Key Stats for Alibaba Stock

- Current Price: $129.47

- Target Price (Mid): ~$207

- Street Target: ~$191

- Potential Total Return: ~60%

- Annualized IRR: ~10% / year

- Earnings Reaction: -3.22% (May 13, 2026)

- Max Drawdown: 36.77% (April 7, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

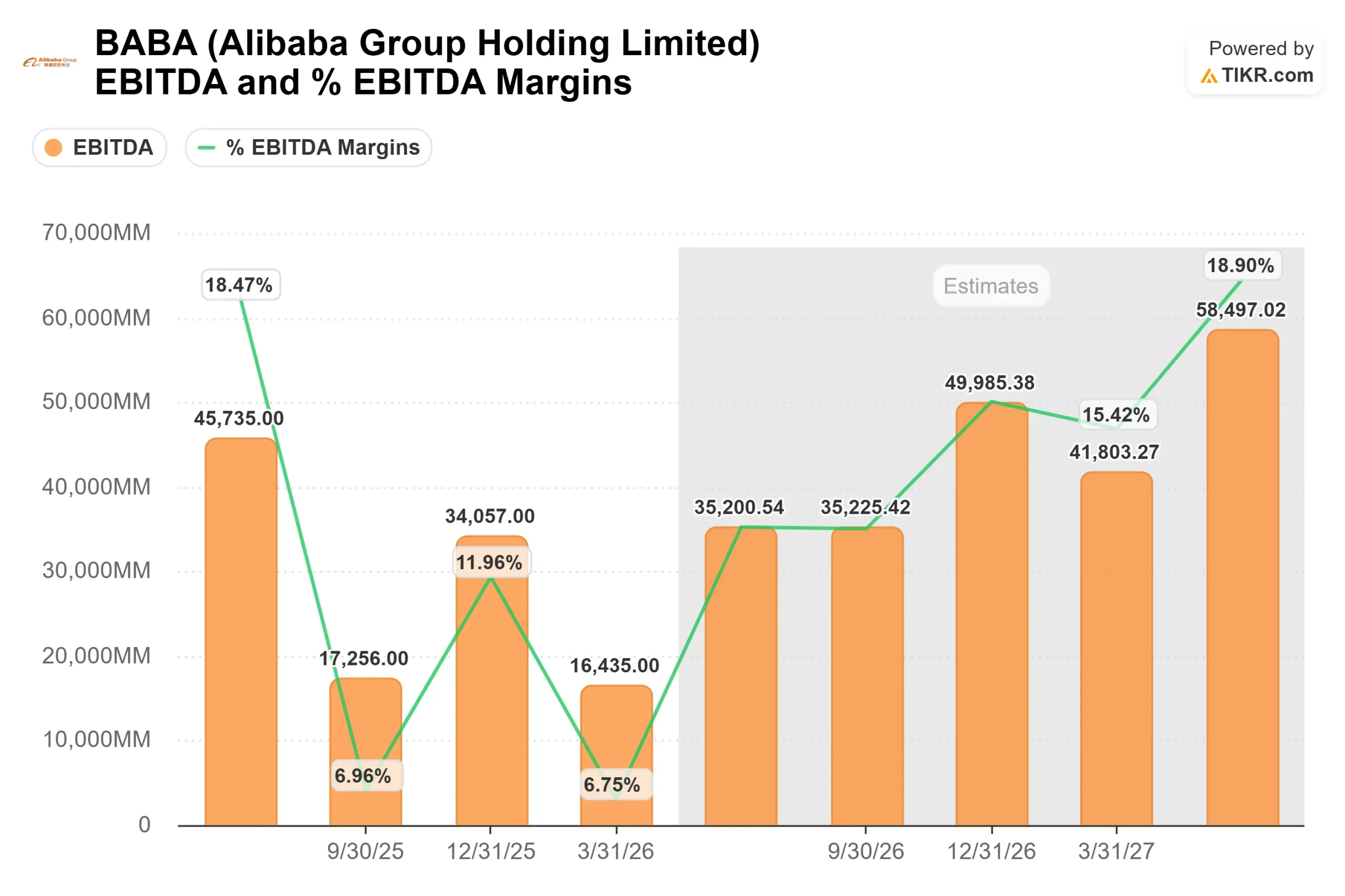

Alibaba Group Holding (BABA) reported Q4 FY2026 earnings on May 13, 2026, and the headline numbers were hard to look at. Adjusted EBITA fell 84% year over year. Free cash flow swung to an RMB 17.3 billion outflow. The company posted an operating loss of RMB 848 million, its first since 2021. The stock fell 3.22% on the day and has since settled at $129.47, roughly 33% below its 52-week high of $192.67.

That is the bear case. But inside the same report, Cloud Intelligence Group external revenue accelerated to 40% growth, and AI-related product revenue hit triple digits for the eleventh consecutive quarter. Those two stories, sitting in the same earnings release, are why the market has not reached a verdict.

The Profit Collapse Was Intentional

The 84% EBITA decline was not a sign of a business in distress. It was management executing a stated plan.

CFO Toby Xu told analysts directly on the earnings call: the negative free cash flow is “primarily due to the very significant investments we’ve been making in AI over the past year,” and the company plans to maintain that intensity for the next two years. CEO Eddie Wu framed the logic as building two parallel factories, one for AI training and one for AI inference, both requiring upfront capital before they generate returns. His specific claim: there is not a single idle card on Alibaba’s servers. Demand exists. The question is whether the monetization timeline holds.

The losses are concentrated and bounded. Quick commerce, which grew revenue 57% to RMB 20 billion this quarter, is still loss-making. Management confirmed unit economics improved quarter over quarter, with the target for unit economics to turn positive by the end of fiscal year 2027. The Qwen consumer AI app also drove significant investment spending in the quarter. Excluding quick commerce losses entirely, management noted that China e-commerce EBITA would have been stable year over year.

See historical and forward estimates for Alibaba stock (It’s free!) >>>

The Cloud Numbers That Change the Calculus

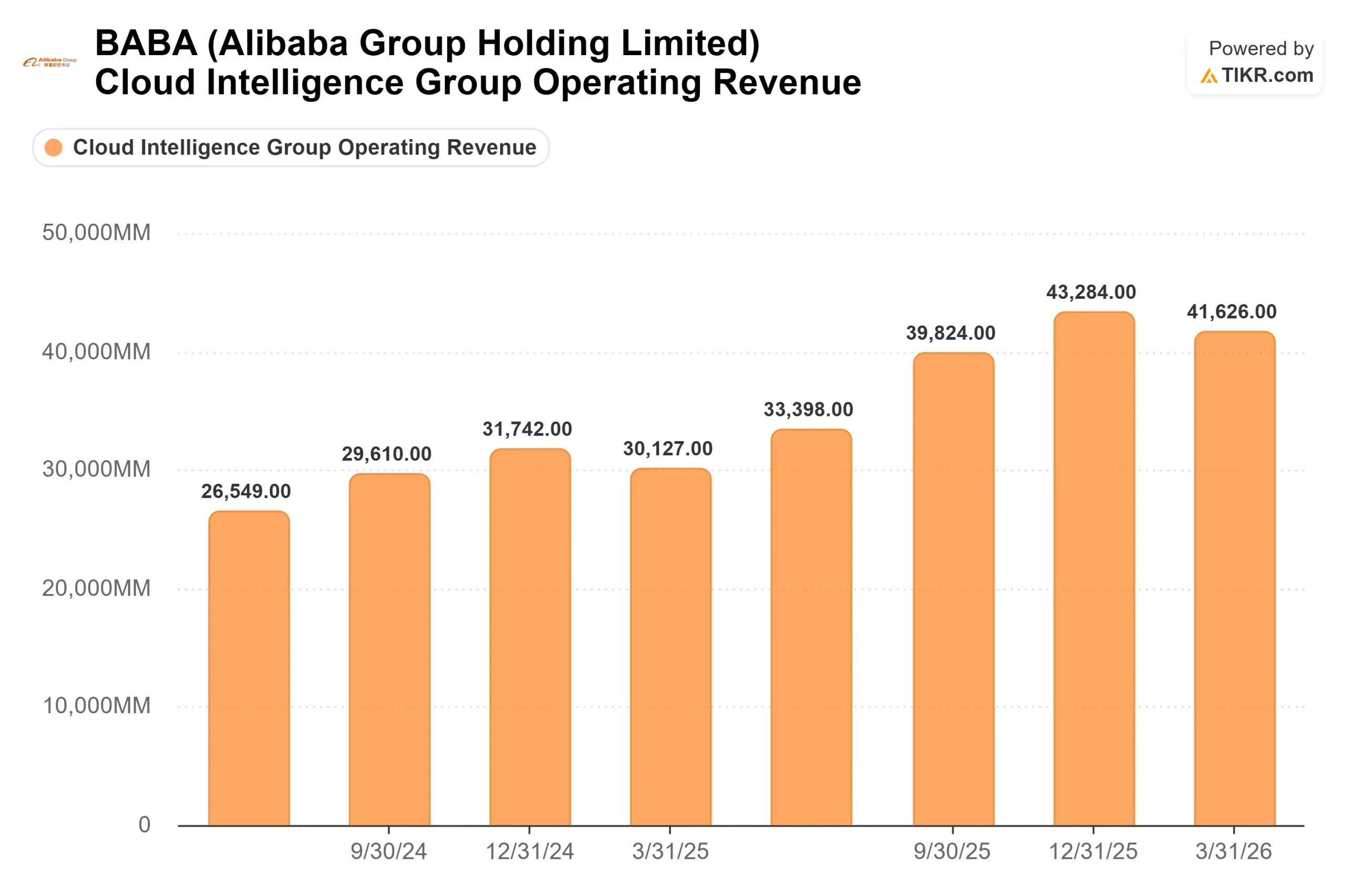

Cloud Intelligence Group revenue reached RMB 41.6 billion (approximately $6 billion) in the March quarter, up 38% year over year per Alibaba’s official earnings release. External revenue, which reflects actual competitive demand rather than internal Alibaba billing, grew 40%. AI-related products now account for 30% of that external revenue and have posted triple-digit growth for eleven straight quarters.

CEO Wu disclosed on the call that model and application services ARR has already crossed RMB 8 billion and is on track to exceed RMB 10 billion this quarter. He set a specific public target: RMB 30 billion in model and application services ARR by the end of calendar year 2026. That number is now measurable at the next earnings call.

Two days before earnings, Alibaba announced the full integration of its Qwen AI assistant into Taobao and Tmall, per the South China Morning Post reporting on May 11, 2026. Consumers can now browse, compare, and buy from a catalog of over 4 billion products via conversational chat rather than keyword search. This matters financially because MaaS (Model-as-a-Service, meaning revenue from API access to AI models) carries structurally higher gross margins than traditional cloud compute. As MaaS grows as a share of Cloud revenue, margins expand. One data point from the call captures the scale of what is already happening: token consumption on Alibaba’s Model Studio platform grew more than 10x between November 2025 and May 2026.

What the Valuation Says

At $129.47, BABA trades at 19.08x NTM P/E and 12.88x NTM EV/EBITDA, per TIKR. The mean Street target sits at approximately $191, around 48% above current levels per TIKR’s own Target/Close ratio. The analyst breakdown as of May 26, 2026: 30 Buys, 8 Outperforms, 2 Holds, 1 Underperform, 0 Sells. JP Morgan reaffirmed Overweight on May 14, 2026, the day after earnings, with a $205 target.

The balance sheet provides the runway. Alibaba held approximately $38 billion in net cash as of March 31, 2026, per CFO Xu on the earnings call. The Board also approved an annual dividend of $1.05 per ADS for fiscal year 2026, yielding around 0.9% at current prices per TIKR.

The geopolitical risk is real and should not be dismissed. BABA hit its max drawdown of 36.77% on April 7, 2026, during the U.S.-China tariff escalation. In February 2026, the Pentagon briefly listed Alibaba among alleged military-linked companies, then withdrew it the same day, yet the stock still fell roughly 3% in Hong Kong before any facts emerged. That pattern is permanent. Investors who cannot hold through those moments should not own this stock, regardless of the fundamentals.

See how Alibaba performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $129.47

- Target Price (Mid): ~$207

- Potential Total Return: ~60%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Alibaba stock (It’s free!) >>>

The TIKR mid-case model assumes a revenue CAGR of around 10% through March 2031 and a net income margin expanding to around 12%. Two drivers support that revenue growth: Cloud Intelligence Group sustaining above-market acceleration as AI product revenue approaches 50% of external revenue, and quick commerce scaling toward profitability as unit economics normalize. The primary margin driver is the MaaS mix shift, as higher-margin AI model revenue displaces traditional compute in the Cloud segment.

The high case reaches approximately $325 by the same date, implying around 151% total return, if AI monetization accelerates and T-Head chip deployment drives faster gross margin expansion. The downside case of approximately $193 still implies a modest positive return, but reflects a world where quick commerce losses persist beyond guidance and geopolitical friction further compresses valuation multiples.

The central risk is not that the AI business fails. It is that the timeline extends. If the MaaS revenue ramp takes two years instead of one, the free cash flow trough deepens before it recovers, and patience becomes the real variable.

Conclusion

Watch Q1 FY2027 earnings, expected around August 2026. Two numbers will tell you whether this thesis is holding. Cloud external revenue needs to remain at or above 40% growth. The model and application services ARR need to track toward CEO Wu’s stated target of RMB 30 billion by year-end 2026. If both hold, the investment cycle is delivering on its stated logic. If Cloud decelerates meaningfully or ARR disappoints, the narrative shifts from productive investment to margin destruction with an unclear payoff date, and the stock will reprice.

At $129.47, with the Street sitting roughly 48% above current levels and the TIKR mid-case implying around 60% total return to March 2031, the setup is clear. August is when the data confirms it or doesn’t.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alibaba?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alibaba, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alibaba alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alibaba on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!