Key Stats for Adobe Stock

- This Week Performance: -2%

- 52-Week Range: $251 to $453

- Current Price: $259

What Happened to Adobe Stock?

Adobe (ADBE) shares are trading near their 52-week low of $251, down sharply from a 52-week high of $453.26, as a sector-wide $1 trillion software selloff, Figma’s aggressive AI-powered competitive push, and institutional investors slashing software holdings to their most underweight position since 2021 all converged within the same brutal February window.

The immediate pressure intensified on February 18 when Adobe stock dropped between 2.5% and 5.4% in a single session alongside CrowdStrike, Intuit, and Atlassian, as the S&P 500 Software and Services sector fell 1.7% with more than 90% of its components trading lower on AI disruption fears.

Compounding the selloff, rival Figma jumped roughly 14% on February 19 after forecasting 2026 revenue of $1.36 billion to $1.37 billion, beating estimates by nearly $80 million, and announcing a new AI credit monetization model launching March 2026 that directly targets Adobe’s design software customer base.

The market is actively repricing Adobe from a dominant creative software incumbent to a company now fighting a two-front war, defending its core design business against an AI-native Figma while simultaneously needing to prove its own AI integration justifies a multiple that has more than halved from roughly 44 times forward earnings just one year ago.

Against the panic, however, Coatue Management raised its Adobe stake by 43.2% to 874,150 shares as of December 31, 2025, a notable institutional vote of confidence that stands in direct contrast to Mubadala Investment Co. cutting its Adobe position by 49.0% to 11,570 shares over the same period.

The broader picture for Adobe ultimately hinges on whether its enterprise moat, including active AI partnerships with major clients like Havas, which is using Adobe tools to cut advertising production costs by up to 50%, can withstand the structural pressure that has driven institutional software underweighting to a four-year extreme.

Wall Street’s Take on ADBE Stock

Despite the sector panic wiping Adobe from a 52-week high of $453.26 to a current $258.61, the selloff now sets up a forward story where Adobe’s ability to defend 50%-plus EBITDA margins and grow EPS from $20.94 to a forecast $23.46 in FY2026 becomes the central test.

The fundamental case remains intact underneath the noise, with consensus projecting FY2026 revenue of $26.04 billion (+9.5% YoY), normalized EPS of $23.46 (+12.1% YoY), and net income margins holding at 36.6%, numbers that look difficult to reconcile with a stock sitting near its 52-week floor.

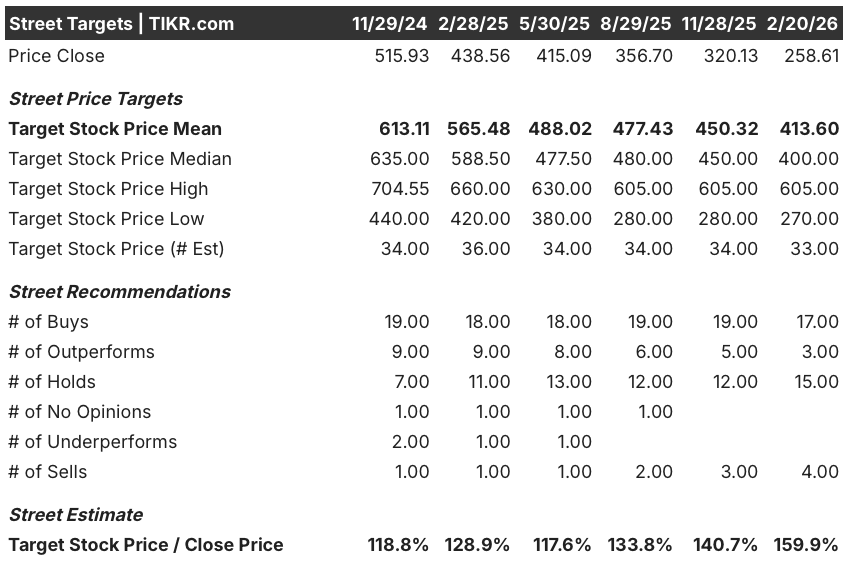

Wall Street still leans bullish but conviction is visibly eroding, with 17 buys and 3 outperforms against 15 holds and 4 sells as of February 20, 2026, while the mean price target of $413.60 implies a striking 59.9% upside from the current close of $258.61.

The target spread tells the real story of how divided sentiment has become, ranging from a bear case of $270.00 sitting barely above the current price to a bull case of $605.00 that would require Adobe to fully reassert its creative software dominance over an increasingly aggressive Figma.

What Does the Valuation Model Say?

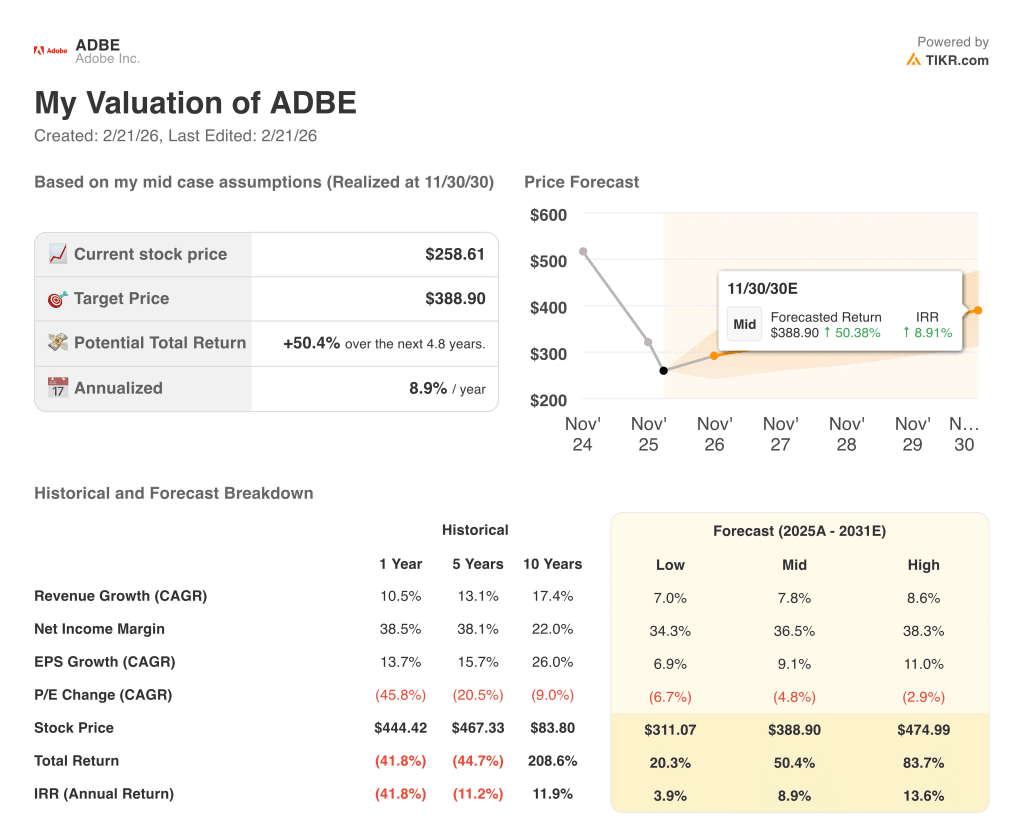

Even after pricing in Figma’s AI credit monetization threat and the sector-wide multiple compression that has cut valuations roughly in half, a mid-case valuation model targets Adobe at $388.90 by November 2030, implying a 50.4% total return and an 8.9% annualized IRR from current depressed levels.

The sharpest risk Adobe faces is not Figma alone but the combination of continued P/E compression, which the model already forecasts at a negative 4.8% CAGR through 2031, and institutional underweighting at a four-year extreme that could suppress any multiple recovery even if fundamentals hold.

At $258.61, Adobe looks materially undervalued relative to its earnings trajectory and analyst targets, but the stock remains a conviction buy only for investors willing to absorb further multiple compression pain before the AI disruption narrative either proves overblown or forces a genuine fundamental reset.

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.