Key Stats for Accenture Stock

- Past-Week Performance: +3%

- 52-Week Range: $188.7 to $334.4

- Current Price: $209.4

What Happened?

Accenture (ACN), the world’s largest IT consulting firm, just made its most aggressive AI infrastructure bet yet, agreeing March 3 to acquire Ziff Davis’ entire Connectivity division for $1.2 billion in cash, adding Ookla’s Speedtest network intelligence platform and the Downdetector outage tracker to its AI services arsenal.

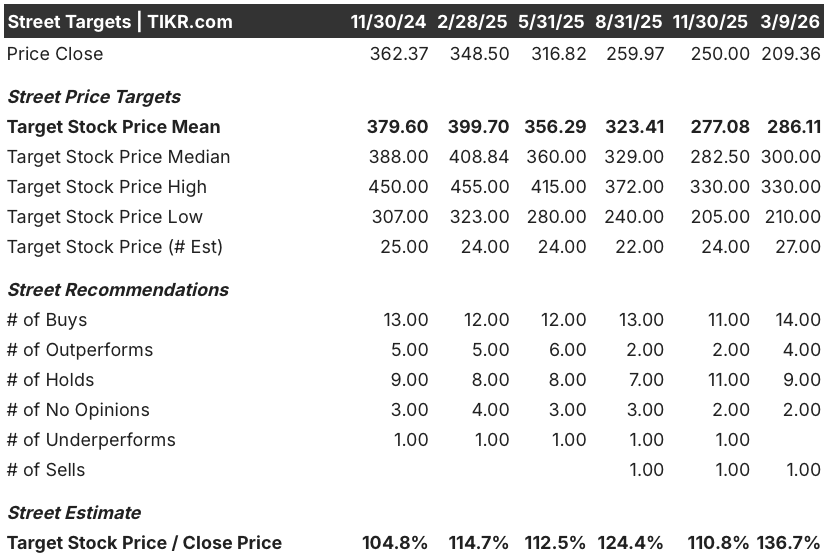

Wells Fargo upgraded ACN to “overweight” on February 17, citing two consecutive quarters of improving bookings growth and calling the stock’s 42.4% twelve-month decline an overreaction to AI disruption fears, with the median analyst price target sitting at $300 against a current price of $209.36.

Accenture’s Q1 FY2026 results, reported December 18, delivered $18.7 billion in revenue at the top of its guided range, with advanced AI bookings reaching $2.2 billion in a single quarter, nearly doubling year-over-year and pushing the cumulative total to $11.5 billion across 11,000 client projects.

Chief Executive Julie Sweet stated on the Q1 FY2026 earnings call that “enterprise AI is fundamentally different than consumer AI,” tying the remark directly to the firm’s strategy of winning large, multi-year transformation programs by solving clients’ foundational data and process debt before AI can scale.

With $3 billion committed to acquisitions this fiscal year, a free cash flow target of up to $10.5 billion, and at least $9.3 billion pledged for shareholder returns, Accenture is simultaneously compressing its valuation gap and building the network intelligence, agentic AI, and data infrastructure capabilities it needs to lead enterprise AI adoption through 2029 and beyond.

Wall Street’s Take on ACN Stock

WALL STREET’S TAKE — Accenture plc (ACN)

The March 3 Ookla acquisition, which adds real-time network intelligence data directly into Accenture’s AI services stack, strengthens the firm’s ability to win the large-scale enterprise transformation contracts that drive its managed services bookings, which grew 8% in Q1 FY2026.

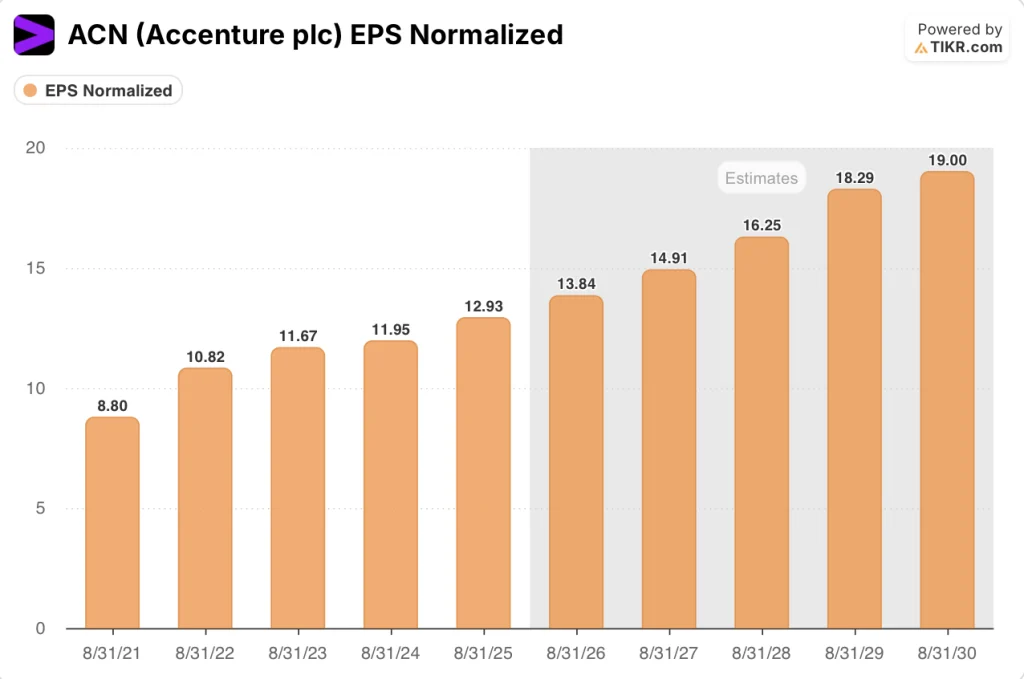

Accenture’s EPS has compounded from $8.80 in FY2021 to $12.93 in FY2025, and consensus estimates project $13.84 in FY2026, reaching $19 by FY2030, a trajectory that has not bent despite the stock’s 42.4% twelve-month decline.

27 analysts with active recommendations lean constructive, with 14 buys, 4 outperforms, and 9 holds, and their mean price target of $286.11 implies 36.7% upside from the current price of $209.36.

The spread between the analyst low target of $210 and the high of $330 reflects a binary read on federal headwinds, where the low assumes sustained government spending drag and the high prices in the second-half revenue acceleration Wells Fargo flagged on February 17.

What Does the Valuation Model Say?

TIKR’s mid-case model prices ACN at $330.13 by August 2030, implying a 57.7% total return and a 10.7% annualized IRR from today’s entry price of $209.36.

The model assumes 5.7% revenue CAGR and net income margins expanding from 11.7% today to 12.0%, driven by the fixed-price contract mix, which has already risen 10 points to 60% over three years.

The market is pricing ACN as an AI-disruption casualty, yet normalized EPS has grown every single year since FY2021 and consensus projects $13.84 for the fiscal year ending August 2026.

The $11.5 billion in cumulative advanced AI bookings across 11,000 projects, with over 1,300 clients now engaged, provides the contracted revenue backlog that underpins the model’s 6% FY2026 revenue growth estimate.

Management’s pledge to return at least $9.3 billion to shareholders this fiscal year, up 12% from FY2025, signals confidence in the free cash flow target of up to $10.5 billion, directly confirming the model’s margin expansion assumption.

Sustained federal spending cuts beyond the current estimated 1% revenue drag would pressure the Americas segment, which already saw public service decline in Q1, and compress the low end of the $13.52 to $13.90 FY2026 EPS guidance range.

The Q2 FY2026 earnings call on March 19 is the immediate test, where bookings momentum and any revision to the federal headwind estimate will either validate or challenge the second-half revenue acceleration thesis Wells Fargo built its February 17 upgrade around.

Should You Invest in Accenture plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ACN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Accenture plc alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ACN stock on TIKR for Free →