Key Takeaways:

- AI-Powered Growth: BlackLine’s platform strategy and AI agents are driving record bookings growth of 22% in 2025.

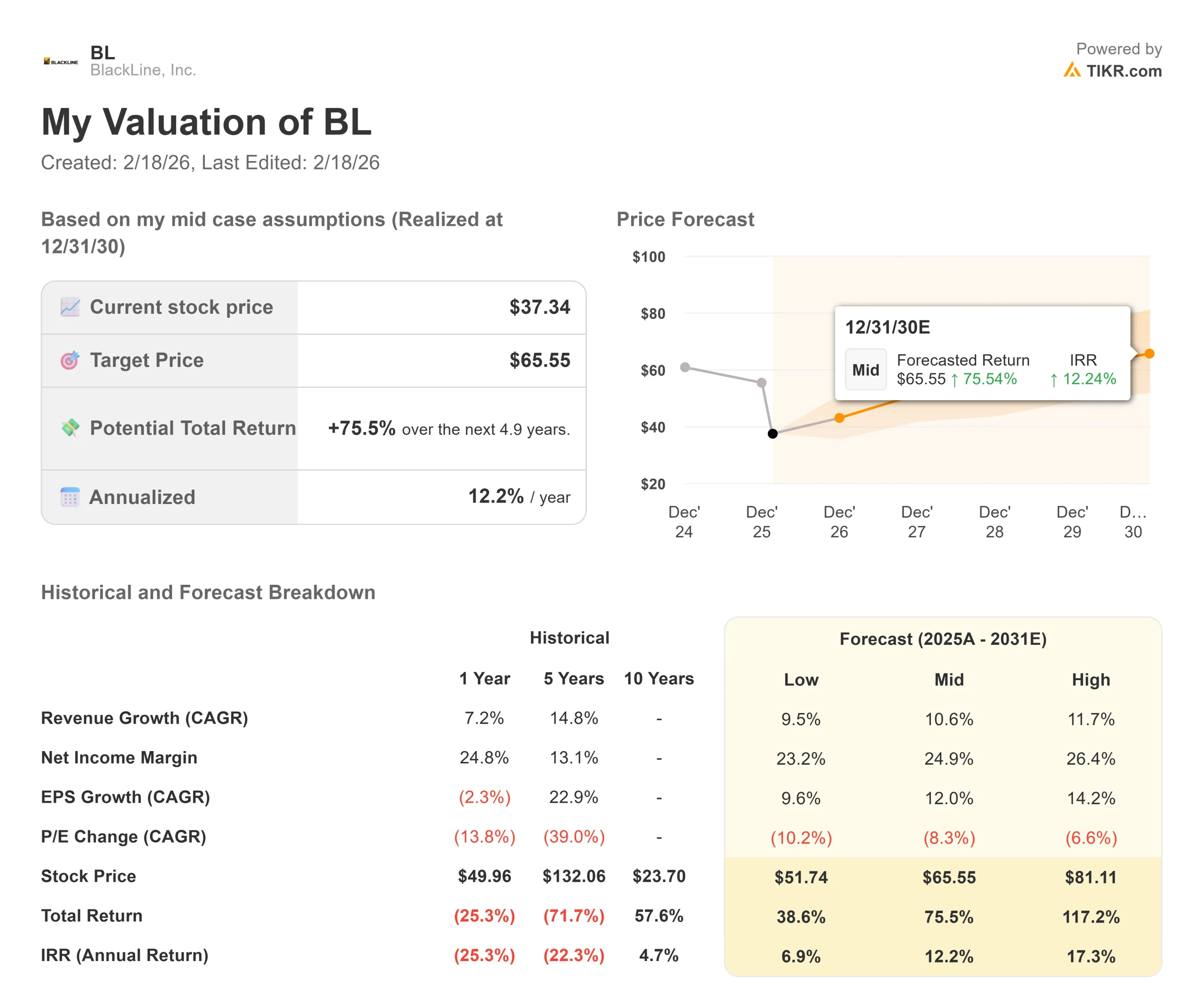

- Price Projection: Based on current execution, BL stock could reach $52 by December 2028.

- Potential Gains: This target implies a total return of 39% from the current price of $37.

- Annual Return: Investors could see roughly 12% growth over the next 2.9 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

BlackLine Corporation (BL) delivered strong fourth-quarter 2025 results, with 8% revenue growth, and raised guidance for 2026, signaling that the company’s transformation is gaining momentum.

CEO Owen Ryan highlighted that the company’s strategic shift is now translating into results.

- BlackLine now serves approximately 70% of the Fortune 100, up from 50% in 2022, demonstrating growing influence with the world’s most complex organizations.

- The company posted its strongest booking quarter ever, with full-year bookings growth of 22%.

- Nearly three-quarters of bookings came from existing customers, showing the platform’s value is resonating with the installed base.

- Remaining Performance Obligations (RPO) grew 23%, driven by platform adoption and multiyear renewals.

- Customers are making long-term commitments to BlackLine, with enterprise customers maintaining a 95% revenue renewal rate and 107% net revenue retention.

- BlackLine’s shift to platform pricing is fundamentally changing customer relationships. By moving away from per-seat subscriptions toward value-based partnerships, the company is capturing more revenue upfront while positioning for future AI-driven growth.

- The company continues to demonstrate operational discipline. Revenue grew 34% over the past three years while headcount increased just 2%, adding only 40 net new roles.

- Sales productivity improved notably, with customer acquisition costs down 30% this quarter.

Despite strong fundamentals and expanding margins, BlackLine trades at $37, offering upside for investors who recognize the company’s position as the financial operating system for enterprise CFOs.

See analysts’ full growth forecasts and estimates for BL stock (It’s free) >>>

What the Model Says for BlackLine Stock

We analyzed BlackLine’s transformation from a financial close solution into an intelligent platform for the CFO, powered by AI agents and deep financial process expertise.

- The company benefits from multiple growth drivers. Its platform strategy is accelerating adoption, with nearly 75% of new bookings leveraging platform pricing in Q4. This model is focusing on business outcomes rather than user seats.

- BlackLine’s Verity AI agents provide additional upside. These pre-trained, auditable agents automate reconciliations, collections, and accruals while maintaining the trust and controls that companies require. Management expects AI to drive both immediate platform adoption and future consumption-based revenue.

- The company’s partnership with SAP continues to mature. Every deal over $500,000 involved a partner, and BlackLine secured full product qualification for its Studio360 platform with SAP’s advanced financial close solution.

- Deeper integrations with SAP’s Joule Copilot are in development.

- Using a forecast of 11% annual revenue growth and 26.4% operating margins, our model projects the stock will rise to $52 within 2.9 years. This assumes a 15.4x price-to-earnings multiple.

- That represents compression from BlackLine’s historical P/E averages of 23.8x (one year) and 138x (five years). The lower multiple reflects the company’s transition period as it shifts customers to platform pricing and launches monetization of AI agents.

The real value lies in capturing the long-term opportunity to become the intelligent financial operating system for global enterprises while expanding margins toward best-in-class SaaS levels.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BL stock:

1. Revenue Growth: 11%

BlackLine’s growth centers on platform adoption and AI-driven expansion.

The company delivered 8% revenue growth in Q4 2025, with guidance calling for 9.1% to 9.6% growth in 2026.

Management expects acceleration as platform pricing gains traction.

Platform pricing ARR reached 11% of eligible ARR in Q4, up from 4% in Q3. The company targets 25% to 35% platform adoption by year-end 2026.

Strategic products like Intercompany and Invoice-to-Cash each delivered record years, representing 33% of sales.

New customer deal sizes increased 35%, driven by enterprise wins that view BlackLine as a strategic partner.

2. Operating margins: 26.4%

BlackLine delivered 25% non-GAAP operating margin in Q4 2025, demonstrating the scalability of its business model.

The company has grown its revenue 34% over three years while adding just 40 net employees.

With the Google Cloud migration now complete, BlackLine expects further margin expansion as legacy data centers shut down.

Management targets operating margins of 23.7% to 24.3% for 2026, with continued expansion in subsequent years.

3. Exit P/E Multiple: 15.4x

The market currently values BlackLine at 15.6x earnings. We assume modest compression to 15.4x over our forecast period, reflecting the company’s transition dynamics.

As BlackLine demonstrates consistent execution on platform adoption, AI monetization, and margin expansion, the company should command a premium multiple relative to the broader SaaS market given its mission-critical position in enterprise finance operations.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Software companies face technology transitions and execution risks. Here’s how BlackLine stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth slows to 9.5% and net income margins compress to 23.2%, investors still see a 39% total return (6.9% annually).

- Mid Case: With 10.6% growth and 24.9% margins, we expect a total return of 75% (12.2% annually).

- High Case: If AI adoption accelerates, driving 11.7% revenue growth while BlackLine maintains 26.4% margins, returns could hit 117% total (17.3% annually).

See what analysts think about BL stock right now (Free with TIKR) >>>

The range reflects execution on platform migrations, AI agent monetization, customer retention improvement, and SAP partnership development.

In the low case, platform adoption disappoints or competitive pressure limits pricing power.

In the high case, AI agents drive faster-than-expected consumption growth while enterprise customers expand aggressively.

How Much Upside Does BlackLine Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!