Key Stats for Abbott Laboratories Stock

- 52-Week Range: $91 to $139

- Current Price: $94

- Street Mean Target: $119

- Street High Target: $143

- Analyst Consensus:16 Buys, 5 Outperforms, 7 Holds

- TIKR Model Target (Dec. 2030): $154

What Happened?

Abbott Laboratories (ABT) is a diversified healthcare company spanning medical devices, diagnostics, nutrition, and established pharmaceuticals, now transformed by its $23 billion acquisition of cancer test maker Exact Sciences.

The Exact Sciences deal closed March 23, adding Cologuard, the leading at-home colorectal cancer screening test, and Oncotype DX to Abbott’s diagnostics portfolio.

Abbott stock fell roughly 5% following its April 16 Q1 2026 earnings report, which delivered an adjusted EPS of $1.15, narrowly beating the $1.14 consensus, on revenue of $11.16 billion against expectations of $11.0 billion.

The beat was not enough to offset the bigger story: Abbott trimmed its full-year 2026 adjusted EPS guidance to $5.38 to $5.58 from $5.55 to $5.80, absorbing a $0.20 per-share dilution hit tied to the Exact Sciences financing.

CEO Robert Ford framed the guidance cut as a deliberate derisking choice, not a deterioration signal, telling analysts on the Q1 2026 earnings call: “I’m not going to forecast that we’re going to make it up in Q4 this respiratory aspect.”

The quarter exposed real near-term noise: nutrition sales declined 6%, continuous glucose monitor (CGM) revenue grew just 7.5% after a tender delay slowed international volumes, and structural heart faced competitive pressure from Edwards Lifesciences.

The noise obscures a more compelling underlying story.

Medical devices, Abbott’s largest segment by revenue, grew 8.5%, with electrophysiology up 13%, heart failure up 12%, and rhythm management up 13% for the third consecutive quarter of double-digit growth.

In electrophysiology specifically, Abbott launched two pulsed field ablation (PFA) catheters in Q1: the Volt PFA in the U.S., driving 14% domestic EP growth, and the TactiFlex Duo in Europe, fueling mid-teens European growth.

Ford made a pointed growth forecast on CGM, projecting a return to double-digit growth in Q2, supported by evidence from a randomized controlled trial showing Type 2 basal insulin patients achieved better outcomes using Libre.

Cancer diagnostics, now including Exact Sciences, grew 13% on a comparable basis in Q1, with Cologuard posting mid-teens growth and international cancer diagnostics up in the high teens.

Ford described the Cologuard market opportunity as structurally underpenetrated: 50 million Americans are not current with colorectal cancer screening, colonoscopy capacity is fixed at roughly 6 million procedures per year, and average wait times for colonoscopies now range from 3 to 9 months depending on state.

The FDA and CE Mark clearances for Ultreon 3.0, Abbott’s AI-guided coronary imaging software, confirmed April 28, position the company to expand its next-generation intravascular imaging platform simultaneously in the U.S. and Europe.

Abbott Laboratories stock has declined 22.5% year to date, making it one of the worst performers in large-cap medtech despite a business that is growing at an accelerating pace in its highest-value segments.

Wall Street’s Take on ABT Stock

The Exact Sciences acquisition layers $3 billion in incremental 2026 revenue onto a medical device franchise already growing in the low double digits, shifting Abbott’s long-term growth ceiling meaningfully higher even as the near-term EPS guide absorbs dilution mechanics.

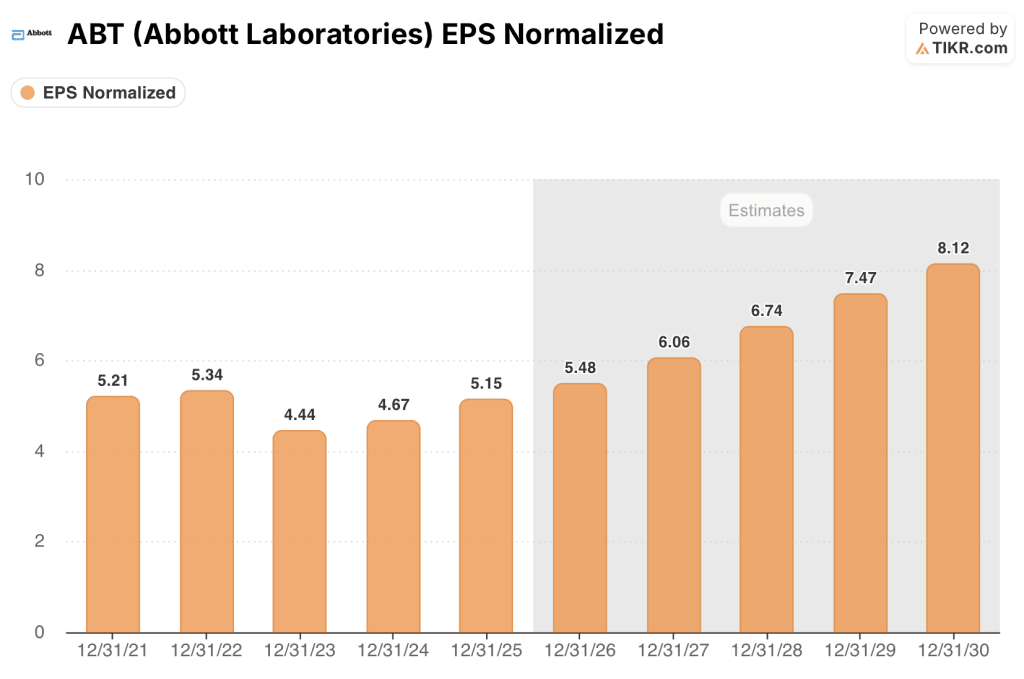

Abbott’s normalized EPS of $5.15 in 2025 is expected to grow to around $5 in 2026 before reaccelerating to around $6 in 2027 and around $7 in 2028, as the Exact Sciences dilution fades and the combined portfolio compounds.

The buy-side conviction on Abbott Laboratories stock has held even as the price targets have not: 21 of 25 analysts rate it a buy or outperform, but the mean target has compressed from $144 at the end of 2025 to around $119 today, a $25 cut that reflects dilution modeling rather than a change in the underlying growth outlook.

The $92 low target and $143 high target bracket a genuine debate: the low end prices in sustained nutrition weakness and competitive CGM pressure, while the high end credits Cologuard and the EP catheter launches with the durable mid-teens growth rate already demonstrated in Q1.

With the mean target now sitting at around $119 against a stock that has fallen to $94, the implied 26% upside is actually wider than it was when Abbott Laboratories stock was trading at $125 in December, and yet the analyst conviction profile has strengthened, leaving Abbott Laboratories stock appearing undervalued as the business enters a period of compounding revenue from two simultaneously accelerating growth engines.

The most precise signal came from CEO Robert Ford on the Q1 earnings call, who confirmed that Cologuard rescreens now account for 25% of all tests and compound at an increasing rate with each passing year, embedding durable recurring revenue that the declining price targets have not captured.

The core risk is execution: a second consecutive quarter of CGM growth below double digits, further nutrition volume softness, or a structural heart miss would confirm the bear case that operational complexity is weighing on the underlying business.

The catalyst is Q2 guidance delivery: if CGM returns to double-digit growth and Cologuard maintains mid-teens momentum, the combination will demonstrate that both the organic and acquired growth engines are running simultaneously, which is the entire investment thesis.

What Does the Valuation Model Say?

The TIKR model prices Abbott Laboratories at a mid-case target of around $154, implying 63% total return over roughly 4.7 years, built on a mid-case revenue CAGR of around 8% through 2030 and net income margins expanding from 20.4% in 2025 toward around 21%, both assumptions already well-supported by Q1’s 13% cancer diagnostics growth and the EP franchise’s third consecutive double-digit quarter.

At 17x forward earnings against a revenue profile that is now growing faster than at any point since the COVID testing windfall, Abbott Laboratories stock appears undervalued for investors willing to look past a guidance cut that reflects dilution mechanics rather than business deterioration.

The main tension for Abbott Laboratories stock is whether the Exact Sciences integration accelerates the growth rate the company is already posting, or introduces the kind of operational drag that distracted management at the time of other large Abbott acquisitions.

Bull Case

- Cologuard grew mid-teens in Q1 and has 50 million unscreened Americans as addressable pipeline, with rescreens now compounding at 500,000 patients annually

- Volt PFA and TactiFlex Duo are in limited market release with physician feedback Ford described as “extremely favorable,” setting up EP acceleration through the back half of 2026

- CGM management guided explicitly to double-digit Q2 growth, and Type 2 non-insulin reimbursement expansion could add close to 10 million newly covered patients as proposed language arrives

- The TIKR model’s high-case target of around $257 (IRR around 12%) requires only around 9% revenue CAGR, a rate Exact Sciences alone was already running near before the acquisition closed

Bear Case

- Nutrition sales declined 6% in Q1 and a volume recovery depends on pricing pass-through that is still incomplete at the retail channel level

- Structural heart showed execution gaps in the U.S. market and management acknowledged competitive share losses that required leadership changes mid-quarter

- EPS dilution from Exact Sciences ($0.20 per share) runs through 2026 and 2027 before turning accretive, compressing near-term earnings growth to around 6% in 2026 versus the revenue story

- A weak respiratory testing season further cut into diagnostic revenue in Q1, and Ford explicitly declined to assume a recovery in Q4, leaving that upside unmodeled

Should You Invest in Abbott Laboratories?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ABT stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Abbott Laboratories alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ABT stock on TIKR for Free →