Key Takeaways:

- Data Center Boom: 60%+ growth expected in FY2026, fueled by AI infrastructure demand.

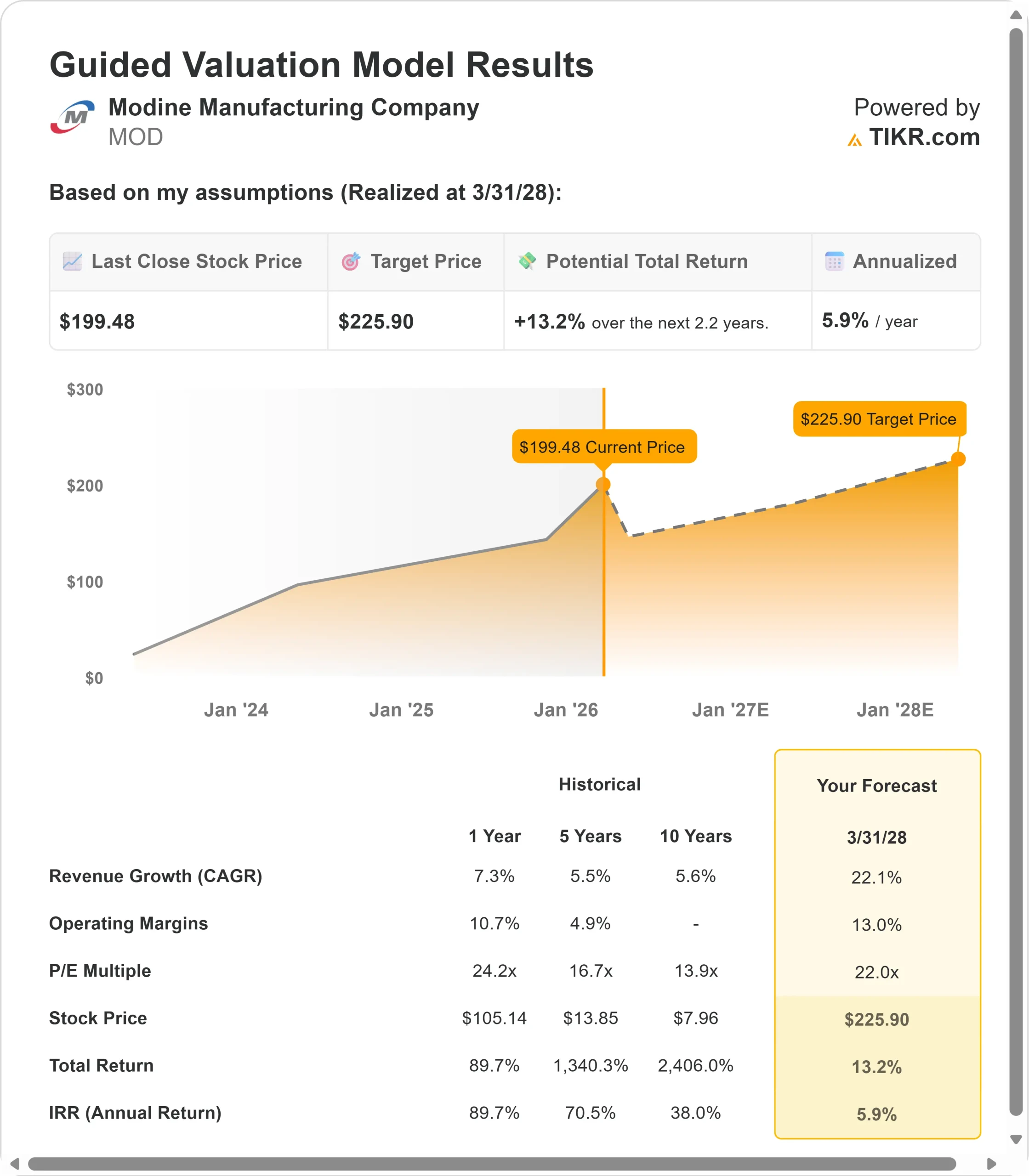

- Price Projection: Based on current execution, MOD stock could reach $226 by March 2028.

- Potential Gains: This target implies a total return of 13% from the current price of $199.

- Annual Return: Investors could see roughly 6% growth over the next 2.2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Modine Manufacturing Company (MOD) is in the middle of its biggest transformation yet. The company is expanding data center production capacity across multiple U.S. facilities while integrating three strategic acquisitions.

In Q2 FY2026, Modine posted 24% revenue growth in its Climate Solutions segment, reaching unprecedented scale in the booming data center cooling market.

CEO Neil Brinker is executing an aggressive capacity expansion centered on AI infrastructure.

- The company now projects data center revenues will exceed $2 billion by fiscal 2028, up from previous guidance.

- Data center sales surged 42% in Q2, with management expecting second-half growth to exceed 90% year-over-year.

Despite this momentum, Modine stock trades at $199, near its peak, but still offers potential upside for investors who recognize the company’s strategic position in data center infrastructure.

See analysts’ full growth forecasts and estimates for MOD stock (It’s free) >>>

What the Model Says for Modine Stock

We analyzed Modine’s transformation into a leading thermal management provider for AI data centers, leveraging unmatched manufacturing scale.

- The company is rapidly expanding beyond traditional HVAC products.

- Modine now operates chiller production lines in Grenada, Mississippi, with additional facilities planned in Franklin, Wisconsin; Jefferson City, Missouri; and Grand Prairie, Texas.

- The company has also established production in Chennai, India, and is expanding capacity in the U.K. to serve global hyperscaler and colocation customers.

- With AI infrastructure investments accelerating globally, Modine is capturing demand as data centers increasingly require sophisticated liquid- and air-cooling solutions.

- The company serves all major hyperscalers and is expanding relationships with neocloud providers.

Using a forecast of 22.1% annual revenue growth and 13% operating margins, our model projects the stock will rise to $226 within 2.2 years. This assumes a 22x price-to-earnings multiple.

That represents compression from Modine’s historical P/E averages of 24.2x (one year) and 16.7x (five years). The lower multiple acknowledges near-term margin pressure from capacity expansion costs and integration challenges from recent acquisitions.

The real value lies in successfully ramping production capacity while maintaining customer relationships and expanding into modular data center solutions.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for MOD stock:

1. Revenue Growth: 22.1%

Modine’s growth centers on explosive data center expansion. The company achieved 42% organic growth in data center sales for Q2 and expects full-year growth exceeding 60%.

Management has increased visibility, with order windows extending three to five years for major customers.

- The company has hired 1,200 employees to support data center operations this year and is launching multiple production facilities simultaneously.

- Beyond the current $2 billion target, Modine is building capacity to produce significantly more as AI infrastructure demand continues accelerating.

- Recent acquisitions of AbsolutAire, L.B. White, and Climate by Design International add breadth to the HVAC Technologies portfolio.

- The company is applying its proven 80-20 principles to drive value through margin improvement and cross-selling opportunities.

2. Operating margins: 13%

Modine faces temporary margin pressure as it scales operations.

The company delivered an adjusted EBITDA margin of 14% in Q2, down from normal levels due to significant launch costs.

Management incurred $10-12 million in additional labor and overhead expenses to build out new production lines and train the workforce.

These inefficiencies are temporary. As new facilities ramp to full production in Q4 FY2026 and beyond, margins should normalize and eventually exceed historical levels.

Management expects Q4 margins to approach 20%+ as volume leverages fixed costs. The company’s mature data center facilities already operate at or above segment-average margins.

3. Exit P/E Multiple: 22x

The market values Modine at 35.1x earnings currently. We assume the P/E will compress to 22x over our forecast period.

Near-term execution risk from simultaneous facility launches and acquisition integration weighs on the multiple. The company must successfully train thousands of new employees while maintaining quality and meeting customer delivery schedules.

However, as production stabilizes and Modine demonstrates it can deliver at scale, the company should command a premium multiple. The expanding relationships with all major hyperscalers and proven thermal management expertise provide a strong competitive moat.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Thermal management companies face execution risks and capital spending cycles. Here’s how Modine stock might perform under different scenarios through March 2028:

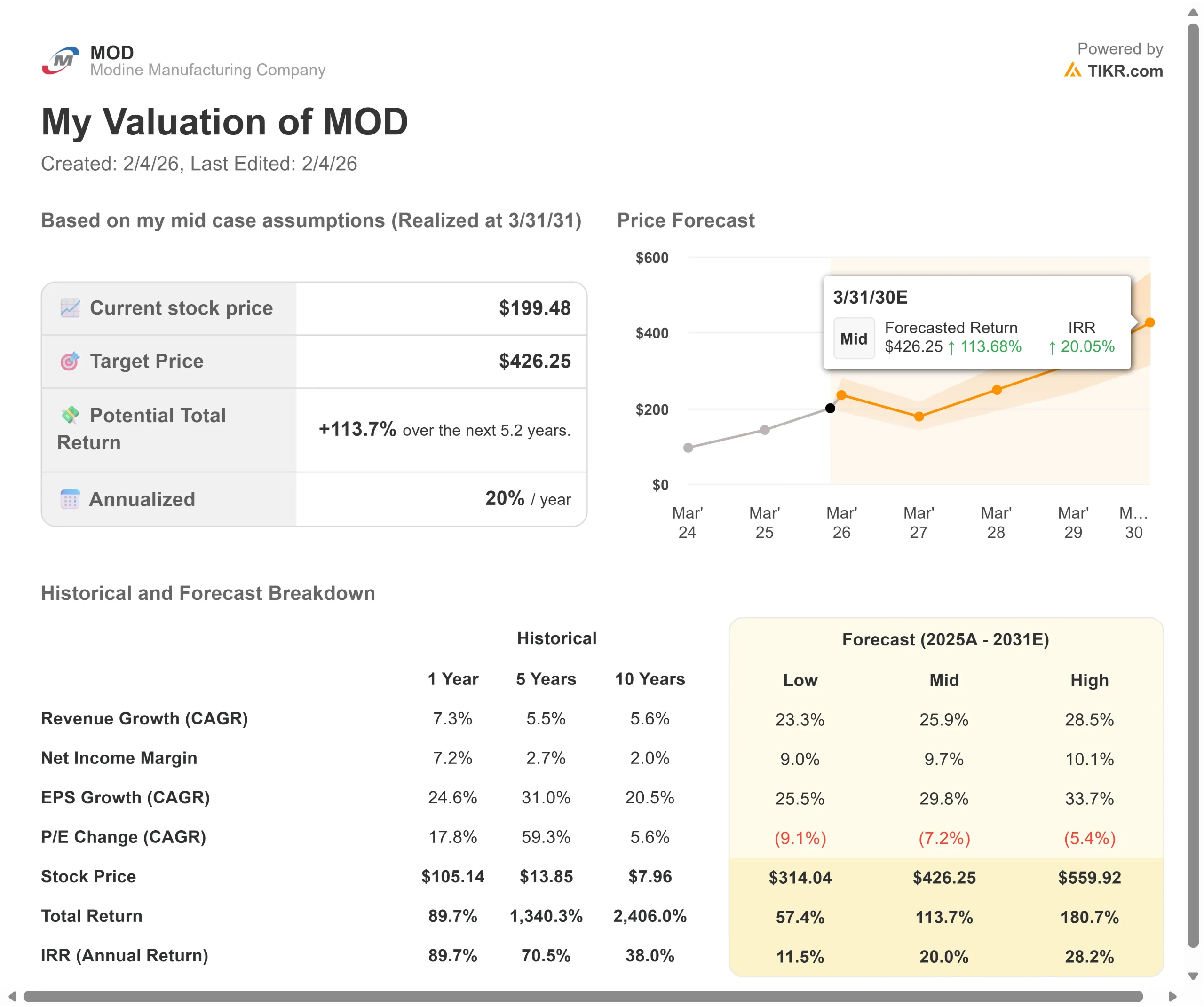

- Low Case: If revenue growth slows to 23.3% and net income margins compress to 9%, investors still see a 57% total return (11.5% annually).

- Mid Case: With 25.9% growth and 9.7% margins, we expect a total return of 114% (20% annually).

- High Case: If AI infrastructure accelerates and Modine maintains 10.1% margins while growing at 28.5%, total returns could reach 181% (28.2% annually).

See what analysts think about MOD stock right now (Free with TIKR) >>>

The range reflects execution on capacity expansion, successful integration of acquisitions, and margin improvement as new facilities reach full production.

In the low case, launch delays or integration challenges emerge.

In the high case, AI infrastructure demand exceeds expectations, and margins improve ahead of schedule as production efficiency accelerates.

How Much Upside Does Modine Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!