Key Stats

- Current Price: ~$350

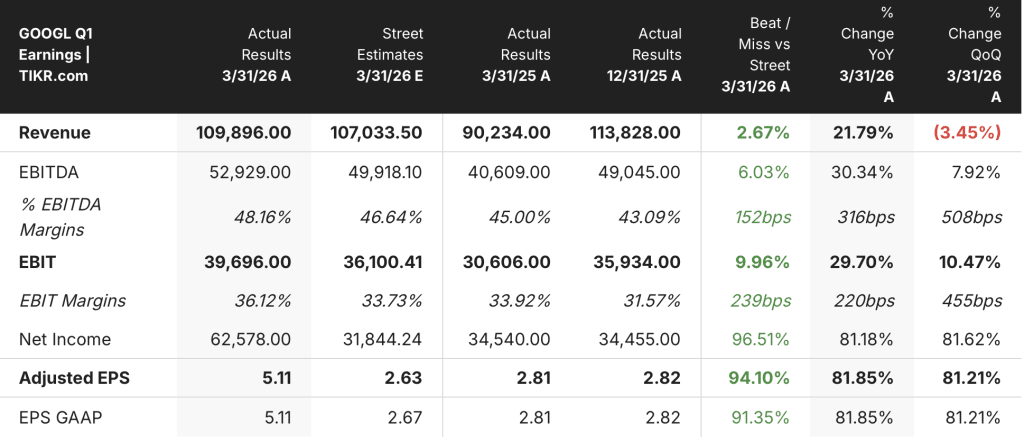

- Q1 2026 Revenue: $109.9B, up 22% YoY

- Q1 2026 EPS (GAAP): $5.11, up 82% YoY

- Google Cloud Revenue: $20B, up 63% YoY

- Google Search & Other Revenue: $60.4B, up 19% YoY

- Operating Income: $39.7B, up 30% YoY; operating margin 36%

- TIKR Model Price Target: ~$563 (mid-case, realized 12/31/30)

- Implied Upside: ~61% over approximately 5 (~11% annualized)

What Happened?

Alphabet Q1 2026 Earnings Breakdown

Alphabet stock (GOOGL) reported Q1 2026 revenue of $109.9B, up 22% year-over-year, marking the company’s 11th consecutive quarter of double-digit revenue growth.

EPS came in at $5.11, up 82% from $2.81 in the prior-year quarter, though net income was heavily lifted by unrealized gains in Alphabet’s nonmarketable equity securities portfolio, according to CFO Anat Ashkenazi on the Q1 2026 earnings call.

Google Cloud was the standout segment, with revenue accelerating to $20B, up 63% year-over-year, exceeding the $20B threshold for the first time.

Cloud operating income tripled year-over-year to $6.6B, with operating margin expanding from 18% in Q1 2025 to 33% in Q1 2026, according to Ashkenazi on the Q1 2026 earnings call.

Google Search & Other delivered $60.4B in revenue, up 19%, driven by strength in retail and financial services verticals.

YouTube advertising revenue grew 11% to $9.9B, with direct response advertising as the primary driver, while network advertising revenue declined 4% to $7B.

Subscription, Platforms and Devices revenue grew 19% to $12.4B, fueled by YouTube Premium and Google One AI plan adoption, with total paid subscriptions reaching 350 million, according to CEO Sundar Pichai on the Q1 2026 earnings call.

Google Cloud’s backlog nearly doubled sequentially to $462B at quarter end, driven by enterprise AI demand and the inclusion of TPU hardware agreements, with just over 50% of the backlog expected to convert to revenue within 24 months, according to Ashkenazi on the Q1 2026 earnings call.

CapEx was $35.7B in the quarter, with full-year 2026 guidance raised to $180B to $190B following the Intersect acquisition close.

Other Bets posted revenue of $411M and an operating loss of $2.1B, with Verily deconsolidated after an external capital raise in Q1.

Alphabet Stock Financials: Margin Expansion Continues

Alphabet stock’s income statement tells a clear operating leverage story: revenue has accelerated materially while margins have expanded at both the gross and operating line over the past two years.

Gross margin held in a tight range through 2024, moving between 58% and 59%, before stepping up to approximately 60% across the last three quarters of 2025.

Operating margin moved from 32% in Q1 2024 to 34% in Q1 2025, and has now reached 36% in Q1 2026, according to Ashkenazi on the Q1 2026 earnings call.

Operating income grew from $25.5B in Q1 2024 to $30.6B in Q1 2025 to $39.7B in Q1 2026, a 56% cumulative increase over two years.

Revenue growth itself has re-accelerated meaningfully: total revenues rose from 12% YoY growth in Q4 2024 to 22% YoY growth in Q1 2026, a sequence that supports the margin expansion rather than working against it.

The near-term headwind to watch is depreciation pressure: Ashkenazi explicitly flagged that higher CapEx will flow through as increased depreciation and data center operating costs, and the Wiz acquisition is expected to weigh on Cloud operating margin by a low single-digit percentage point for the remainder of 2026.

What Does the Valuation Model Say?

The TIKR model prices Alphabet stock at ~$563 in the mid-case, against a current price near $350, implying roughly 61% upside over approximately 4.7 years at ~11% annualized.

The mid-case model assumes a 12.8% revenue CAGR and a 32.6% net income margin from 2025 through 2035, a profile that Q1 2026 actively supports given the Cloud acceleration and operating margin expansion already visible in the numbers.

The risk/reward picture has shifted modestly in favor of bulls this quarter: Cloud revenue grew faster than most prior-quarter run rates would have implied, backlog nearly doubled sequentially, and margins expanded despite rising CapEx, all of which compress the downside to the model’s key assumptions.

The investment case for Alphabet stock is measurably stronger after this quarter than before it.

The real question for Alphabet stock is whether Cloud margin can continue expanding even as CapEx and depreciation accelerate sharply into 2027.

What Has to Go Right

- Cloud operating margin held at 33% in Q1 2026, up from 18% in Q1 2025, demonstrating that AI revenue growth is already absorbing higher infrastructure costs at scale

- The $462B backlog with just over 50% converting in the next 24 months provides multi-year revenue visibility that supports continued margin durability

- Search revenue grew 19% despite AI integration concerns, and queries are at an all-time high, removing the single biggest structural risk that has weighed on Alphabet stock’s multiple

- Gemini Enterprise paid monthly active users grew 40% quarter-over-quarter, with AI solutions becoming the largest contributor to Cloud growth for the first time

What Could Still Go Wrong

- 2027 CapEx is guided to increase significantly above $180B to $190B, with no floor stated, and the depreciation drag will be heavier and sustained across both Cloud and Google Services margins

- Cloud operating margin faces a known headwind from the Wiz acquisition for the remainder of 2026, and integration execution risk is not yet resolved

- Network advertising revenue declined 4% in Q1, a structural signal that the lower-margin, third-party ad business continues to shrink

- TPU hardware revenues will fluctuate quarter-to-quarter with no predictable cadence, adding noise to Cloud margin and revenue comparisons beginning in 2027

Should You Invest in Alphabet Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GOOGL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze GOOGL stock on TIKR for Free →