Key Stats

- Current Price: $104

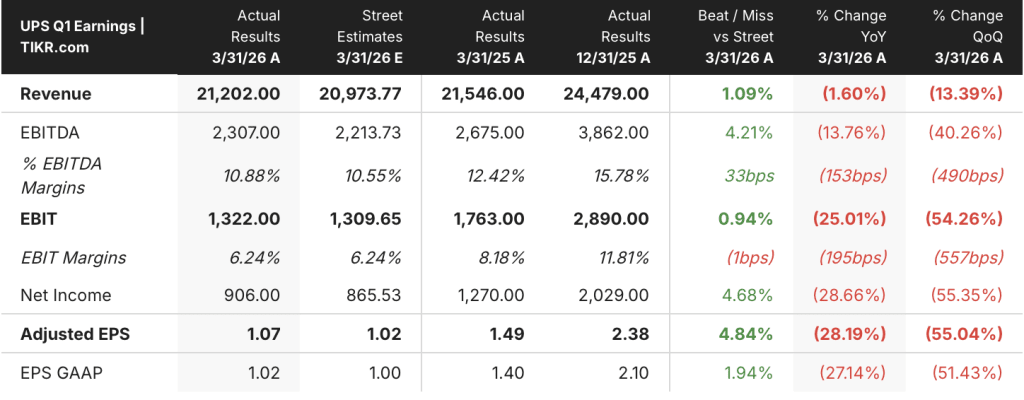

- Q1 2026 Revenue: $21.2B (down 1.6% YoY from $21.5B in Q1 2025)

- Q1 2026 Adjusted EPS: $1.07 (down 28% YoY from $1.49 in Q1 2025)

- Full-Year 2026 Revenue Guidance: ~$89.7B (reaffirmed)

- Full-Year 2026 Operating Margin Guidance: ~10% (reaffirmed)

- Full-Year 2026 EPS Guidance: Approximately flat to 2025

UPS Stock Posts a Beat, But the Real Story Is What Comes Next

United Parcel Service stock (UPS) came into Q1 2026 carrying heavy transformation weight, and the quarter delivered results above internal expectations despite $350M in one-time transitional costs dragging the headline numbers.

Consolidated revenue reached $21.2B, down 1.6% from $21.5B in Q1 2025, while adjusted EPS came in at $1.07 versus $1.49 in the prior-year quarter.

The U.S. Domestic segment generated $14.1B in revenue, a 2.3% decline year-over-year, as an 8% drop in average daily volume (roughly two-thirds tied to the deliberate Amazon glide-down) was partially offset by 6.5% revenue per piece growth.

SMB average daily volume rose 1.6% year-over-year, with SMB penetration hitting 34.5% of total U.S. volume, the highest level in company history, according to CFO Brian Dykes on the Q1 2026 earnings call.

The International segment grew revenue to $4.5B, up 3.8% from the prior-year quarter, outperforming the low-single-digit growth the company had guided toward, as revenue quality improvements and SMB penetration exceeding 60% offset a 6% volume decline.

Supply Chain Solutions more than doubled operating profit year-over-year to $206M, with operating margin expanding 450 basis points to 8.1%, driven by healthcare logistics growth and a 19.9% revenue increase in UPS Digital.

The $350M in additional Q1 expense from temporary aircraft leases during the MD-11 fleet retirement, Ground Saver transition costs, weather, and casualty expenses represented a 250 basis point drag on U.S. Domestic operating margin, according to CFO Brian Dykes on the Q1 2026 earnings call.

UPS reaffirmed full-year 2026 guidance of approximately $89.7B in revenue and a 9.6% operating margin, with Q2 U.S. Domestic operating margin guided to a range of 7.5% to 8.5% as transitional costs clear.

The company plans to pay approximately $5.4B in dividends in 2026 and expects free cash flow of approximately $5.5B, including one-time payments for the Driver Choice voluntary buyout program.

Financials: Margin Compression in Transit, Recovery on the Schedule

UPS stock is in the middle of an intentional margin trough, and the income statement shows the full weight of that transition in Q1 2026.

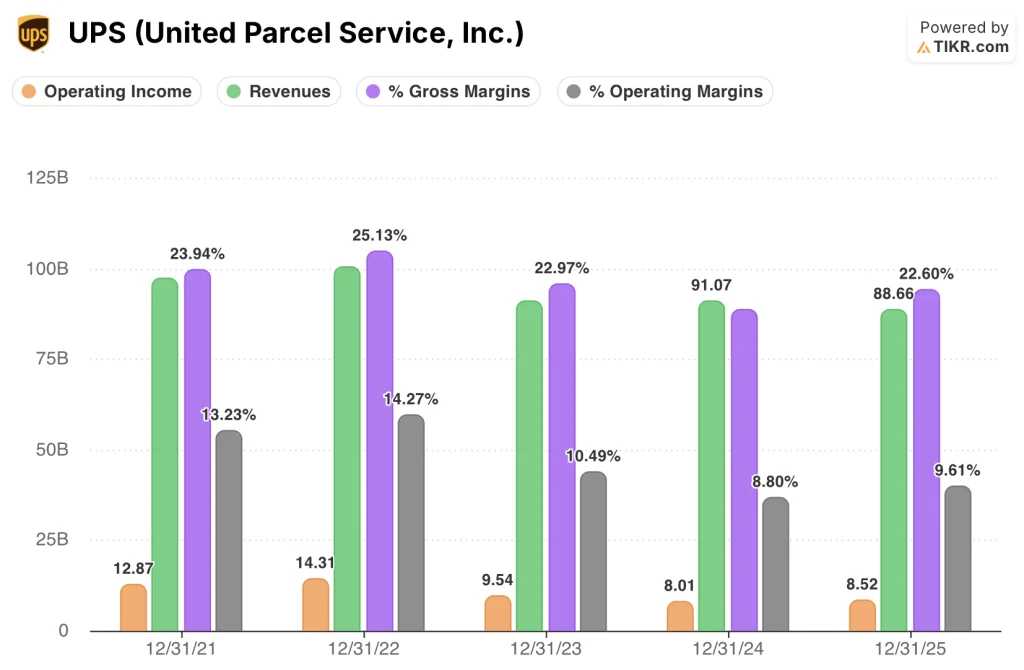

Gross margin fell sharply to 6.3% in Q1 2026, down from 21.6% in Q1 2025, a compression the income statement reflects as a consequence of cost structure misalignment during peak transformation activity rather than a deterioration in pricing or mix.

Operating income dropped to $1.33B in Q1 2026 from $1.79B in Q1 2025, with operating margin contracting to 6.3% from 8.3% over the same period.

The multi-quarter operating margin trend shows a peak of 10.7% in Q4 2025, followed by the Q1 2026 decline to 6.3%, a pattern consistent with the seasonal compression UPS has historically experienced between its strongest and weakest quarters, compounded this cycle by the $350M in transitional costs, according to CFO Brian Dykes on the Q1 2026 earnings call.

Revenue has been range-bound between $21.2B and $21.5B across the last four Q1 periods, with Q1 2026 at the lower end of that band as the Amazon glide-down removes deliberate volume.

Management guided Q2 U.S. operating margin to 7.5% to 8.5%, implying a roughly 120 to 220 basis point sequential recovery as transitional costs roll off, with the full-year 9.6% target requiring a significantly stronger back-half margin profile.

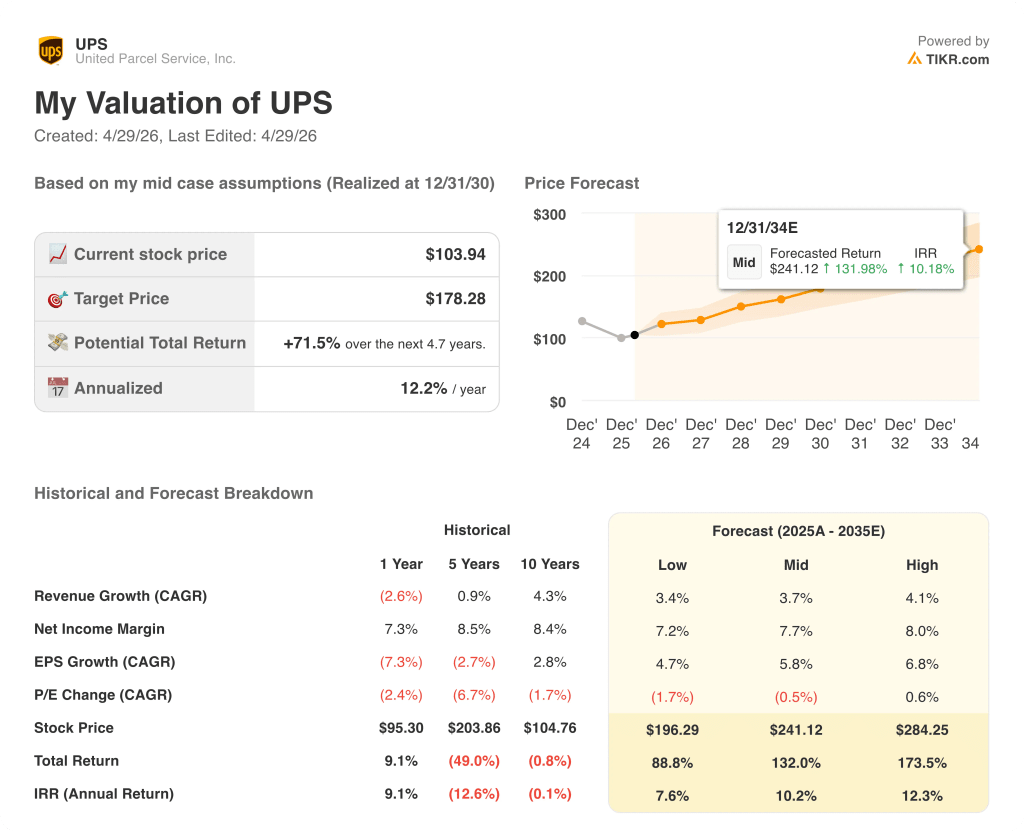

What Does the Valuation Model Say?

The TIKR model prices UPS stock at $178.28, implying 71.5% total upside from the current price of ~$104, or 12.2% annualized over the next 4.7 years.

The mid-case assumptions driving that target are a 3.7% revenue CAGR through 2035 and a 7.7% net income margin, modest assumptions relative to UPS’s 10-year historical net income margin of 8.4% and revenue CAGR of 4.3%.

The Q1 2026 beat and reaffirmed full-year guidance do not materially alter those assumptions, but they do reduce the risk that the transformation stalls before the back-half inflection arrives.

At ~$104, UPS stock is priced closer to the low-case scenario output of $196 than to the mid-case, suggesting the market is discounting execution risk on the 9.6% operating margin target rather than pricing in a normalized earnings trajectory.

The investment case is incrementally stronger after Q1: the $350M cost drag is characterized as resolved, the Driver Choice program was oversubscribed, and the $3B cost-out target remains on track, all of which support the model’s assumption that margins recover meaningfully from current trough levels.

The back-half margin inflection is the entire investment argument for UPS stock: Q1 beat internal targets, but the full-year 9.6% operating margin guide still requires a recovery the company has not yet delivered.

What Has to Go Right

- The Amazon glide-down completes on schedule by June 2026, removing the remaining volume drag and freeing network capacity for premium SMB and B2B growth

- U.S. Domestic operating margin recovers to the guided 7.5% to 8.5% range in Q2 as the $350M in transitional costs (aircraft leases, Ground Saver, weather/casualty) largely rolls off

- The Driver Choice buyout’s 7,500 position reductions (77% exiting April) generate meaningful cost-per-piece improvement in Q3 and Q4, supporting the targeted 50 to 100 basis point RPP-to-CPP spread

- Health care revenue momentum sustains: UPS delivered its first $3B health care revenue quarter in Q1 2026, with double-digit operating margins across all three segments

What Could Still Go Wrong

- A sustained spike in fuel costs from the Middle East conflict pressures International margins below the mid-teens full-year guidance range, as the China-to-U.S. trade lane (the most profitable) was already down 18.3% in Q1 2026

- Consumer confidence at historic lows suppresses small package demand in the back half, undermining the revenue growth ex-Amazon that management expects every quarter

- The de minimis elimination in Europe this summer creates disruption analogous to last year’s U.S. experience, adding network cost without offsetting volume for the International segment

- Q1 2026 gross margin collapsed to 6.3% from 21.6% a year earlier; any delay in normalizing the cost structure risks a full-year operating margin that falls short of the 9.6% target with limited remaining quarters to recover

Should You Invest in United Parcel Service, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UPS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Parcel Service, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UPS stock on TIKR for Free →