Key Stats for FedEx Stock

- Past-Week Performance: +0.9%

- 52-Week Range: $194.3 to $382.9

- Current Price: $384.1

What Happened?

FedEx is no longer a delivery company chasing volume growth, as its February 12 Investor Day revealed a target of $6 billion in annual free cash flow by 2029, nearly doubling its current $3.8 billion baseline, with shares sitting at $384.09 near 52-week highs.

On February 12, CEO Raj Subramaniam unveiled a 14% adjusted operating income CAGR through 2029, targeting $8 billion in operating income at an 8% margin, up from a 6% adjusted baseline, while Jefferies raised its price target to $450 on March 3.

The structural engine behind that margin expansion is Network 2.0, which has already delivered 10% pickup and delivery cost reductions in optimized U.S. markets and is on track to unlock $1 billion in savings by end of calendar 2026 and $2 billion by end of 2027.

On the other hand, the February 20 Supreme Court ruling invalidating Trump’s IEEPA tariffs triggered FedEx to file suit on February 23 seeking a full refund of all IEEPA duties paid, with the company promising to pass refunds directly to shippers if recovered.

Chief Revenue Officer Brie Carere stated at the February 12 Investor Day that “our surface capacity is currently at utilization levels that we have not seen since the pandemic,” directly supporting the company’s 2% yield growth assumption embedded in its 2029 revenue target of $98 billion.

Looking ahead, the June 1 FedEx Freight spin-off will create a pure-play industrial network generating $16 billion in cumulative free cash flow through 2029, while the InPost minority investment positions FedEx to capture Europe’s out-of-home delivery growth without integrating a single domestic operation.

Wall Street’s Take on FDX Stock

Here is the Wall Street’s Take for FDX:

The February 12 Investor Day reframes FedEx not as a volume-dependent shipper but as a margin-expansion and free cash flow story, with the Freight spin and Network 2.0 forcing a fundamental re-evaluation of its earnings trajectory through 2029.

Consensus estimates project FY 2026 revenue of $92.7 billion (+5.4% YoY) and normalized EPS of $18.61 (+2.3%), building toward management’s 14% adjusted operating income CAGR target that relies on expenses growing below 2% annually.

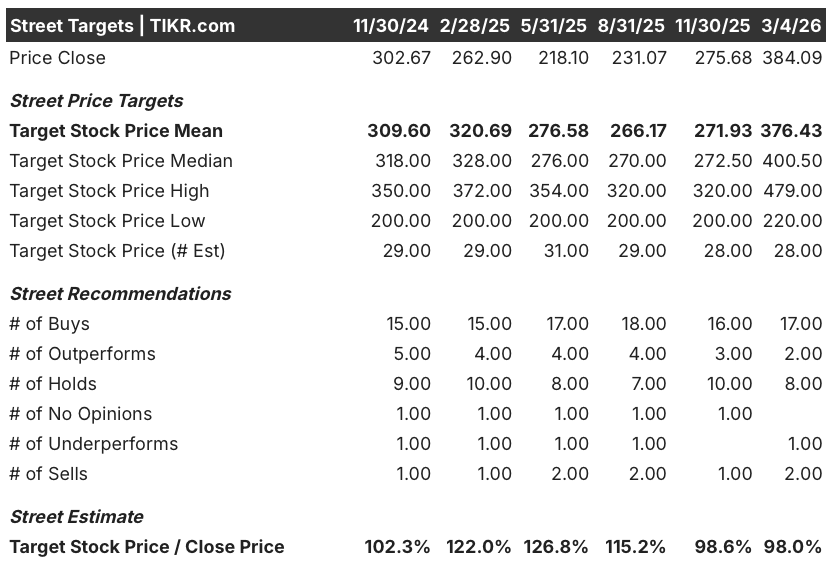

17 analysts rate FDX a Buy, 2 Outperform, 8 Hold, 1 Underperform, and 2 Sell, with a mean price target of $376.43 implying 2% downside from the March 4 close of $384.09, as analysts await Q3 2026 results on March 19 for early margin execution evidence.

The Street’s high target of $479.00 anchors to successful Network 2.0 completion and the June 1 Freight spin unlocking valuation clarity, while the low target of $220.00 reflects risk that Middle East disruptions and tariff refund litigation compound already soft near-term volume trends.

What Does the Valuation Model Say?

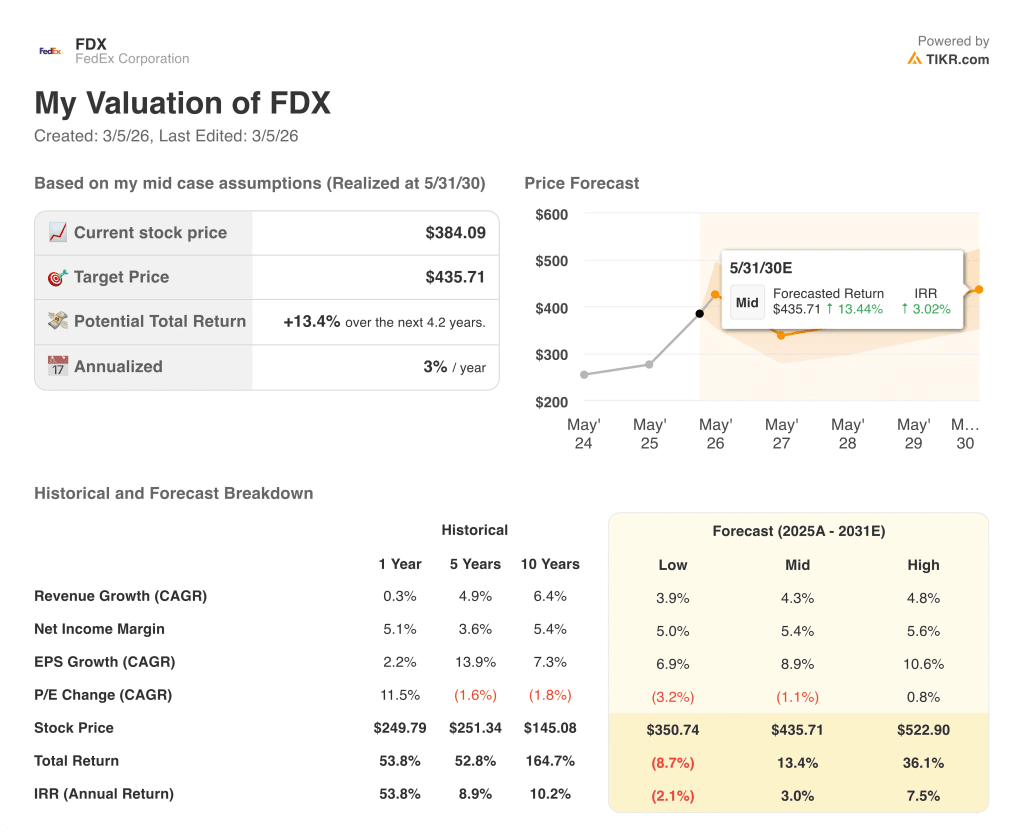

The TIKR mid-case valuation model prices FDX at $435.71 by May 2030, implying only 13.4% total return from current levels with a 3% annualized IRR.

The market is pricing FDX as if its $2 billion Network 2.0 savings target is uncertain, ignoring that $1 billion of that is expected to land by end of calendar 2026.

FDX’s 5-year revenue CAGR of 4.9% and 10-year EPS CAGR of 7.3% historically supported higher multiples than the stock commands near $384.09 today.

Management’s reduction of FY 2026 CapEx guidance to $4.3 billion from $4.5 billion signals deliberate capital discipline, confirming that free cash flow expansion is a management priority, not just a target.

The single most credible threat is prolonged Middle East conflict disrupting international air freight volumes, where FedEx generates $25 billion in annual international revenue at a thin 3.6% margin.

March 19 Q3 2026 earnings call is the moment of truth, as management must demonstrate early Network 2.0 operating leverage before the June 1 Freight spin resets the investment thesis entirely.

FDX earns a Hold at current levels: the transformation is real but the 3% annualized IRR to fair value demands patience, with Q3 2026 operating margin the metric to watch.

Should You Invest in FedEx Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FDX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FedEx Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FDX stock on TIKR for Free →