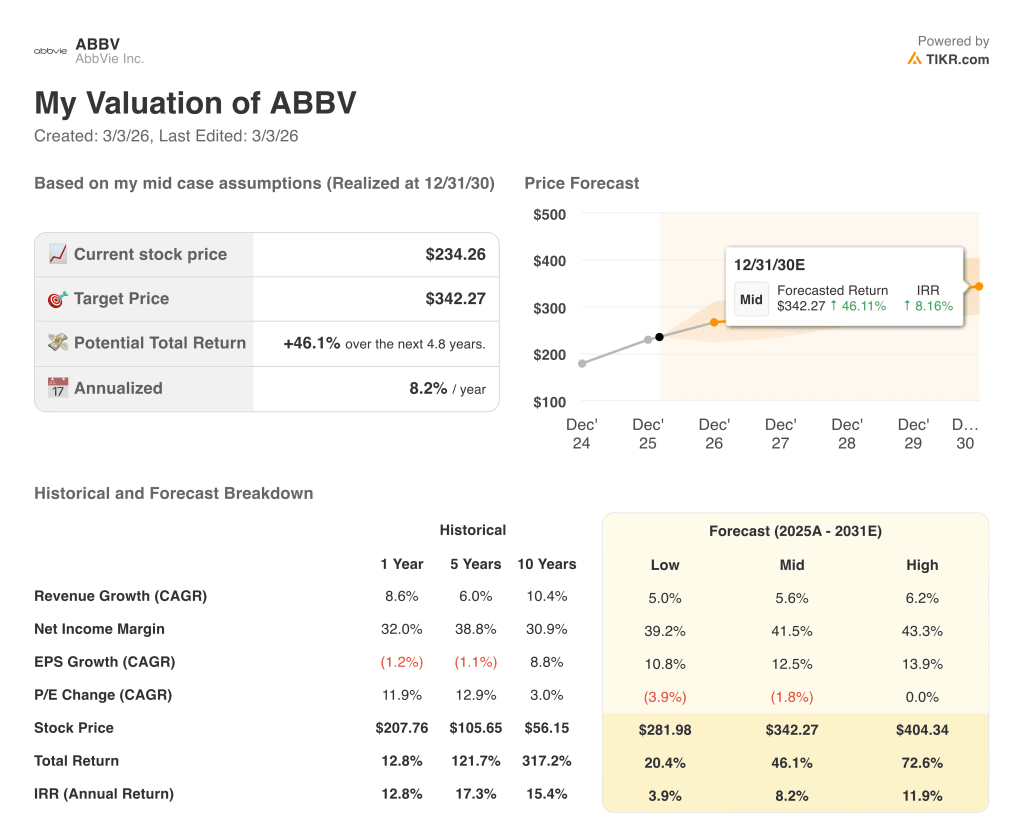

What Does the Valuation Model Say?

The TIKR valuation model sets a mid-case target of $342.3, implying 46.1% total return over 4.8 years at an 8.2% annualized IRR from the current price. That gap between $234.26 today and $342.3 suggests the market has not yet priced the full Skyrizi and Rinvoq compounding runway.

The market is still pricing ABBV as a post-Humira recovery story, yet Skyrizi and Rinvoq already surpassed AbbVie’s own 2027 combined revenue guidance of $31 billion two years early.

Forward EBITDA is projected to reach $33.4 billion in 2026, recovering to a 49.8% EBITDA margin after years of Humira-driven compression, a structural inflection the Street has not fully credited.

CEO Robert Michael’s statement that the migraine and Parkinson’s franchises each carry $5 billion-plus peak potential, both well above current Street models, signals this is a multi-franchise re-rating, not a single-drug story.

The risk that would break the thesis is a faster-than-expected Skyrizi share loss in IBD frontline, where any sustained drop below its current 75% capture rate would directly threaten the $21.5 billion 2026 revenue target.

Tavapadon’s FDA approval decision, expected in Q3, will serve as the first concrete test of whether AbbVie’s neuroscience franchise can deliver the $5 billion-plus Parkinson’s peak management is projecting.

ABBV is undervalued at $234.26 given a 45.3% forward EPS inflection and a $342.3 mid-case model target, with the Skyrizi subcutaneous Crohn’s approval timeline as the key re-rating trigger to watch.

Should You Invest in AbbVie, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ABBV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AbbVie, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ABBV stock on TIKR for Free →