Key Stats for Procter & Gamble Stock:

- 52-Week Range: $19.74 to $91.45

- Current Price: $23.14

- Street Mean Target: ~$31 TIKR

- Model Target (Mid): ~$44

- Earnings Date: May 7, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Procter & Gamble’s Q3 Fiscal 2026 Earnings: Volume Is Back, But Margins Are Still Under Pressure

Procter & Gamble (PG) makes the products that stock most of the world’s bathroom cabinets and kitchen shelves. Tide, Pampers, Gillette, Head & Shoulders, Oral-B, Bounty. These are not discretionary purchases. They are the daily-use staples that consumers buy through recessions, tariff cycles, and geopolitical uncertainty, which is exactly why P&G has been a cornerstone holding for income and stability-focused investors for decades.

The Q3 fiscal 2026 results were genuinely encouraging on the demand side, with revenue of $21.2 billion, up 7% year over year and beating estimates of $20.5 billion. Adjusted EPS of $1.59 beat the $1.56 estimate. Organic sales climbed 3%, with volume up 2%, the first time in a year that volume has grown across the company. CFO Andre Schulten described the U.S. consumer as “stable,” while acknowledging the continued bifurcation between higher-income shoppers buying bigger pack sizes and budget-conscious consumers stretching their products further.

The margin story is harder to celebrate. Gross margin fell 150 basis points year over year, extending a losing streak now running six consecutive quarters. Tariffs are the primary culprit, expected to cost around $400 million after tax this fiscal year.

Management now guides full-year EPS toward the lower end of its flat-to-4 % growth range. New CEO Shailesh Jejurikar, who took over on January 1, is simultaneously navigating the tariff environment and executing a restructuring targeting around 7,000 non-manufacturing job cuts over two years.

See analysts’ growth forecasts and price targets for Procter & Gamble (It’s free) >>>

P&G’s Cash Generation Is What Long-Term Investors Actually Own

For a business like P&G, the free cash flow chart tells you more than the quarterly earnings table ever could. Over the past five years, P&G has averaged roughly $14.6 billion in annual free cash flow.

The dip to $14 billion in fiscal 2025 reflects increased capital spending tied to the restructuring, not deterioration in the underlying business. Very few companies of any size sustain that level of cash generation across a full economic cycle, and that cash has one primary destination.

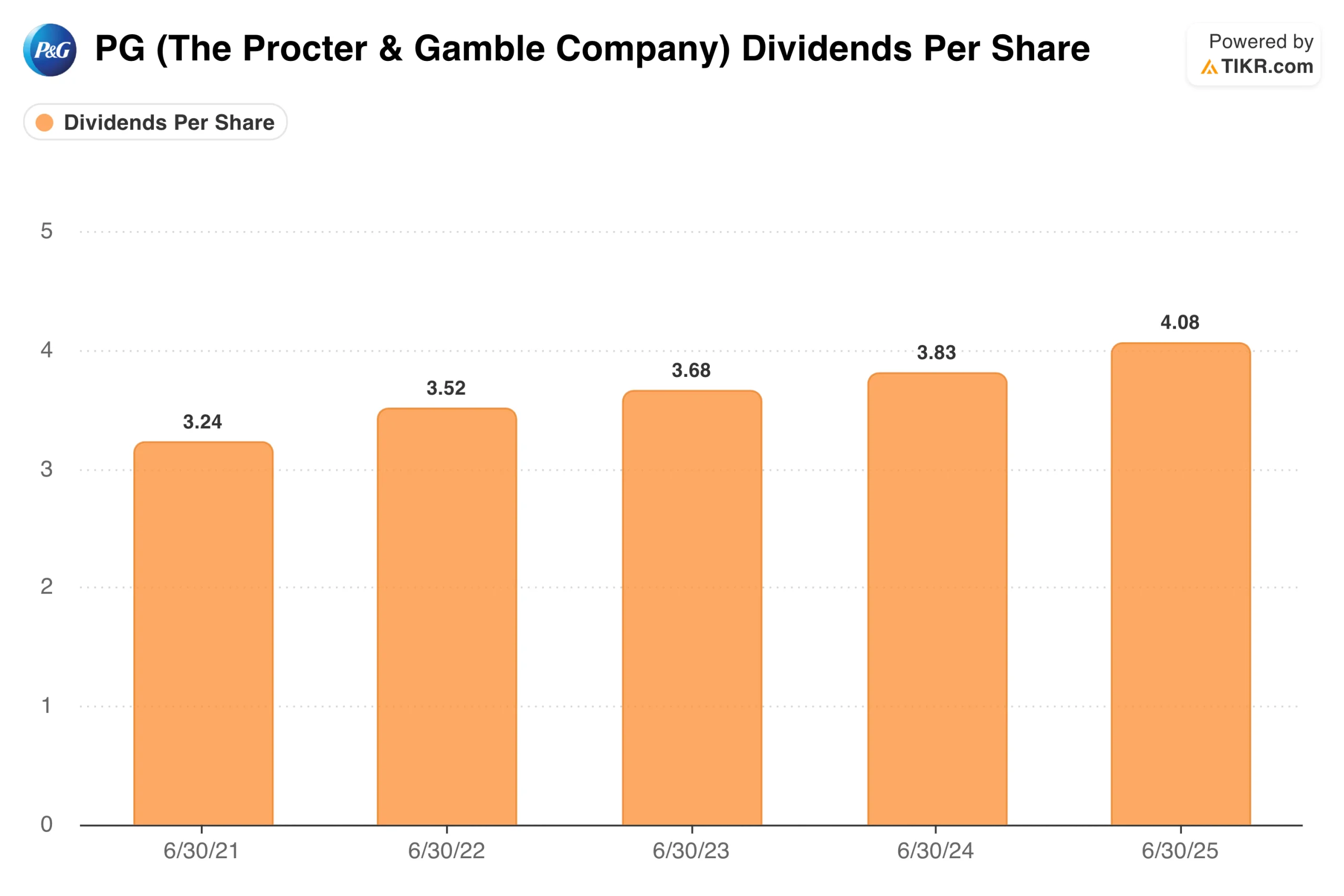

P&G has raised its dividend for 68 consecutive years. Dividends per share have grown from $3.24 in fiscal 2021 to $4.08 in fiscal 2025, a steady climb that has persisted through commodity cycles, pandemic disruptions, and geopolitical headwinds.

The current yield of 3% sits toward the higher end of P&G’s historical range, which is one of the more reliable signals that the stock is not obviously overpriced. Management plans to return around $15 billion to shareholders in fiscal 2026 through dividends and buybacks combined.

On the competitive side, P&G held or grew market share in seven of ten product categories globally over the past year. Private-label competition is not accelerating as it typically does in downturns, which suggests something meaningful about the durability of P&G’s brand positioning against Unilever, Colgate-Palmolive, and Kimberly-Clark.

Procter & Gamble’s Valuation: Pricing in Durability, Not Growth

TIKR’s mid-case model targets around $203 for P&G, assuming around 4% annual revenue growth through 2030 and net income margins holding around 20%. Based on the current price, that implies an approximately 37% total return over roughly 4.2 years, or about 8% annualized. The high case gets you toward $301.

What the Bulls Are Betting On:

- Volume growth sustains. The Q3 print showing volume up 2% for the first time in a year is meaningful if it holds. Sustained volume alongside modest pricing is the combination that drives earnings re-acceleration.

- Tariff headwinds are transitory. Management has levers, including sourcing flexibility, productivity savings, and selective price increases on premium products. If tariff pressure eases in fiscal 2027, the margin compression story reverses.

- The restructuring delivers. P&G has executed similar transformations before. If cost savings translate into margin expansion by fiscal 2027, the earnings trajectory improves meaningfully.

What the Bears Are Watching:

- Six consecutive quarters of gross margin compression is not a short-term story. The bear case is that tariffs, commodity costs, and competition from lower-priced rivals are more structurally challenging than management’s guidance implies.

- The K-shaped consumer is a real risk. Budget-conscious shoppers stretching their detergent and shampoo further directly pressure volume in P&G’s largest categories. If that behavior deepens, organic growth guidance becomes harder to hit.

- The valuation is not obviously cheap. At around 21x forward earnings, P&G is priced for stability and steady compounding. If the earnings recovery takes longer than expected, upside from current levels is limited even with the dividend providing a floor.

Should You Invest in Procter & Gamble?

P&G is the kind of stock that rarely gets exciting but rarely disappoints investors who own it for the right reasons. The free cash flow is durable, the dividend is as reliable as anything in the market, and the brand portfolio has held up through conditions that have broken weaker competitors.

At around $148 with a 3% yield and 68 consecutive years of dividend growth, P&G offers a combination of income and compounding that is genuinely difficult to replicate. Add it to your TIKR watchlist and track gross margin trajectory and volume growth in the upcoming Q4 report as the two metrics that will tell you whether the recovery is on schedule.

Start your own analysis of P&G alongside every other stock on your radar with a free TIKR account.

Analyze Procter & Gamble stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!