Key Stats for NVIDIA Stock

- Current Price: $218.66

- Target Price (Mid): ~$525

- Street Target (Mean): ~$298

- Potential Total Return (Mid): ~140%

- Annualized IRR (Mid): ~21% / year

- Earnings Reaction: -1.77% (reported 5/20/26)

- Max Drawdown: -20.22% (3/30/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

NVIDIA Corporation (NVDA) reported $81.6 billion in revenue on May 20, and the stock fell 1.77% the next session. That reaction, a record quarter followed by a sell-off, has become a pattern for NVDA shareholders. So, when CFO Colette Kress took the stage at the Bank of America Global Technology Conference on June 4, the morning after GTC Taipei had sent the stock surging +6.26%, investors had specific questions that the earnings call had left unanswered.

Kress answered them. Vera Rubin Ships in Q3. The demand base has structurally diversified beyond hyperscalers. The company holds $124 billion in supply commitments. And a 50% amount that can be returned to shareholders, including a $1-per-share annual dividend, is a long-term commitment, not a one-time event.

Vera Rubin Ships in Q3 Earlier Than the Market Expected

At GTC Taipei on June 1, CEO Jensen Huang confirmed that Vera Rubin, pairing the new Vera CPU with the Rubin GPU, had entered full mass production, with OpenAI, Anthropic, and SpaceX among its first customers. At the BofA conference two days later, Kress made the timeline explicit: “…it is coming soon. It’s ready for Q3.”

Q3 means the ramp begins in the quarter ending October 2026. Many investors had assumed that Vera Rubin would be a late fiscal-2027 contributor. Kress was also explicit that NVIDIA is “already in full production in order to make that plan within Q3,” so the supply chain commitments are locked. She was asked whether Vera Rubin was concerned about the kind of margin levels despite all this because of the planning work and prepurchase commitments. “Nothing as we see moving forward, changes to where we are today.”

See historical and forward estimates for NVIDIA stock (It’s free!) >>>

The Demand Base Has Diversified. The Bears’ Core Argument is Weaker

The persistent bear argument against NVDA is customer concentration: if Microsoft, Google, Amazon, and Meta control AI capex, a slowdown at any one of them hits NVDIA disproportionately.

At the BofA conference, Kress described ACIE (AI Cloud Infrastructure and Enterprises) as a structurally distinct category. These operators are not repurposed general-purpose cloud providers. They are newly-built AI infrastructure problems, national AI factories, all built on NVIDIA’s full reference architecture.

The ASIC displacement argument also came up. Kress’s answer was not that custom chips cannot compete on specs. It was that they could not replicate 25 years of software development. “It was determined at the point that they went and designed it, the time that they went to go tape it out, it’s done. It doesn’t have the ability to change over that.” NVIDIA’s platform evolves with the workload. That distinction matters more as agentic AI tasks grow more complex and variable.

What the Peer Comparison Says About the Valuation Discount

For a company growing hyperscaler revenue at around 115% year-over-year and launching a next-generation architecture in Q3, NVIDIA’s valuation multiples tell a surprisingly modest story.

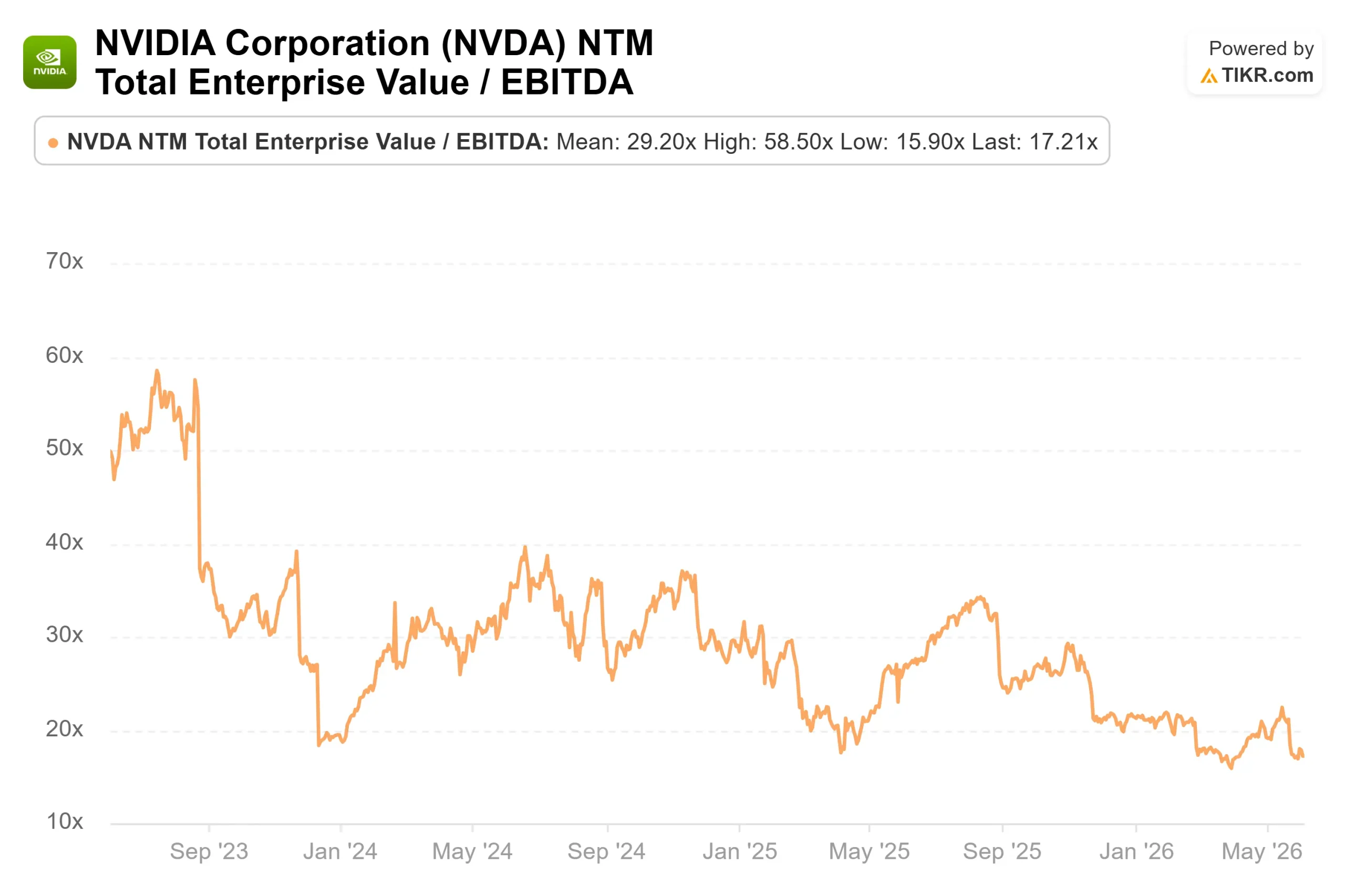

According to TIKR data, NVIDIA trades at 22.00x NTM P/E against a peer mean of around 41x and a median of around 36x. On free cash flow, it’s 22.92x NTM MC/FCF versus a peer mean of around 42x. On EBITDA, 17.52x versus a peer mean of around 30x. On every earnings-based metric, the most important infrastructure business in AI trades at a discount to a peer group growing at a fraction of its pace.

The bear case on valuation has always been that NVIDIA is priced for perfection. The peer comparison suggests something closer to the opposite. That gap — against the backdrop of Vera Rubin, the ACIE growth trajectory, and $124 billion in supply chain commitments — is either the market’s unresolved concern about growth durability, or an opportunity that the next few quarters could close.

See how NVIDIA performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $218.66

- Target Price (Mid): ~$525

- Potential Total Return: ~140%

- Annualized IRR: ~21% / year

See analysts’ growth forecasts and price targets for NVIDIA stock (It’s free!) >>>

The mid-case uses a revenue CAGR of around 21% and a net income of around 56%, both from the TIKR model. The two primary revenue drivers are continued data center compute and networking growth from hyperscaler and ACIE segments, and emerging VERA CPU standalone revenue.

TIKR shows LTM EBIT margin at 64% and LTM gross margin at 74.1%, with the mid-case holding margins roughly flat through 2031. The street’s mean target is $298.07 per TIKR, with 48 Buys, 10 Outperforms, 2 Holds, 0 Underperforms, and 1 Sell as of June 4. The TIKR mid-case at ~$525 sits well above even the most aggressive Street targets. Neither figure includes any China data center revenue. With any policy change, there is genuine upside that no analyst’s base case currently prices.

Conclusion

NVIDIA entered the BofA conference with a stock that had just sold off on a record quarter. It left with three things clarified: Vera Rubin ships in Q3, the demand base is structurally broader than the bear thesis assumed, and the capital return commitment is durable.

The valuation picture adds an unusual wrinkle. At 22.00x NTM P/E against a peer median of around 36x, NVIDIA is not priced for perfection. It is priced like a company that the market is still stress-testing. The TIKR mid-case at around $525 — implying around 140% upside and an annualized IRR of around 21% — sits well above the Street mean of around $298, suggesting that even sell-side consensus may be underweighting the Vera Rubin ramp and the ACIE growth trajectory.

The unresolved risks are real. China’s export restrictions remain a structural overhang. The CapEx cycle could turn. And the $525 mid-case assumes margins hold roughly flat through 2031 — an assumption that deserves scrutiny as competition develops.

But the BofA conference did what the earnings call did not: it gave investors a cleaner read on the durability of the demand story. For a stock trading at a discount to peers on every earnings-based metric, that clarity matters.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVIDIA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVIDIA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!