Synopsys Inc. (NASDAQ: SNPS) has dropped to about $390/share after a 27% decline over the past year. The pullback reflects broad weakness in software and semiconductors, but the company’s position as a critical supplier of chip design and AI automation tools remains intact. Slower spending across tech has pressured valuations, though Synopsys’ long-term relevance to the semiconductor ecosystem continues to stand out.

Recently, Synopsys reported results that highlighted strong demand for its design software and semiconductor IP, even as broader chip markets remain uneven. The company also advanced its AI-driven EDA initiatives, reinforcing its role in enabling faster, more efficient chip development at a time when AI workloads are pushing complexity to new levels. These developments suggest Synopsys is still executing well despite macro uncertainty.

This article explores where Wall Street analysts think Synopsys could trade by 2027. We have pulled together consensus targets and valuation model data from the images you provided to outline the stock’s potential path. These figures reflect current analyst expectations and not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

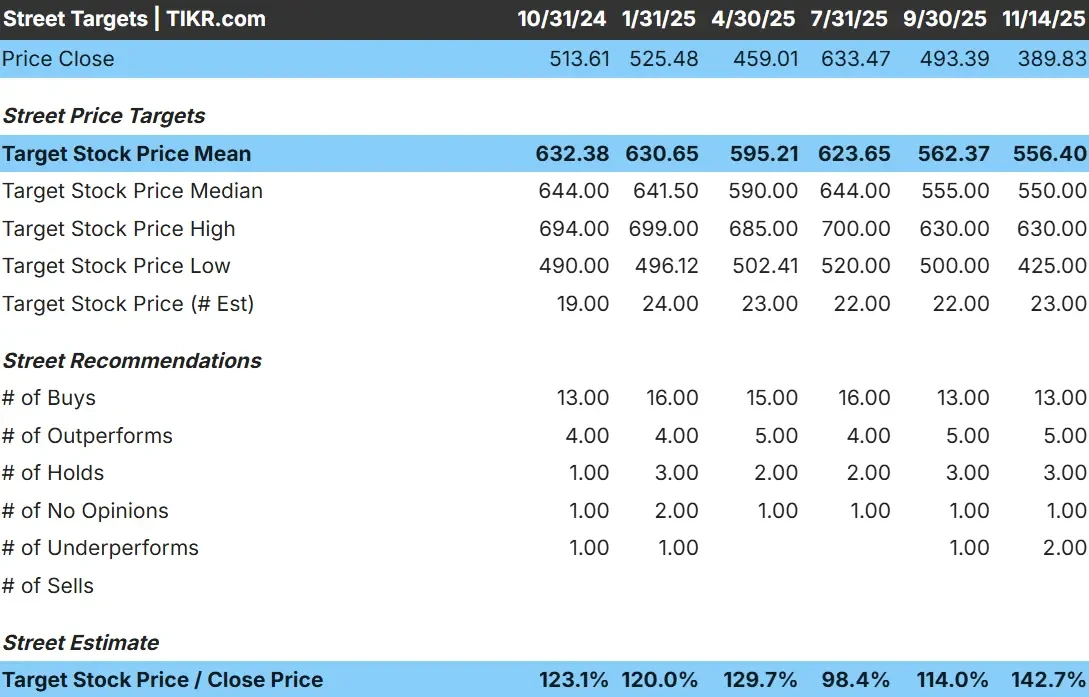

Synopsys trades near $390/share today. The latest analyst price targets point to an average estimate of about $556/share, which suggests meaningful upside of roughly 43%. Forecasts show a wide range, highlighting mixed conviction among analysts:

- High estimate: ~$630/share

- Low estimate: ~$425/share

- Median target: ~$550/share

- Ratings: 13 Buys, 5 Outperforms, 3 Holds, 2 Underperforms

Even after the recent pullback, analysts still expect the stock to recover as semiconductor complexity continues rising and AI workloads expand. For investors, the takeaway is that there is meaningful upside potential, but sentiment remains sensitive to macro trends in chip spending. Execution and industry conditions will play major roles in whether the stock can realize this upside.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Synopsys: Growth Outlook and Valuation

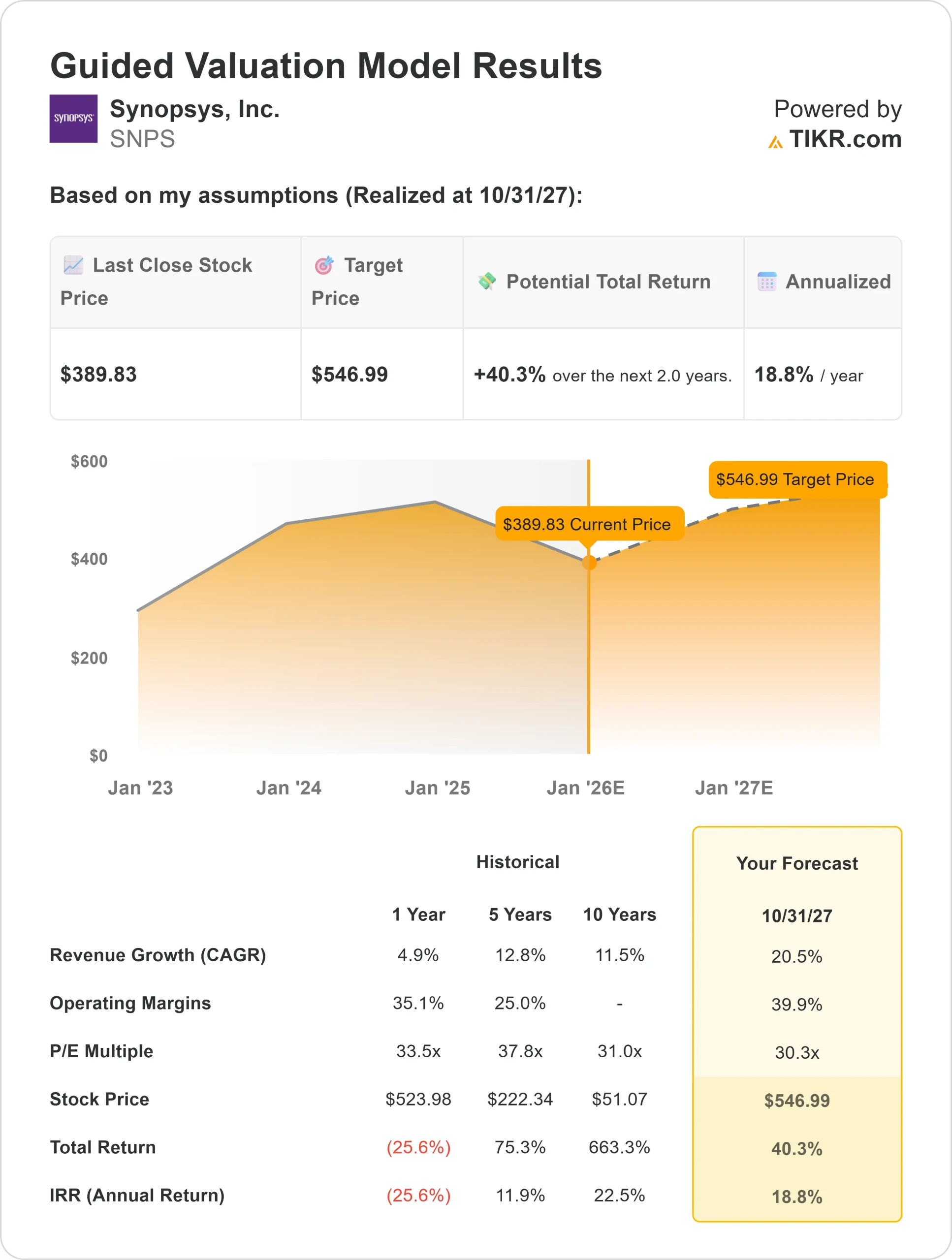

The company’s fundamentals look strong based on the Guided Valuation Model inputs:

- Revenue growth: 20.5%

- Operating margins: 39.9%

- Forward valuation: 30.3x earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 30.3x forward P E suggests ~$547/share by 2027

- That implies roughly 40% upside, or about 19% annualized returns

These results point to a high quality compounder with durable growth drivers. Synopsys benefits from long-term structural demand in chip design, verification, and AI automation. Its recurring revenue base and deep customer integration give it a level of stability uncommon in the semiconductor ecosystem.

For investors, the model reinforces that Synopsys is positioned for steady compounding rather than short-term swings. If the company maintains strong margins and continues expanding its AI-enabled design suite, the stock has a clear path to delivering meaningful returns through 2027.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Synopsys remains one of the most essential suppliers in the semiconductor ecosystem. Its software powers the design of increasingly complex chips, and demand continues to rise as AI workloads push performance and efficiency requirements higher. These trends make Synopsys a critical enabler of next-generation semiconductor development.

The business also benefits from a highly resilient model. Recurring revenue is strong, customer relationships are long term, and design cycles typically span several years. For investors, these strengths offer steady visibility in an industry known for volatility, positioning Synopsys to grow even when hardware markets soften.

Bear Case: Valuation and Market Sensitivity

Despite its advantages, Synopsys is not immune to risk. The stock still trades at a premium valuation, and that premium requires consistent delivery. If semiconductor development budgets tighten or if customers delay large design programs, growth expectations could come under pressure.

Competition is also increasing as rivals build their own AI-enabled design tools. Pricing pressure or slower adoption of advanced software could weigh on results. For investors, the concern is that even strong companies can see multiples contract if the broader tech environment weakens or if execution slips.

Outlook for 2027: What Could Synopsys Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Synopsys could trade near $547/share by 2027. That represents roughly 40% upside from current levels, or about 19% annualized returns. The model reflects expectations for continued margin strength, resilient demand for design automation, and growing adoption of AI-driven tools.

While the forecast is encouraging, it already assumes steady execution. For Synopsys to outperform these expectations, it would likely need faster growth in its AI-enabled software offerings, stronger semiconductor IP adoption, or a more robust rebound in enterprise tech spending. Without that, investors should expect returns roughly in line with the current valuation model.

For investors, Synopsys stands out as a high quality compounder with credible long-term potential. Its central role in next-generation chip design positions the company well, but sustained leadership and disciplined execution will be key to delivering returns above the current outlook.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>