Key Stats for Axon Enterprise Stock

- Past-Week Performance: +25%

- 52-Week Range: $396.4 to $885.9

- Current Price: $569.8

What Happened?

Axon‘s $7.4 billion in 2026 bookings, up 46% and accelerating from two straight years of high-20% growth, signals the company has crossed from momentum story to compounding platform, with shares at $569.8 still 36% below their 52-week high.

On February 24, Axon reported Q4 adjusted EPS of $2.15 against a $1.60 estimate, with revenue of $796.7 million beating the $755.2 million consensus, sending the stock up 20% on February 25 as the S&P 500’s top percentage gainer.

Underneath the beat, the structural shift is unmistakable: Software and Services revenue grew 40% to $342.5 million, the AI Era Plan generated $750 million in bookings in its first full year, and net revenue retention expanded to 125%.

Simultaneously, Axon closed its Carbyne acquisition in February, combining it with the Q4 Prepared acquisition to build a full-stack 911 ecosystem that connects call origination directly to Fusus real-time crime centers and drone-first-response dispatch.

COO and CFO Brittany Bagley stated at the Morgan Stanley Technology, Media and Telecom Conference on March 3 that “as you get through to the end of the year, as you’ve digested the memory costs, as you’ve annualized on tariffs, then you’ll start to see some of that software product mix come through,” directly supporting the 28% adjusted EBITDA margin target by 2028.

With only 30% of customers on premium plans, a $6 billion revenue target by 2028, and the Axon Body Mini launching mid-2026 to unlock the enterprise market, the platform’s compounding has significantly more runway than current multiples imply.

Wall Street’s Take on AXON Stock

The $750 million AI Era Plan bookings in its first full year forces a direct re-evaluation of Axon’s revenue ceiling, as software monetization is still in the earliest innings of a $14.4 billion contracted backlog.

Revenue grew 33.5% in 2025 to $2.8 billion, and the Street projects $3.6 billion for 2026 at 29.1% growth, while EBITDA margins hold steady at 25.5% before expanding toward 28% by 2028.

As of March 4, 10 analysts rate AXON a Buy, 8 Outperform, and 2 Hold, with zero Sells, and the mean price target of $735.0 implies 29.0% upside as analysts wait for enterprise and federal revenue to materialize at scale.

The Street’s high target of $950 prices in full realization of the AI Era Plan, Carbyne and Prepared 911 integration, and enterprise adoption, while the low target of $521.2 reflects tariff headwinds and the 25-basis-point gross margin compression already visible in Q4.

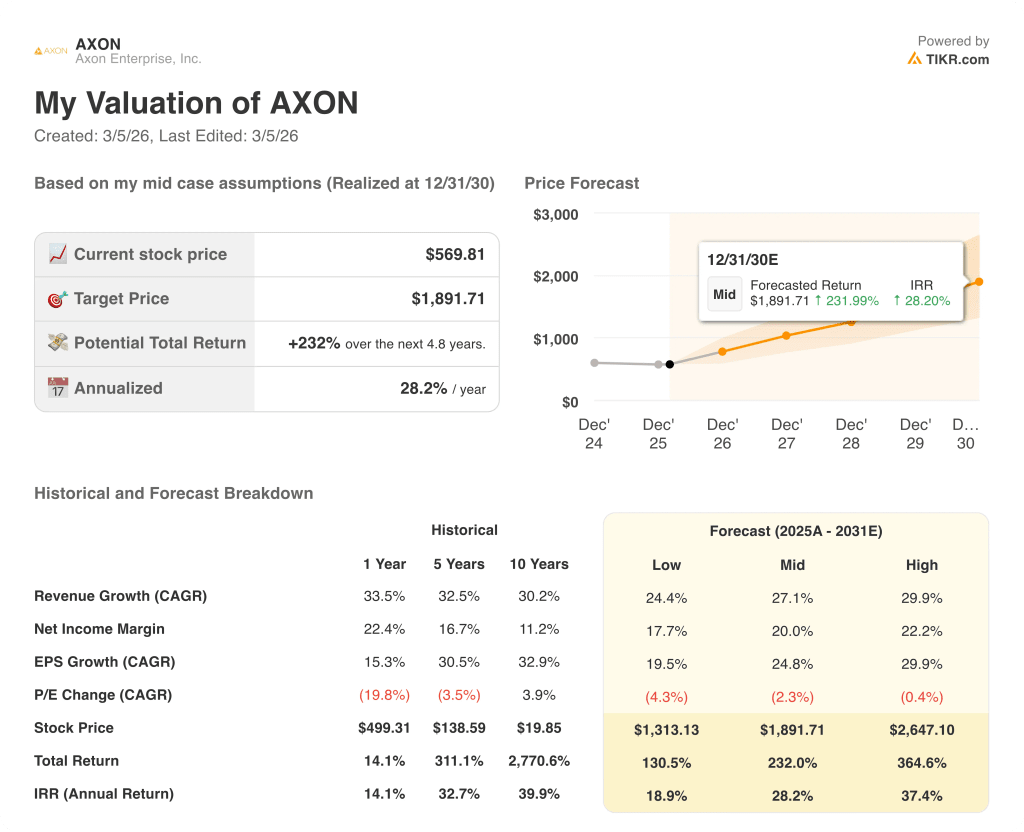

What Does the Valuation Model Say?

The mid-case TIKR valuation model targets $1,891.7 by December 2030, implying 232% total return from current levels at a 28.2% annualized IRR.

The market is pricing Axon as though the AI Era Plan is a feature, not a platform shift, yet $750 million in first-year bookings with only 30% of customers on premium plans contradicts that framing entirely.

The 5-year EPS CAGR of 30.5% runs directly against a forward P/E contracting at 2.3% annually in the mid-case, suggesting multiple compression is suppressing a structurally stronger earnings profile.

Management’s signal that Carbyne closed in February with zero revenue impact yet baked into 2026 guidance confirms the market has not priced the full 911 ecosystem monetization opportunity.

The most credible risk is tariff-driven gross margin compression, with Platform Solutions already down to 49.3% adjusted gross margin in Q4 from 52.2% a year earlier.

Just accordingly, the Axon Body Mini launch in mid-2026 and Q1 2026 earnings will serve as the first hard test of whether enterprise adoption and bookings momentum can sustain the 27% to 30% revenue growth guide.

AXON is a Buy, with the AI Era Plan adoption rate and net revenue retention at 125% as the primary metrics to monitor against any bookings deceleration.

Should You Invest in Axon Enterprise, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AXON stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Axon Enterprise, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AXON stock on TIKR for Free →