Key Takeaways for United Airlines Stock

- United Airlines reported Q1 2026 total revenue of $14.6 billion, up 11% year-over-year to a record first quarter.

- Adjusted EPS came in at $1.19, up 31% year-over-year, despite absorbing a $340 million higher fuel bill.

- Operating margins compressed to 9% in fiscal 2025 from a 10% peak in fiscal 2023, as fuel costs outpaced gross profit growth.

- TIKR’s model values United Airlines at approximately $152 by December 2030, implying around 31% total return from the current price of $116.

United Airlines Stock Just Posted Record Q1 Revenue While Fuel Costs Rewrote the Margin Story

United Airlines Holdings (UAL) delivered record first-quarter revenue of $14.6 billion in Q1 2026, up 11% year-over-year, while a $340 million fuel cost surge from the Iran conflict simultaneously compressed the operating margins the company spent three years building.

Premium demand was the standout driver, with premium revenues rising 14% on only 4% capacity growth, pushing premium RASM (revenue per available seat mile) up 9% year-over-year.

Selling yields, which measure ticket prices for future travel, moved from up 4% year-over-year in January and February to up 18% in the second half of March, and then to up 20% in the final week of April.

CFO Mike Leskinen reported adjusted EPS of $1.19, up 31% year-over-year, within the initial guidance range of $1 to $1.50, even with the elevated fuel bill.

CEO Scott Kirby told analysts on the Q1 earnings call: “I feel very good about 100% recovery and getting to double-digit margins in 2027.”

United responded to the fuel environment by proactively cutting approximately 5 points of planned capacity for the back half of 2026, targeting Q3 and Q4 at flat to up 2% year-over-year.

The company also paid down more than $3.1 billion in debt and returned to the unsecured bond market for the first time since 2019, pricing a 3-year bond below 5%.

The case for United Airlines stock rests on whether the yield recovery management is engineering in real time translates into an operating margin rebound that the current share price at $116 does not price in.

United’s Gross Margin Is Holding Firm. The Operating Margin Is Not. That Gap Is the Story

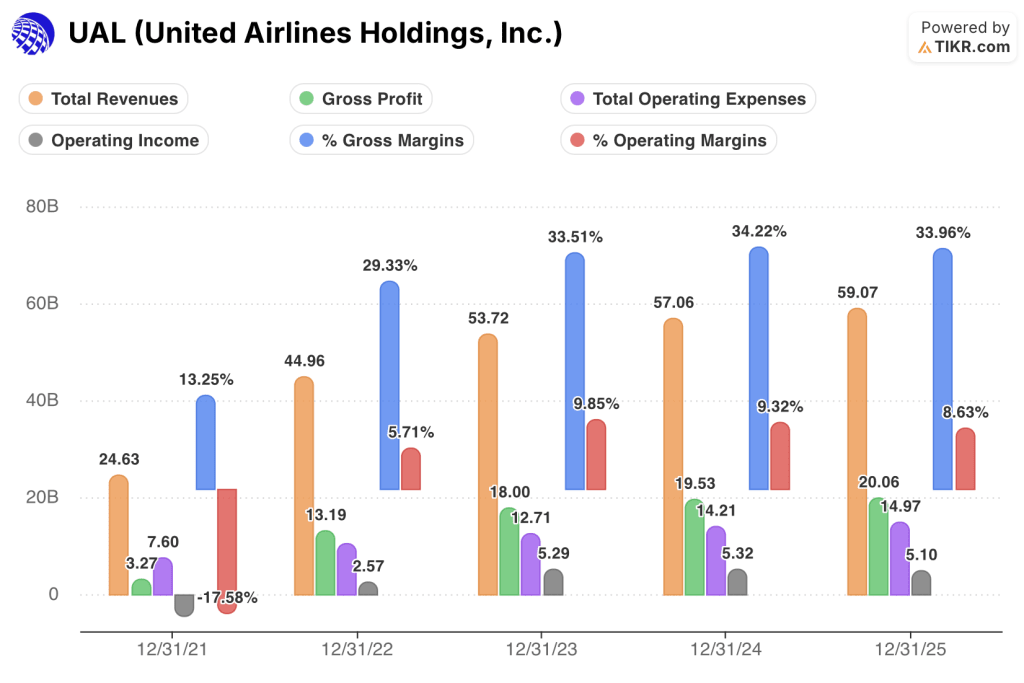

Total revenue for United grew 4% year-over-year in fiscal 2025 to $59.1 billion, a sharp deceleration from 20% growth in fiscal 2023.

Gross profit reached $20.1 billion in fiscal 2025, with gross margins holding near 34%, a level consistent with fiscal 2023 and 2024, signaling that the pricing structure of the core business remained intact.

Total operating expenses grew from $14.2 billion in fiscal 2024 to $15.0 billion in fiscal 2025, absorbing the fuel cost escalation that revenue growth could not offset.

Operating income declined from $5.3 billion in fiscal 2024 to $5.1 billion in fiscal 2025, a 4% contraction that marked the first year-over-year decline since the pandemic recovery period.

Operating margins compressed from 9% in fiscal 2024 to 9% in fiscal 2025 on a headline basis, but the LTM figure also sits at 9%, masking a trough that the Q1 2026 data began to surface.

The thesis is not that gross margins are breaking down. They are not. The thesis is that operating margins are being artificially suppressed by a fuel cost event that management is actively passing through to yields, and the income statement recovery has not yet registered at the operating line.

UAL Leads the Legacy Peer Group on Operating Margins, but the Gap With Delta Is the Competitive Benchmark That Matters

United Airlines posted an operating margin of 9% in fiscal 2025, holding above American Airlines (AAL) at 3% and Southwest Airlines (LUV) at 3% for the same period.

Delta Air Lines (DAL) led the peer group at 9%, matching United’s margin level while operating a comparably sized network, which sets the competitive ceiling United has not yet broken through.

The structural story is the distance from American’s 3% operating margin, which confirms that the fuel environment pressured all legacy carriers but hit under-capitalized balance sheets disproportionately, leaving United’s cost discipline in a materially stronger position.

Southwest’s 3% margin in fiscal 2025 reflects a business model under stress from structural changes that are distinct from the fuel shock, making it the least useful competitive benchmark for United’s thesis.

The margin convergence between United and Delta at the 9% level in fiscal 2025 is the figure that matters: if United’s yield recovery delivers the operating margin expansion management guided toward double digits in 2027, it would open a lead over Delta that the current UAL stock price at $116 does not yet reward.

Is United Airlines Stock Undervalued in 2026? TIKR’s $152 Model Says the Operating Margin Recovery Has to Hold

TIKR’s model values United Airlines at approximately $152 by December 2030, implying around 31% total return from the current price of $116, or roughly 6% per year.

That target becomes credible only if operating margins recover toward the double-digit level management has explicitly guided for 2027, a trajectory supported by the gross margin stability already visible in the income statement.

If the Q2 through Q4 yield pass-through delivers even the low end of the 40% to 100% fuel cost recovery range management outlined, the gap between gross margins at 34% and operating margins at 9% narrows in a way the LTM income statement does not yet show.

Should You Invest in United Airlines Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up United Airlines Holdings, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Airlines Holdings, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UAL stock on TIKR for Free →

What Did United Airlines Say About Premium Demand in Q1 2026?

CCO Andrew Nocella reported that premium revenue grew 14% year-over-year on only 4% capacity growth in Q1 2026, with premium RASM outpacing the main cabin by 4 percentage points.