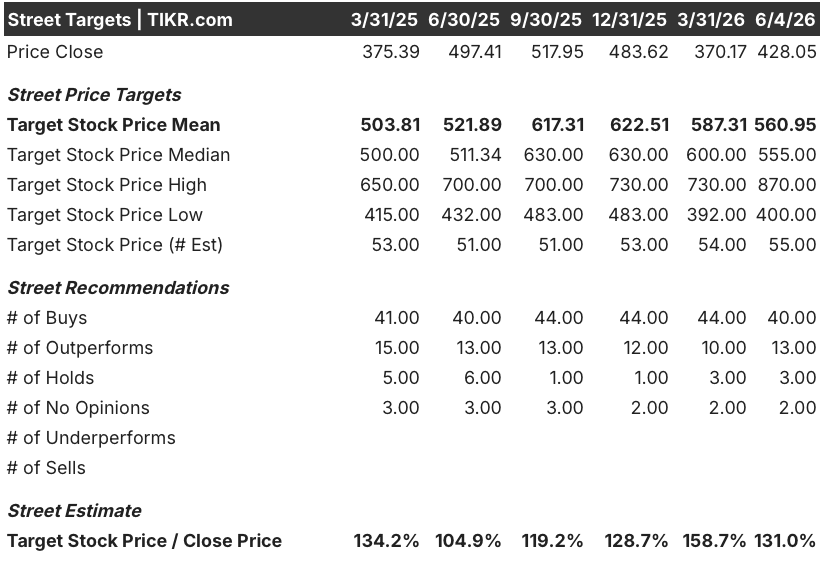

Key Stats for Microsoft Stock

- 52-Week Range: $356 to $555

- Current Price: $428

- Street Mean Target: $561

- Street High Target: $870

- Analyst Consensus: 40 Buy, 13 Outperform, 3 Hold

- TIKR Model Target (Jun. 2030): $872

Microsoft’s AI Business Hits $37 Billion ARR as Azure Grows 40% in Q3 FY26

Microsoft Corporation (MSFT) delivered a record third quarter on April 29 as Microsoft Cloud revenue surpassed $54 billion and Azure grew 40% year-over-year in constant currency, yet Microsoft stock has remained nearly 23% below the mean Street price target heading into June.

The company posted $82.9 billion in total revenue for the March quarter, up 18% year-over-year, beating guidance and coming in ahead of analyst expectations across revenue, operating income, and earnings per share.

The AI revenue line was the undeniable headline of the quarter.

MSFT’s AI business crossed $37 billion in annualized revenue run rate, growing 123% year-over-year, a figure that CEO Satya Nadella framed as the beginning of a platform shift, not a product cycle.

“We are at the beginning of one of the most consequential platform shifts that will change the entire tech stack as agents proliferate and become the dominant workload,” Nadella told analysts on the Q3 2026 earnings call.

Microsoft 365 Copilot paid seats crossed 20 million and grew 250% year-over-year, representing the fastest growth rate since the product launched.

The quarter also revealed early structural evidence that the company’s business model is shifting: nearly 60% of Copilot service customers are now purchasing usage-based credits rather than fixed-seat licenses, and GitHub announced a transition to usage-based pricing effective June 1.

Capital expenditures came in at $31.9 billion for the quarter, down sequentially, with roughly two-thirds allocated to short-lived assets like GPUs and CPUs that translate into near-term revenue capacity rather than the long-dated infrastructure that clouds the quarterly free cash flow figure.

Commercial remaining performance obligation reached $627 billion, growing 26% year-over-year when excluding OpenAI commitments, representing a dense forward revenue backlog that the quarterly earnings snapshot obscures.

CFO Amy Hood guided for Q4 FY26 revenue of $86.7 to $87.8 billion and projected Azure to accelerate modestly in the second half of calendar 2026 compared to the first half.

The company also disclosed that it expects full-year FY26 capital expenditures of approximately $190 billion, including roughly $25 billion in component price impact, which has been the primary source of investor anxiety this year.

Hood stated the company expects another year of double-digit revenue and operating income growth in FY27.

The quarter’s other catalysts included a $9.7 billion Pentagon enterprise software deal announced in late May, Microsoft Build featuring Project Solara and a new Surface RTX Spark Dev Box, a healthcare AI partnership with Mayo Clinic, and the unveiling of Majorana 2, a next-generation quantum chip targeting 2029 commercialization.

Why Analysts Still Hold $561 as the Mean Target for Microsoft Stock Despite a Rough Year

Microsoft stock is down roughly 23% from its 52-week high of $555 despite three consecutive quarters of strong cloud execution, and the analyst consensus remains overwhelmingly constructive because the numbers that matter most for the forward earnings case have not broken down.

The Wall Street view is anchored to the revenue trajectory: consensus estimates $87.7 billion in revenue for the June quarter, reflecting around 15% year-over-year growth, and projects revenue accelerating through fiscal 2027 into the $96 to $103 billion per quarter range.

That trajectory is not speculative.

It is backlog-supported: the $627 billion RPO with roughly 25% recognized in the next 12 months implies around $157 billion in near-term contracted revenue, growing 39% year-over-year.

The analyst community is not widely split on direction.

Of the 56 analysts covering MSFT, 40 rate it Buy and 13 rate it Outperform, with only 3 Holds and no Underperforms or Sells recorded on the TIKR data as of June 4.

The Street mean target of $561 implies around 31% upside from the current price of $428, and the high-end target of $870 sits near where TIKR’s mid-case valuation model lands.

The bearish counterargument that has kept the stock suppressed since late 2025 centers on three concerns: the margin dilution from $190 billion in full-year capex, the unraveling of the OpenAI exclusivity structure, and the risk that enterprise AI adoption converts to real usage metrics more slowly than the ARR figures suggest.

The first concern is real but overstated: operating margins came in at 46% for Q3 FY26 and Hood guided for full-year FY26 operating margins to be up roughly 1 point year-over-year inclusive of the one-time voluntary retirement program costs, which is a compelling result given the scale of infrastructure investment underway.

The second concern is more nuanced than the headlines suggest: Nadella confirmed on the call that Microsoft retains royalty-free access to OpenAI IP through 2032 with full rights to exploit it, the OpenAI revenue share agreement continues through 2030, and OpenAI remains a large Azure compute customer.

The third concern is where Microsoft stock’s near-term re-rating most depends: Copilot queries per user grew nearly 20% quarter-over-quarter, weekly Copilot engagement is now at the same level as Outlook, and the Dynamics 365 LinkedIn talent solutions agents already surpassed a $450 million annualized revenue run rate, all pointing to genuine adoption depth, not just seat count expansion.

With 53 of 56 analysts constructive on the name and a mean target implying roughly 31% upside, Microsoft stock looks priced for a scenario where the AI buildout permanently impairs economics, while the data from the quarter argues for the opposite conclusion.

Microsoft Stock Holds the Revenue Growth Lead Over Apple While Google Closes the Gap

Microsoft stock’s revenue growth rate of 18.30% in the March 2026 quarter outpaced both Apple’s (AAPL) 16.60% and Alphabet’s (GOOGL) 21.8%, but the forward estimates chart reveals a more interesting divergence than the trailing figures suggest.

Consensus projects MSFT’s revenue growth to decelerate to around 15% through mid-2026 before re-accelerating toward 17% by the June 2027 quarter, while Apple’s growth is expected to slow sharply to around 6% in late 2026 before recovering modestly to around 11% by March 2027.

Alphabet is the only peer that holds a structurally higher revenue growth rate across the forward estimate horizon, sustaining around 20% through 2027, which is the honest competitive read that makes MSFT’s current price gap relative to the Street mean target notable: a stock growing revenue in the mid-to-high teens with a $627 billion backlog, trading 24% below analyst consensus, against a peer whose growth premium is around 4 points and whose stock is not comparably discounted.

Apple’s growth deceleration toward 6% in the December 2026 quarter is the starkest contrast in the chart and the clearest argument for MSFT’s relative positioning: the market is penalizing Microsoft for its capex cycle while Apple faces a demand deceleration that the consensus is already pricing in.

Is Microsoft Stock Undervalued in 2026? TIKR’s $872 Model and the Capex Assumption That Decides It

TIKR’s base case values Microsoft at approximately $872 by June 2030, implying around 104% total return from the current price of $428, or roughly 19% annualized over approximately 4 years.

At the current price, with $627 billion in contracted backlog, 40% Azure growth, and a $37 billion AI ARR growing at 123%, Microsoft stock is priced as though the capex cycle will consume its economics permanently rather than build the capacity that converts a demand-constrained business into a revenue-acceleration story.

The mid-case in TIKR’s model requires approximately 16% revenue CAGR from 2025 through 2035 and roughly 39% net income margins across that period, both of which are consistent with the company’s 5-year and 10-year historical performance and the demand visibility the RPO provides.

The single non-trivial tension is the P/E multiple: TIKR’s model projects around 4% annual P/E compression in the mid-case, which means the return scenario does not depend on multiple expansion but rather on earnings growth more than outpacing the contraction in what investors are willing to pay.

If revenue growth comes in at approximately 14% CAGR and margins converge toward 36%, TIKR’s low-case scenario points to around $1,119 in stock price by 2035, implying roughly 13% annualized returns over that longer horizon.

If AI monetization fully materializes with approximately 18% revenue CAGR and margins approaching 41%, the high case reaches approximately $2,023, implying around 21% annualized returns. The mid-case’s roughly 19% IRR sits in a range where the stock is meaningfully undervalued at $428 if the backlog-supported demand outlook holds through 2027.

Is Microsoft Stock a Buy Right Now?

The analyst consensus is strongly bullish: 40 Buy ratings, 13 Outperforms, and 3 Holds as of June 4, with a mean target of $561 implying around 31% upside from the current price of $428.

TIKR’s mid-case model projects approximately $872 by June 2030, or roughly 104% total return.

The stock looks undervalued for investors with a multi-year horizon who believe Azure demand remains capacity-constrained rather than demand-constrained.

What Is the Price Target for MSFT Stock?

The Street mean target for Microsoft stock is $561 as of June 4, 2026, with the high target at $870 and the low at $400.

TIKR’s model places the mid-case at approximately $872 by June 2030. The 55.00 analyst count on TIKR reflects strong coverage breadth, with 53 of those analysts maintaining a Buy or Outperform rating.

Should You Invest in Microsoft Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Microsoft Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Microsoft Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze X stock on TIKR for Free →