Key Stats for Vulcan Materials Stock

- Past-Week Performance: %

- 52-Week Range: $215.1 to $331.1

- Current Price: $310

What Happened?

Vulcan Materials stock (VMC) dropped 7.2% on February 17 after missing Q4 EPS by $0.41, yet the stock now trades at $310, just 6.4% below its 52-week high.

Specifically, 17 of 25 brokerages maintained buy ratings after the miss, with a median price target of $330.50, signaling Wall Street is holding conviction through the weakness.

Regardless, the engine remains intact: full-year adjusted EBITDA grew 13% to $2.3 billion, and operating cash flow surged 29% to $1.8 billion in 2025.

Consequently, the market is beginning to re-rate Vulcan from a cyclical aggregates producer to a data center infrastructure play, with 70% of data center construction activity occurring within 30 miles of a Vulcan facility.

Meanwhile, CEO Ronnie Pruitt stated on the Q4 earnings call that “data centers remain the biggest catalyst with over 150 million square feet under construction,” as large projects now represent 45% of bookings versus a historical average of 30%.

Additionally, Wall Street’s median price target of $330.50 sits 6.6% above current levels, with 17 buy-rated brokerages holding firm despite the Q4 earnings miss.

Looking further out, Vulcan’s 55% improvement in aggregates cash gross profit per ton over 4.5 years positions it to compound margins further as data center and infrastructure demand accelerates through 2028.

Wall Street’s Take on Vulcan Materials Stock

Vulcan’s Q4 EPS miss of $0.41 was weather and mix-driven, not structural, leaving the 2026 EBITDA recovery story fully intact.

Underneath the noise, EBITDA grows 8.5% to $2.5 billion in 2026, while EPS accelerates 17% to $9.36 from $8.00 in 2025.

Still,Wall Street fields 14 buys, 3 outperforms, 5 holds, and 1 sell, with a mean target of $328.4, implying 5.9% upside from $310.

The analyst range stretches from $198.0 to $375.0, with single-family housing recovery determining the low end and data center demand acceleration driving the high.

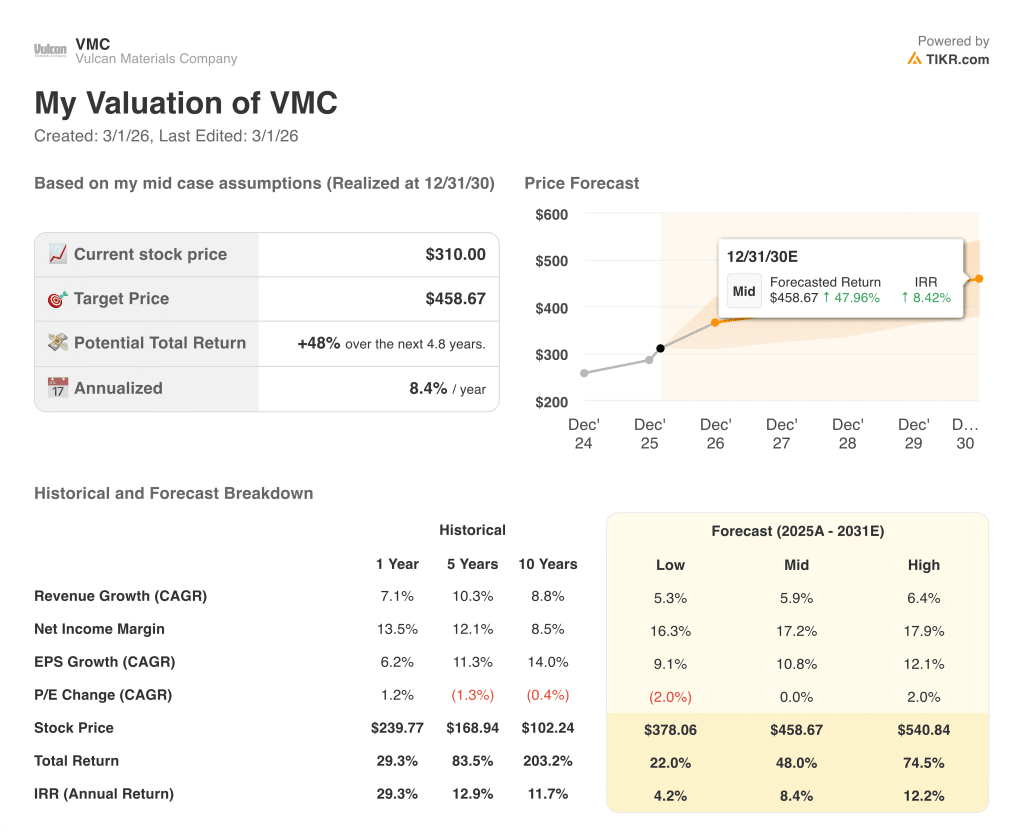

What Does the Valuation Model Say?

The TIKR mid-case model targets $458.7 by December 31, 2030, a 48% total return from today’s price. That delivers an 8.4% annualized IRR over 4.8 years.

The market is punishing Vulcan for a one-quarter miss caused by weather and product mix, not business deterioration.

The number that exposes that mispricing: EBITDA margins expand to 31.3% in 2026, up from 29.3% in 2025, continuing a 700 bps three-year expansion streak.

CEO Ronnie Pruitt confirmed on the Q4 call that 70% of all data center construction activity sits within 30 miles of a Vulcan facility, making the demand pipeline structural, not cyclical.

However, if single-family housing stays flat and midyear price increases fail, the $2.4 billion low-end EBITDA guide stalls the re-rating entirely.

Watch the March 12 Investor Day: management’s long-term EBITDA targets will confirm whether the $458.7 model price is conservative or stretched.

Therefore, VMC stock appears to be undervalued, with a 48% model upside and a data center footprint the current price completely ignores.

Should You Invest in Vulcan Materials Company Stock?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VMC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vulcan Materials Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VMC stock on TIKR for Free →