Key Stats for Arm Stock

- 52-Week Range: $100 to $428

- Current Price: $393

- Street Mean Target: $245

- Street High Target: $500

- Analyst Consensus: 21 Buys, 7 Outperforms, 10 Holds, 1 Underperform

- TIKR Model Target (Mar. 2031): $1,773

ARM Stock Surges 277% on Record Earnings and a $2 Billion AGI CPU Demand Surge

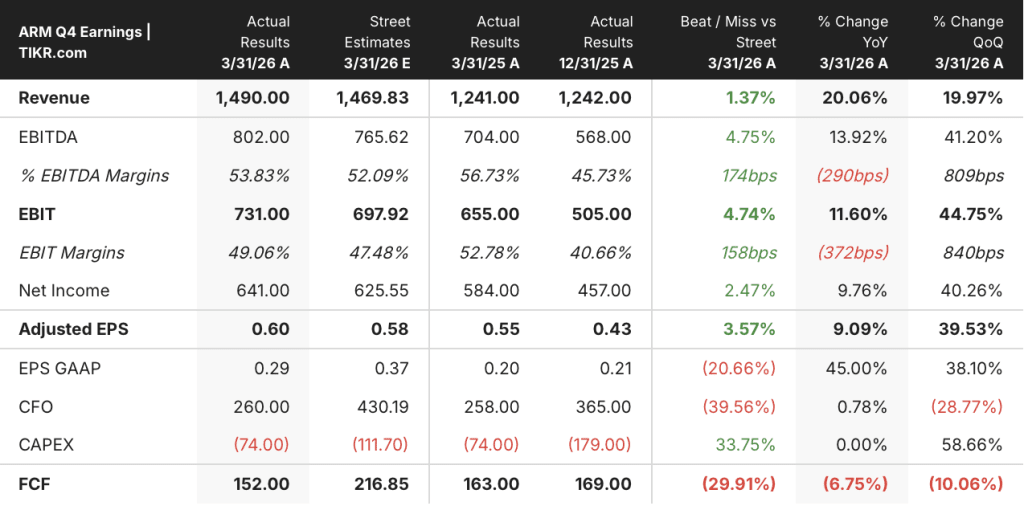

Arm Holdings (ARM) delivered a record quarter and a record fiscal year in Q4 FY2026, with revenue of $1.49 billion up 20% year-over-year, capping a full-year total of $4.92 billion and the company’s third consecutive year of greater than 20% growth since its 2023 IPO.

The stock’s 277% year-to-date surge is not a single-catalyst move.

It is the accumulation of three compounding developments: the launch of the Arm AGI CPU at the company’s March Arm Everywhere event, the subsequent doubling of stated customer demand from $1 billion to over $2 billion across FY2027 and FY2028, and a blitz of ecosystem wins at Computex in early June that pulled in Oracle and ByteDance as named customers.

ARM CEO Rene Haas stated on the Q4 earnings call: “The direction is clear. Customers want Arm at the center of the AI data center.”

The AGI CPU is not a licensing product.

It is a finished silicon product, purpose-built for agentic AI workloads, with 136 Neoverse V3 cores and a rack architecture promising more than 2x the performance per rack versus x86 at up to $10 billion in reduced AI data center capital expenditure per gigawatt.

Meta is the lead co-development partner and is targeting personal superintelligence for over 3 billion users on Arm infrastructure.

Cloudflare, SAP, SK Telecom, Cerebras, OpenAI, and Rebellions have also committed to the platform, and at NVIDIA GTC, NVIDIA unveiled Vera: a next-generation Arm-based CPU with 88 cores per chip, built into a dedicated 256-chip rack for agentic AI orchestration.

The data center royalty business is running in parallel, not being cannibalized.

Data center royalty revenue more than doubled year-over-year in Q4 FY2026, driven by hyperscalers deploying Arm-based custom silicon at scale: AWS with Graviton, Google pairing its TPU 8t and 8i training and inference chips with custom Arm Axion CPUs delivering 80% performance improvement, and Microsoft advancing its Cobalt Arm-based compute platform.

Haas said on the call that data center royalties are expected to double again year-over-year in FY2027.

Full-year licensing revenue reached $2.31 billion, up 25%, while annualized contract value grew 22% year-over-year, signaling that the underlying licensing business has not lost momentum even as the silicon story takes the headlines.

The Nvidia RTX Spark announcement at Computex on June 1, which positions Arm-based PC chips as the engine for local AI agents on Windows PCs, pushed ARM stock up approximately 14% in a single session, with Arm’s chip technology embedded in both Nvidia and Apple’s processor architectures.

What Analysts Say About ARM Stock After the 277% Run

The street is deeply split, and the split is structural.

ARM stock carries 21 Buy ratings, 7 Outperforms, 10 Holds, 1 Underperform, and 2 Sells in the current consensus table, with a mean target of around $245 and a street high of $500, both well below a current price near $369.

This is an unusual configuration: a strong Buy-majority consensus with a mean target that implies a roughly 38% downside from where the stock actually trades.

Mizuho raised its price target to $500 on June 4, citing accelerating agentic AI tailwinds from Computex, including the Oracle and ByteDance AGI CPU additions and the RTX Spark PC partnership, while keeping an Outperform rating.

The Hold camp is not bearish on the business.

It is bearish on the entry price: a stock that tripled in five months, with the street’s highest published target sitting $72 below the current price on June 5.

Consensus revenue estimates for Q1 FY2027 call for around $1.26 billion, up roughly 20% year-over-year, with both royalty and licensing revenue expected to grow at approximately 20% in the quarter.

For the full FY2027, Jason Child guided to royalty growth in the roughly 20% range for each quarter, with licensing approximately 60% weighted to the second half.

EPS normalized for Q1 FY2027 is guided to $0.40 plus or minus $0.04, up around 14% year-over-year.

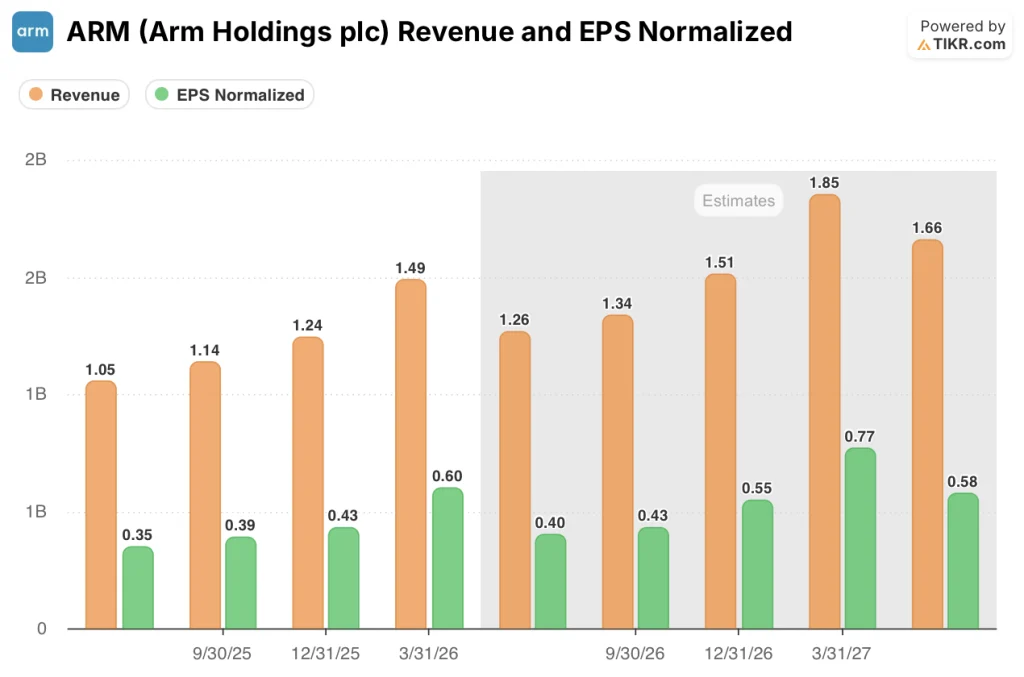

The forward revenue trajectory accelerates sharply in the estimates table: consensus projects Q3 FY2027 revenue at around $1.51 billion, Q4 FY2027 at around $1.85 billion, and Q1 FY2028 at around $1.66 billion, as AGI CPU production silicon revenues begin landing in Q4 FY2027 and build into the following year.

The single tension the bulls and bears share: supply chain capacity for the AGI CPU.

Haas confirmed that Arm has line of sight to over $2 billion in demand but is maintaining the $1 billion revenue guidance while securing additional wafer supply from TSMC and packaging capacity from Socionext.

ARM Trades at a Revenue Scale Discount to AMD and Intel: the AGI CPU Is the Only Path to Parity

ARM’s quarterly revenue of $1.49 billion in Q4 FY2026 is a fraction of AMD’s $9.92 billion and Intel’s $12.43 billion in the same period, making ARM’s premium valuation entirely forward-looking.

AMD’s revenue estimates run around $11.3 billion for June 2026, approximately $12.4 billion for September, roughly $15.6 billion for December, around $16.4 billion for March 2027, and approximately $17.8 billion for June 2027.

Intel’s revenue estimates run around $14.4 billion for June 2026 and stay roughly flat through June 2027 at approximately $15.9 billion, signaling stabilization rather than acceleration.

That plateau puts Intel in a different category from both ARM and AMD: large but not growing, and not competing for the agentic AI CPU market on a forward revenue basis.

ARM’s forward revenue runs around $1.3 billion for June 2026, approximately $1.3 billion for September, roughly $1.5 billion for December, around $1.9 billion for March 2027, and approximately $1.7 billion for June 2027.

At around $1.9 billion by March 2027, ARM’s quarterly revenue estimate is still roughly 9x smaller than AMD’s approximately $16.4 billion estimate for the same period.

The entire case for ARM’s valuation premium rests on the AGI CPU closing that gap over the next four to five years, not the next four quarters.

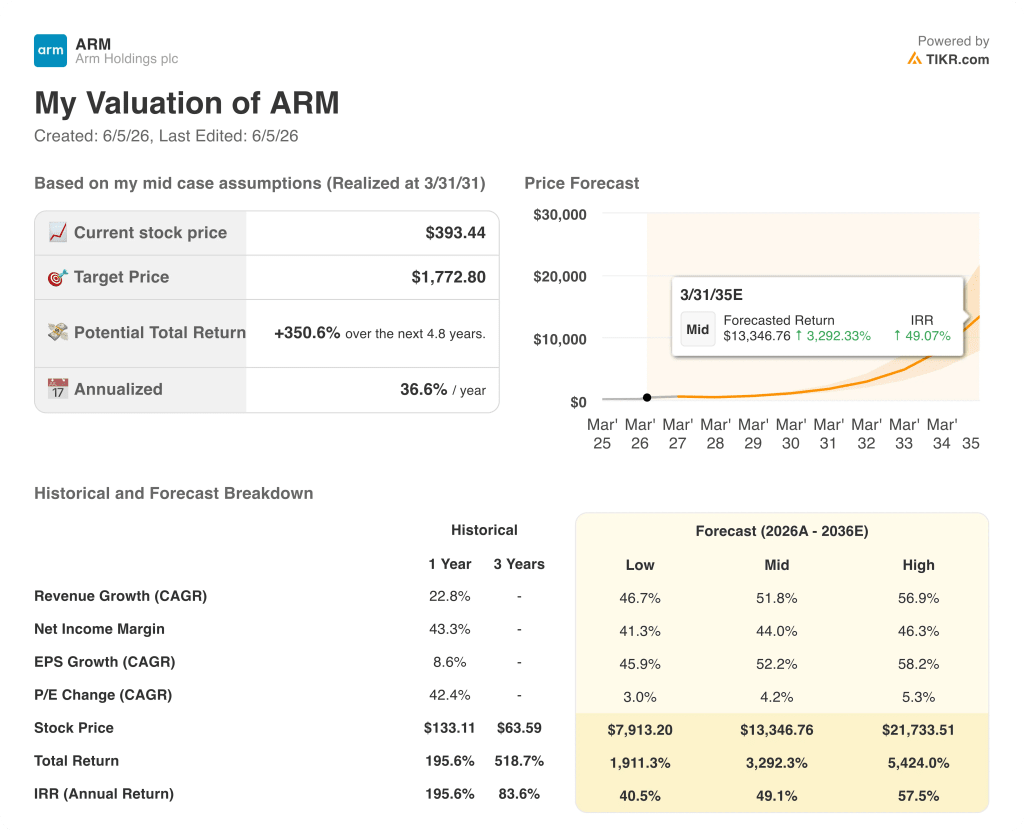

Is ARM Stock Undervalued in 2026? What the TIKR Model Says

TIKR’s base case values Arm Holdings at approximately $1,773 by March 2031, implying around 351% total return from the current price of $369, or roughly 37% annualized over approximately 4.8 years.

ARM stock is not undervalued on any near-term fundamental screen. But the TIKR model is not a near-term model.

It is built around a revenue CAGR assumption of roughly 52% through 2036, a net income margin converging toward 44%, and EPS growing at a CAGR of roughly 52%, anchored to one scenario: that Arm’s stated $15 billion AGI CPU revenue target by FY2031 and its stated $10 billion IP business target are both realized.

That is the tension the stock embeds. The current price of $369 is not pricing in the street’s $245 mean target. It is pricing in a version of the TIKR mid-case, partially discounted for execution risk, particularly on supply chain ramp and the pace at which AGI CPU revenue scales from the initial roughly $90 million in Q4 FY2027 toward the multi-billion run rate required by FY2031.

The scenario math, as the TIKR model builds it: if revenue grows at around 47% and net income margins hold near 41%, the low case produces a price of around $7,913 by March 2031, a total return of roughly 1,911% and an IRR of around 41% annually. The mid case at around 52% revenue growth and 44% margins reaches approximately $13,347 and an IRR of roughly 49%. The high case, at around 57% revenue growth and 46% margins, produces approximately $21,734 and an IRR of roughly 58%.

All three scenarios land far above the current price, which means the question is not whether to believe in ARM’s long-term growth story. The question is whether the supply chain, the regulatory backdrop on CPU exports to China, and the pace of hyperscaler adoption deliver the growth trajectory the model assumes within the timeframe it assumes.

Haas himself said at Computex that banning AI CPU exports to China would be “nearly impossible” given the difficulty in establishing specific performance thresholds, providing some buffer on the regulatory risk. But the supply constraint is real and self-acknowledged: every unit of unmet demand is a quarter of revenue that does not arrive on schedule.

At $369, ARM stock is fairly valued against the TIKR mid-case only if investors believe the supply chain resolves before the demand window closes.

Is ARM stock a buy right now?

ARM stock carries a Buy-majority analyst consensus with 21 Buy ratings and 7 Outperform ratings, but the street mean target of around $245 sits roughly 38% below the current price of $369.

The TIKR base case targets approximately $1,773 by March 2031, implying around 351% total return at roughly 37% annualized, anchored to Arm’s $15 billion AGI CPU and $10 billion IP revenue targets by FY2031.

What is the price target for ARM stock?

The street mean target for ARM stock is around $245, with a high target of $500. Mizuho raised its target to $500 on June 4, 2026, citing Computex developments including Oracle and ByteDance joining the AGI CPU platform.

The TIKR mid-case model target is approximately $1,773 by March 2031, based on a revenue CAGR assumption of roughly 52% and a net income margin of around 44%.

Should You Invest in Arm Holdings plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Arm Holdings stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Arm Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ARM stock on TIKR for Free →