Key Stats for Generac Stock

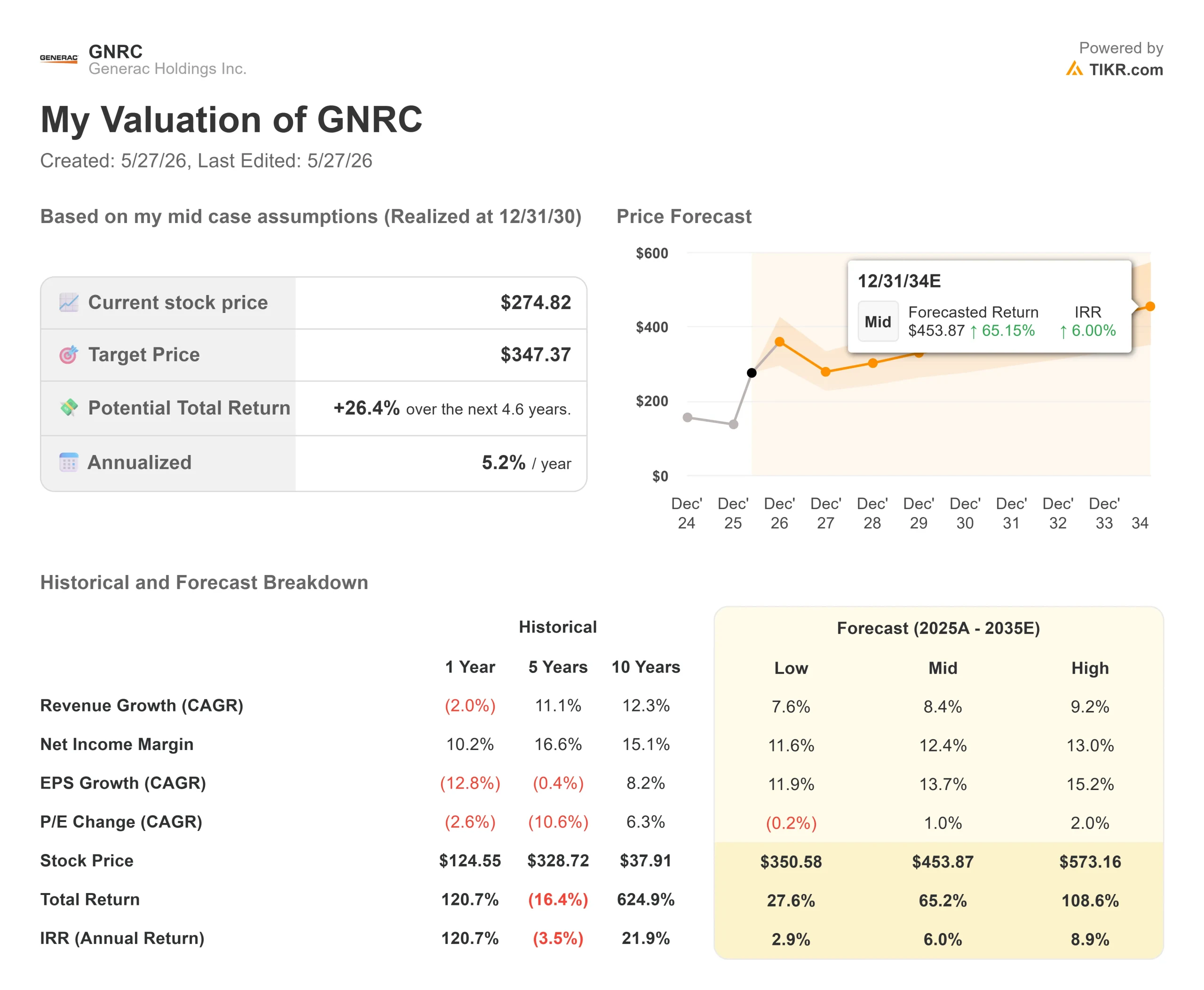

- Current Price: $274.82

- TIKR Target Price (Mid): ~$347

- TIKR Total Return (Mid): ~26%

- Annualized IRR (Mid): ~5% / year

- Street Target (Mean, 5/26/26): ~$277

- Earnings Reaction (Q1 2026, reported 4/29/26): +2.49%

- Max Drawdown: -32.77% on 12/31/25

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Generac Holdings Inc. (GNRC) has spent most of 2026 making skeptics look wrong. On May 22, Jefferies upgraded GNRC from Hold to Buy and raised its price target to $302, sending shares up roughly 9% that day. The move came five weeks after a Q1 earnings call that, read carefully, explains exactly why Jefferies acted when it did.

The debate among investors is not whether Generac is winning in data centers; it clearly is. The real question is whether a stock that had already surged before the upgrade can keep climbing before a hyperscale contract is formally signed.

What Jefferies Saw and What the Q1 Transcript Confirms

Jefferies analyst Tanner James cited accelerating AI-driven data center demand and growing adoption of Generac’s Baudouin engines among hyperscale operators. He described the setup as offering an “asymmetric positive risk-reward profile,” with a major supply agreement potentially imminent. Part of his thesis rests on permitting documents tied to the Stargate AI infrastructure project in Abilene, Texas, which reportedly reference Baudouin engines supplied exclusively in the U.S. through Generac. Jefferies noted those filings do not directly confirm Generac’s involvement but argued they indicate market acceptance of the engine technology.

The Q1 transcript adds the most important context. On the April 29 earnings call, CEO Aaron Jagdfeld described the status of the $600 million nonbinding notice to proceed from a hyperscale customer this way: “If this was a 100-yard dash, we’re like 99 yards of the way done with the race.” He said Generac had already moved into site-level discussions for specific 2027 facilities, not just negotiating contract terms.

That is a different place than where Generac stood at its March Investor Day, when the stock fell as much as 12% because no formal contract was announced. By Q1 earnings, the business had already delivered. The C&I (Commercial & Industrial) segment grew 28% year over year to $510 million. Adjusted EBITDA beat the average analyst estimate by 20.83%, coming in at $193 million or 18.3% of net sales. The stock rose 2.49% on the day results were reported.

See historical and forward estimates for Generac stock (It’s free!) >>>

The $700 Million Backlog and What It Doesn’t Include

The most important detail about Generac’s $700 million C&I backlog is what it excludes. That figure does not include the $600 million nonbinding notice to proceed. CFO York Ragen said the backlog “provides visibility through 2027, even before considering the significant expected contribution from other hyperscale-related opportunities.” The $300 million backlog increase came in roughly ten weeks, between mid-February and the April 29 call.

Beyond the headline customer, Jagdfeld confirmed Generac is in “final stages of vendor approval with two hyperscale data center customers,” with the second “close behind.” Each represents potential significant volume in 2027 and 2028. To prepare, Generac’s new Sussex, Wisconsin, facility is on track for production in the second half of 2026, targeting domestic manufacturing capacity exceeding $1 billion by Q4. Jagdfeld acknowledged they are already thinking beyond that: “We need a bigger boat if we’re going to win both of these accounts.”

Management raised full-year C&I net sales guidance to the mid- to high 20% range, up from the low to mid-20% range at Investor Day, driven by data center, telecom, and rental markets, plus the Enercon acquisition.

The Enercon Acquisition and Residential Recovery

The April 1 Enercon closing funded at $122 million ($77 million cash, $45 million stock) does more than add revenue. Enercon manufactures generator enclosures and switchgear, the components that package large megawatt generators into finished systems for data center installations. Jagdfeld explained the logic directly: “Even if we can get great lead times on the unpackaged product, it doesn’t help us if the packaging phase is constrained.” Ragen quantified the impact: Enercon adds approximately 50 basis points to C&I segment gross margins through vertical integration, a benefit that compounds as data center volumes scale.

On the Residential side, ecobee Generac’s smart home energy platform crossed 5 million connected homes and posted its first positive adjusted EBITDA in a seasonally soft quarter. The dealer network exceeded 9,500. Energy technology EBITDA breakeven remains on track for 2027, per Ragen.

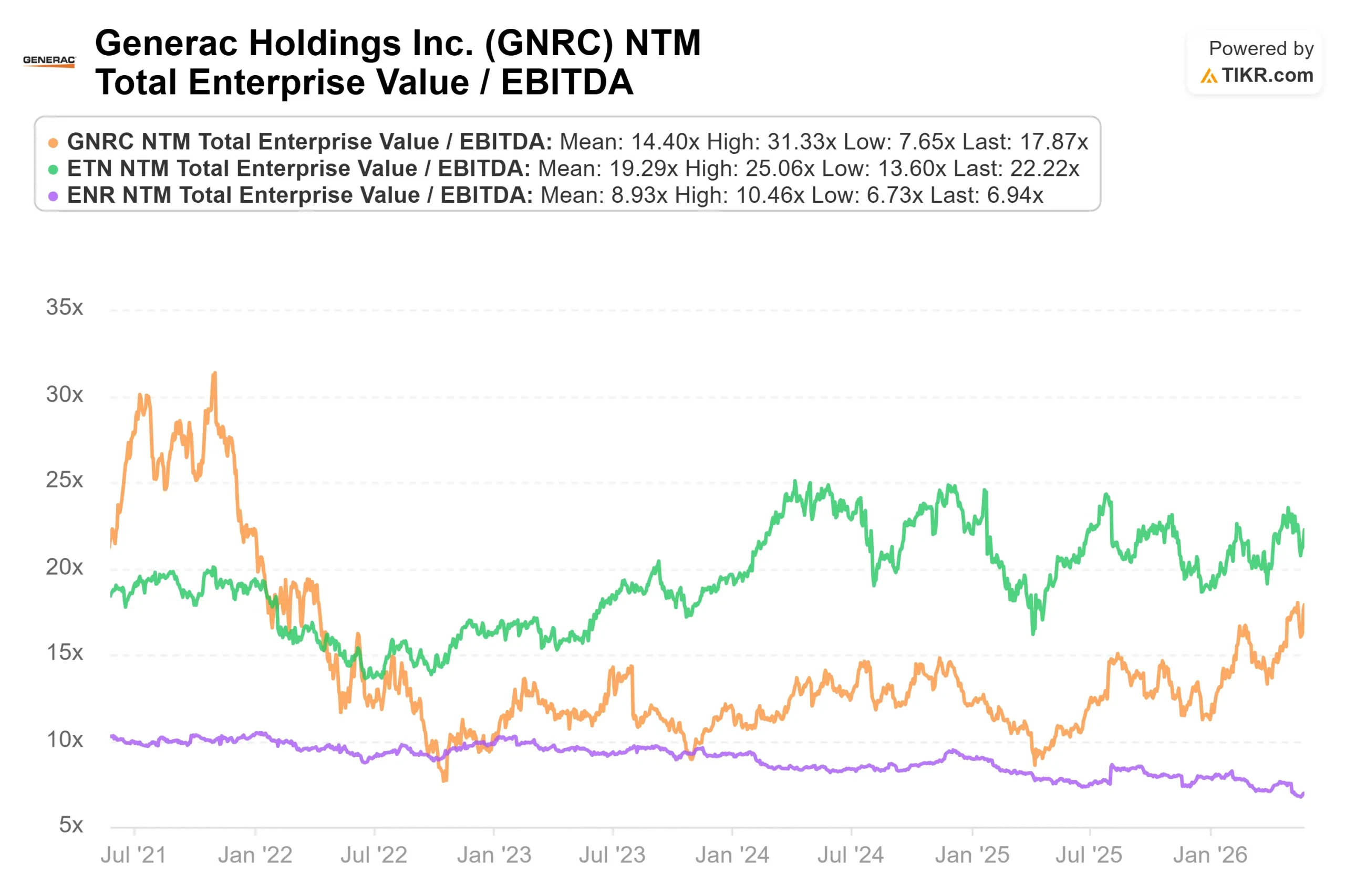

On relative valuation, TIKR’s Competitors data shows Generac at 17.9x NTM EV/EBITDA below Eaton Corporation (ETN) at 22.2x but roughly in line with Siemens Energy (ENR) at 18.8x, despite more direct data center backup power exposure than either. On NTM P/E, Generac at 30.0x sits between Siemens Energy at 34.9x and Eaton at 28.6x. The gap to Eaton narrows quickly if hyperscaler contracts land and C&I margins expand as guided.

See how Generac performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $274.82

- Target Price (Mid): ~$347

- Potential Total Return: ~26%

- Annualized IRR: ~5% / year

See analysts’ growth forecasts and price targets for Generac stock (It’s free!) >>>

The TIKR mid-case assumes an 8.4% revenue CAGR, driven by two things: C&I data center volume converting from backlog to revenue as supply agreements land, and a Residential recovery as power outage activity returns to the long-term baseline in the second half of 2026. The margin driver is operating leverage on the C&I build. Ragen guided toward mid- to high-teens adjusted EBITDA in C&I by 2028. The mid-case assumes a net income margin of around 12%, expanding from 8.9% in 2025.

If both hyperscaler agreements land, the high case around $573 by December 2034 at roughly 9% annualized becomes plausible. If approvals extend without a signed agreement, the premium compresses, and the low case of around $351 by December 2034 at roughly 3% annualized reflects the risk. The Street mean target is currently around $277, sitting just above the current price. Jefferies, as a point of comparison, projects Generac could reach $6.8 billion in 2028 revenue if two hyperscaler agreements land above the current Wall Street consensus.

Conclusion

One metric determines whether this thesis holds at Q2 earnings in late July: the C&I backlog. If it stays above $700 million, the pipeline is replenishing as orders burn down. If it falls, the narrative breaks.

More consequential is whether Generac announces a signed master supply agreement with either hyperscaler. Jagdfeld said they are at the one-yard line. Q2 is the tape.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Generac?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Generac, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Generac alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Generac on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!