Key Takeaways:

- Fortinet is expanding its secure networking platform as enterprises converge networking and security to protect hybrid and cloud environments.

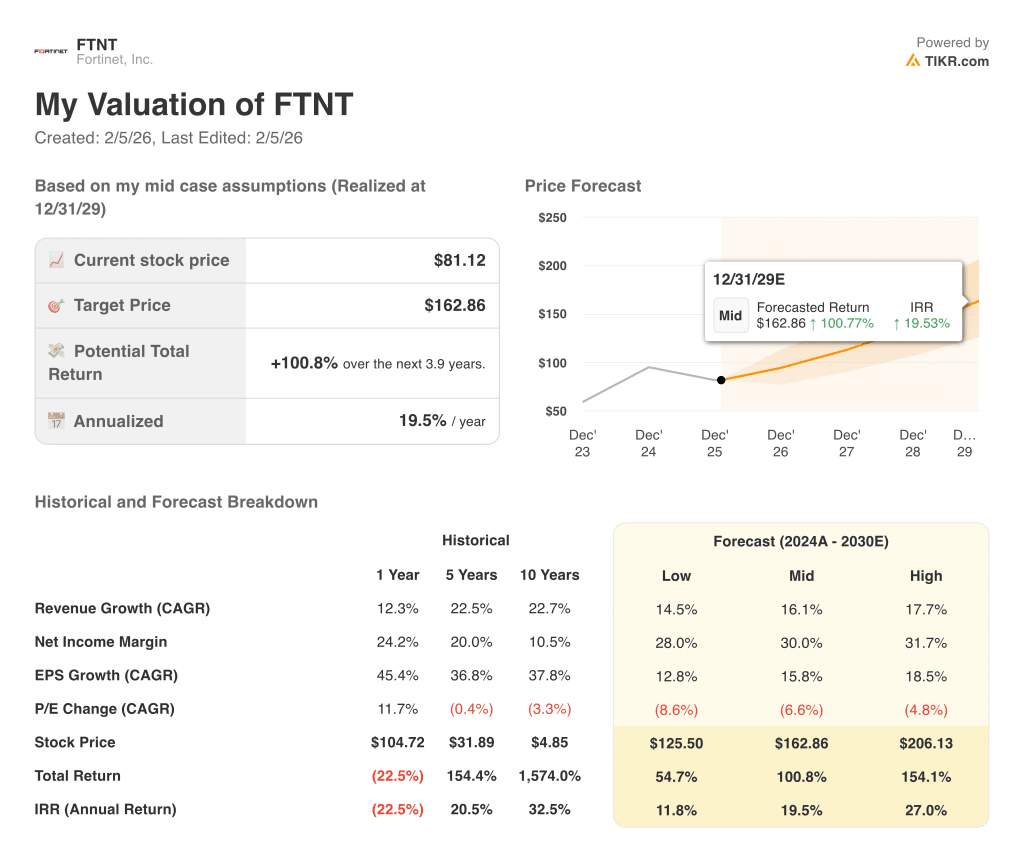

- FTNT stock could reasonably reach $163 per share by December 2029, based on our valuation assumptions.

- This implies a total return of 100.8% from today’s price of $81, with an annualized return of 19.5% over the next 3.9 years.

Fortinet (FTNT) is strengthening its position in cybersecurity as organizations integrate networking and security, and as demand rises for secure connectivity across data centers, branches, and cloud environments.

The security platform leader serves enterprises, service providers, governments, and small businesses through firewalls, secure SD‑WAN, SASE, and AI-driven security operations, and it continues to benefit as cyber threats grow and network architectures become more complex.

The company generated a total return of about 21% over the last year, while the shares now trade around $81, near the lower half of their 52‑week range between $70.12 and $114.82.

Fortinet maintains strong profitability, with a last‑twelve‑month gross margin of 80.9% and EBIT margin of 30.9%, and it earns high returns on invested capital above 100%, which supports sustained reinvestment in growth.

Fortinet demonstrates solid execution heading into its fourth‑quarter 2025 earnings release on February 5, 2026, and it has remained active at industry events such as the World Economic Forum 2026 and multiple technology and cybersecurity conferences during late 2025.

Here’s why Fortinet stock could provide attractive returns through 2029 as it benefits from secular cybersecurity demand and maintains high margins while growing revenue at a double‑digit pace.

What the Model Says for Fortinet Stock

We analyzed the upside potential for Fortinet stock using valuation assumptions based on its strong historical growth, structurally high margins, and premium but still reasonable valuation multiple relative to its profitability profile.

Based on estimates of 11.9% annual revenue growth, 34.5% operating margins, and a normalized P/E multiple of 28.5x, the guided model projects Fortinet stock could rise from $81 to $105 per share by December 2027.

That would be a total return of about 29.2% or roughly 14.4% annualized over the next 1.9 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Fortinet stock:

1. Revenue Growth: 11.9%

Fortinet has delivered robust growth, with revenue rising at a 21.2% compound annual rate over the last three years, and forward two‑year revenue expected to grow at around 12.3% annually according to consensus estimates.

Based on analysts’ consensus estimates, we used an 11.9% forecast in the guided valuation model, reflecting Fortinet’s ability to sustain double‑digit top‑line growth as secure networking, SASE, and AI‑driven security operations remain key priorities for customers.

This assumption is consistent with management’s outlook for 2025 revenue between 6.72 and 6.78 billion dollars, which implies continued expansion from both product and high‑margin service segments.

Because revenue growth has remained near the mid‑teens despite a choppy firewall cycle, an 11.9% CAGR through 2027 appears aligned with current expectations rather than aggressive.

2. Operating Margins: 34.5%

Fortinet currently generates attractive profitability, with non‑GAAP operating margins guided between 34.5% and 35.0% for 2025 and last‑twelve‑month EBIT margins of about 30.9%.

Based on analysts’ consensus estimates, we use 34.5% operating margins in the guided model, reflecting Fortinet’s ability to expand margins slightly as revenue grows while maintaining elevated gross margins around 80%.

These assumptions are supported by the company’s subscription‑heavy services mix, high‑margin software and security operations offerings, and disciplined cost management, which helped drive a record non‑GAAP operating margin of 37% in the third quarter of 2025.

Because cybersecurity solutions are mission‑critical and often sold on multi‑year contracts, Fortinet can sustain strong operating leverage even as it continues to invest in R&D and sales to pursue growth opportunities.

3. Exit P/E Multiple: 28.5x

Fortinet stock currently trades near 30x normalized earnings, and the guided valuation uses an exit P/E multiple of 28.5x by 2027, slightly below the current level.

Based on analysts’ consensus estimates, we maintain a 28.5x exit multiple given Fortinet’s durable competitive advantages in secure networking, SASE, and AI‑driven security operations, along with its strong balance sheet and high returns on capital.

This multiple is also broadly in line with external fair‑value analyses that place Fortinet’s justified P/E in the low‑to‑mid‑30s, while still allowing for modest compression as growth gradually moderates.

Because the model does not depend on multiple expansion, most of the projected returns come from earnings growth and margin strength rather than a higher valuation, which reduces reliance on changing investor sentiment.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for FTNT stock through 2030 show varied outcomes based on revenue growth, margin expansion, and valuation changes (these are estimates, not guaranteed returns):

- Low Case: Revenue growth slows, and competitive pressures in cybersecurity intensify → 11.8% annual returns

- Mid Case: Fortinet sustains double‑digit secure networking growth and maintains strong margins → 19.5% annual returns

- High Case: Faster platform adoption and international expansion drive stronger growth and profitability → 27.0% annual returns

Even in the conservative low‑case scenario, Fortinet stock still produces double‑digit annualized returns above 10%, supported by durable cybersecurity demand, strong margins, and a solid balance sheet with net cash and negative net debt to EBITDA.

Because the base and high cases both exceed 15% annualized returns, the valuation models suggest that Fortinet could be particularly interesting for long‑term investors who believe in sustained cybersecurity growth and Fortinet’s competitive position, while acknowledging that execution risks, macro conditions, and competitive dynamics could affect actual outcomes.

See what analysts think about FTNT stock right now (Free with TIKR) >>>

How Much Upside Does Fortinet Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!