Veeva Systems (NYSE: VEEV) has been gaining momentum over the past year as life sciences companies continue modernizing their clinical, regulatory, and commercial systems. The stock trades near $293/share today, supported by consistent double-digit earnings growth, high margins, and one of the stickiest customer bases in enterprise software.

Recently, Veeva announced new progress in its long-term plan to fully transition off Salesforce by 2030, with more customers adopting Veeva Vault as their primary commercial and data management platform. The company is also seeing increased adoption of its development cloud products, signaling that pharmaceutical companies are expanding digital investments across clinical and regulatory operations. These updates show Veeva is continuing to execute well even in a softer enterprise spending environment.

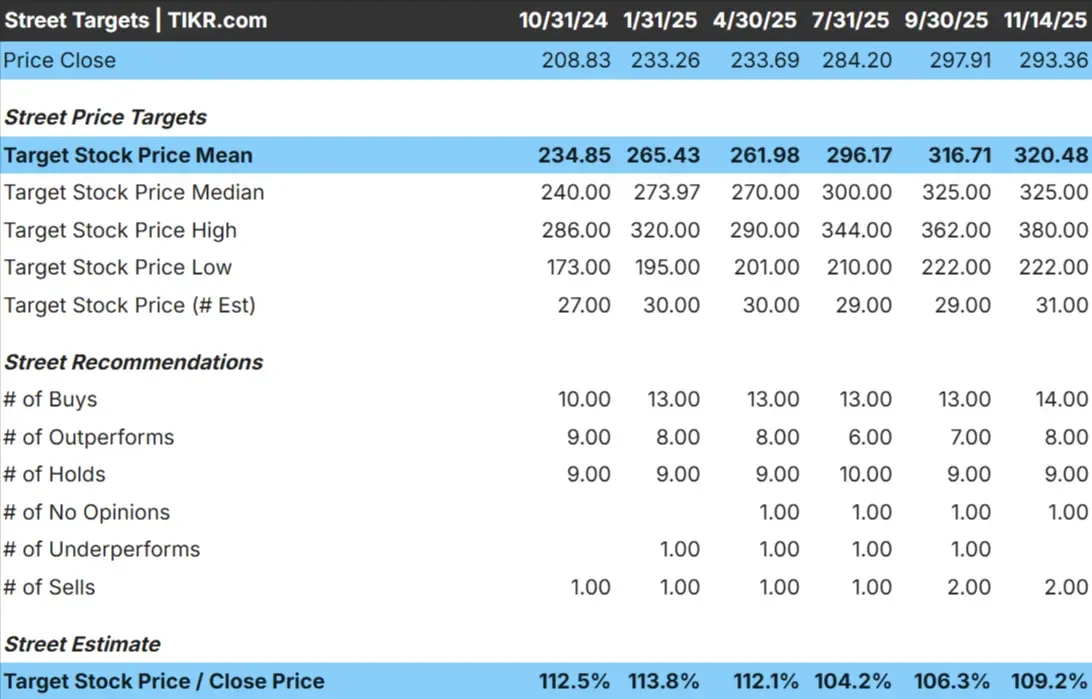

This article explores where Wall Street analysts believe Veeva could trade by 2028. We pulled together consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

Veeva trades around $293/share today. The average analyst price target is about $320/share, which suggests roughly 9% upside. This places the stock in the modest upside category.

- High estimate: ~$380/share

- Low estimate: ~$222/share

- Median target: ~$325/share

- Ratings: 14 Buys, 8 Outperforms, 9 Holds, 2 Sells

For investors, this reflects a business analysts respect but approach with measured expectations. Sentiment is positive but cautious. Veeva could outperform if adoption of Vault and the development cloud accelerates, but analysts want to see more evidence of sustained demand before assigning stronger conviction.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Veeva: Growth Outlook and Valuation

The company’s fundamentals appear strong, supported by stable growth and high profitability:

- Revenue growth projected at 13.3%

- Operating margins expected to remain near 44.9%

- Shares trade at about 34.5x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 34.5x forward P E suggests around $380/share by 2028

- That implies roughly 30% upside, or about 12% annualized returns

These numbers point to a steady compounder rather than a high-growth story. Veeva’s valuation is elevated, but its recurring revenue base, mission-critical role in regulated industries, and long-term shift to its own tech stack help justify the premium.

For investors, Veeva offers one of the more reliable long-term profiles in enterprise software. The company does not need rapid acceleration to deliver meaningful returns, as its margin structure and customer stickiness already support consistent compounding.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Veeva remains one of the most trusted platforms in global life sciences. Its software supports essential processes like clinical trial oversight, regulatory submissions, quality management, and commercial operations. These workflows are highly regulated, and once a company standardizes on Veeva, switching costs become significant.

Digital transformation tailwinds also appear strong. More pharmaceutical companies are adopting Veeva Vault and expanding usage across development and regulatory teams. This helps deepen customer relationships and reinforces the company’s competitive moat.

For investors, these factors support steady revenue visibility and help Veeva maintain its strong margin profile even during softer enterprise spending periods.

Bear Case: Valuation and Growth Moderation

Despite its strengths, Veeva trades at a premium valuation near 35x forward earnings. That leaves limited room for disappointment if customer spending slows or new product adoption takes longer than expected. Some biopharma companies are tightening budgets, which could result in slower short-term growth.

Competition is also worth monitoring. While Veeva is the clear leader, newer tools in data, analytics, and trial workflow management are emerging. Even modest competitive pressure can influence long-term profitability expectations.

For investors, the main risk is valuation compression rather than a weakening business. High-quality companies can still produce muted returns if their multiples decline faster than earnings grow.

Outlook for 2028: What Could Veeva Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Veeva could trade near $380/share by 2028. That represents about 30% upside from today, or roughly 12% annualized returns.

This outlook assumes Veeva maintains its steady revenue growth, preserves high margins, and continues expanding adoption of Vault and development cloud products. If these trends hold, Veeva appears well positioned to deliver the consistent compounding investors expect from high-quality software businesses.

For investors, Veeva stands out as a durable long-term compounder. The stock may not deliver dramatic gains in the near term, but its combination of predictable earnings, industry tailwinds, and deep customer integration creates a clear path to reliable returns through 2028.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>