Key Takeaways for Bank of America Stock as of June 2026

- Analysts rate Bank of America stock 16 buys, 6 outperforms, and 2 holds with a mean target of $64, implying around 10% upside from the current price of $58.

- TIKR’s mid-case model values Bank of America at around $77 by December 2030, implying around 33% total return, or roughly 7% annualized.

- Bank of America stock is undervalued at current levels, with normalized EPS tracking ahead of Street estimates as the NII repricing flywheel and above-guide Q2 trading revenue push earnings power higher than consensus reflects.

- Bank of America raised full-year NII growth guidance to 6–8% in Q1 2026, and Co-President Jim DeMare confirmed in June that Q2 Markets revenue will exceed the initial 15% growth target, putting the bank on track for a 17th consecutive quarter of year-over-year trading revenue growth.

See Bank of America’s full NII trajectory, EPS estimates, and analyst targets on TIKR for free →

Bank of America Raises NII Guidance and Q2 Markets Revenue Runs Ahead of the 15% Target

Bank of America (BAC), one of the four largest U.S. banks by assets, reported Q1 2026 earnings on April 15 with revenue of $30.3 billion, up 7% year-over-year, and normalized EPS of $1.11, up 23% from Q1 2025.

Net interest income (NII), the difference between what the bank earns on loans and pays on deposits, came in at $15.9 billion on a fully taxable equivalent basis, up 9% year-over-year and materially flat sequentially despite two fewer days of interest accrual in Q1.

The 9% NII result outperformed management’s prior expectations enough that CFO Alastair Borthwick raised the full-year NII growth guidance range to 6–8% from the previous 5–7%, citing fixed-rate asset repricing, deposit growth, and the removal of two previously expected Fed rate cuts from the forward curve.

CEO Brian Moynihan even flagged NII’s durability at Q1 earnings call: “Net interest income could hit the upper end of the 6% to 8% range this year.”

The bank’s Global Markets division, which covers sales, trading, equities, and fixed income, posted revenue of $7 billion in Q1 (ex-DVA), up 7% year-over-year, with sales and trading reaching $6.3 billion for its strongest decade-long performance, led by equities revenue that rose 30% to a record.

At the Morgan Stanley U.S. Financials Conference on June 9, Co-President Jim DeMare confirmed Q2 is running ahead of Moynihan’s initial 15% Markets revenue guide, saying the equities business is driving the outperformance: “While credit spreads and the like have remained firm, a lot more of the activity and revenues have been coming from the equity business.”

DeMare also said Q2 operating leverage is tracking above 400 basis points, above the 200–300 basis point medium-term target and ahead of Q1’s 290 basis point result.

The bank ended Q1 with 16 consecutive quarters of year-over-year Markets revenue growth and the Global Markets division is now on track for a 17th.

Investment banking fees of $1.8 billion rose 21% year-over-year in Q1, led by M&A and equity capital markets, and DeMare described the IPO pipeline as “plentiful” with large technology names filing S-1s and transaction activity remaining robust despite geopolitical uncertainty from the U.S.-Israeli conflict with Iran.

The efficiency ratio improved 170 basis points year-over-year to 61%, return on tangible common equity (ROTCE) reached 16%, and the CET1 capital ratio stood at 11.2%, with management targeting a 50 basis point management buffer above the regulatory minimum over the medium term.

Track how Bank of America’s Q2 EPS prints against these estimates on TIKR for free →

Analysts Rate Bank of America Stock 22 Buys or Outperforms vs. Just 2 Holds

Analysts covering Bank of America stock hold 16 buy ratings, 6 outperform ratings, and 2 hold ratings, with no underperforms or sells.

The mean price target stands at around $64, with a median of $64, implying around 10% upside from the current price of around $58.

The high target sits at $71 and the low at around $58, a tight range that reflects broad conviction in the bank’s execution trajectory rather than binary macro bets.

Wall Street Expects Bank of America Stock’s Normalized EPS to Climb Around 25% Through Q1 2027

Consensus estimates normalized EPS for Q2 2026 at $1.11, flat with Q1’s reported figure, and rising to around $1.14 in Q3 2026.

Full-year 2026 normalized EPS estimates imply around 17% growth year-over-year from the $3.90 implied 2025 base, and Q1 2027 consensus sits at around $1.21.

The NII revision, above-guide Q2 Markets revenue, and 400-plus basis points of Q2 operating leverage all point to bottom-line earnings power ahead of the flat Q2E consensus, and Bank of America stock has not yet re-rated to reflect execution running above the guided ranges.

The key question now is does Q2 normalized EPS print above $1.11 when the bank reports in July, and if it does, does the Street revise the full-year range upward?

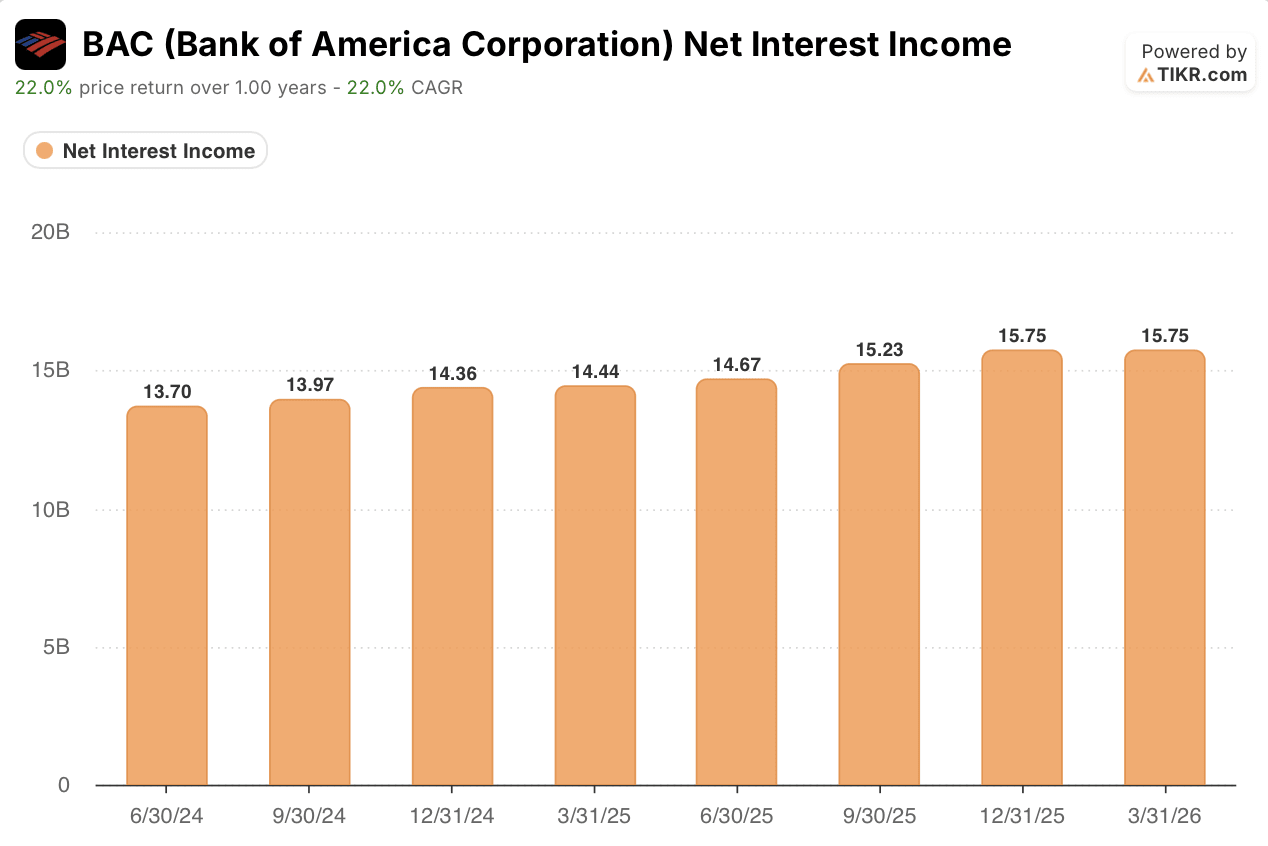

Bank of America’s NII Has Accelerated for Six Straight Quarters and Management Is Guiding Higher

BAC’s net interest income contracted year-over-year through mid-2024, falling 3.2% in Q2 2024 and 2.9% in Q3 2024, before turning positive in Q4 2024 at 3.0% growth.

The acceleration continued through 2025: NII grew 2.9% in Q1 2025, 7.1% in Q2 2025, and 9.1% in Q3 2025, reaching $15.75 billion in Q4 2025 at 9.7% growth.

Q1 2026 NII came in at $15.9 billion, up 9% year-over-year, outperforming management’s own expectations and triggering the guidance raise from 5–7% to 6–8% full-year growth.

CEO Brian Moynihan said at a May conference that NII “could hit the upper end of the 6% to 8% range this year,” with fixed-rate asset repricing, deposit growth, and the removal of previously expected Fed rate cuts all supporting the trajectory.

Management has described the fixed-rate asset repricing tailwind as a 5-year runway, meaning the NII acceleration visible in the historical data is structural, not a one-quarter event, and the six-quarter deceleration-to-acceleration arc in the income statement is the setup, not the story.

TIKR’s $77 Target on BAC Stock Holds If the NII Flywheel Keeps Repricing Into Earnings

TIKR’s mid-case model values Bank of America at around $77 by December 2030, implying around 33% total return from the current price of around $58, or roughly 7% annualized over 4.5 years.

A 7% annualized return from a large-cap money-center bank trading at a 10% discount to Street consensus targets is a compelling proposition for investors who want rate sensitivity and operating leverage in one instrument.

The path is credible: fixed-rate asset repricing has a 5-year runway by management’s own account, NII guidance has already been revised upward once in 2026, Q2 Markets revenue is running ahead of plan, and 400-plus basis points of operating leverage in Q2 suggests the efficiency ratio will continue compressing toward the bank’s multi-year improvement trend.

The thesis resolves cleanly if July’s Q2 earnings confirm EPS ahead of the $1.11 consensus, which the operating leverage and revenue guidance both suggest is likely.

Should You Invest in Bank of America Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Bank of America Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Bank of America Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze BAC stock on TIKR for Free →