Key Stats for Snowflake Stock

- Past-Week Performance: +7%

- 52-Week Range: $120.1 to $280.7

- Current Price: $180.5

What Happened?

Snowflake (SNOW) just delivered 30% product revenue growth to $1.23B in Q4 and signed the largest contract in company history, a $400M+ deal, and is currently trading at $180 as the software sector selloff obscures a fundamentally stronger business than existed one year ago.

On February 25, Snowflake reported Q4 remaining performance obligations of $9.77B, up 42% year over year with growth accelerating for the second consecutive quarter, while closing 7 nine-figure contracts in a single quarter versus just 2 in the same period last year.

The AI product inflection that analysts had been waiting for arrived visibly in Q4, with accounts using AI products reaching 9,100, the largest sequential increase ever recorded, and Snowflake Intelligence, the company’s enterprise agent platform, scaling to 2,500 accounts in just 3 months, nearly doubling quarter over quarter.

The Observe acquisition, a $600M deal closed in early February for a market-leading IT observability platform built natively on Snowflake, immediately targets the $50B IT operations market and expands the addressable customer base within Snowflake’s existing installed base of 13,300 customers.

CEO Sridhar Ramaswamy stated on the Q4 FY2026 earnings call that “Snowflake remains at the center of the enterprise AI revolution,” a claim backed by 430+ product capabilities shipped in FY26, a $200M expanded OpenAI partnership, and Cortex Code, the company’s AI coding agent, already adopted by 4,400 customers weeks after launch.

With FY27 product revenue guided at $5.66B representing 27% growth, non-GAAP operating margins expanding to 12.5%, a confirmed Investor Day set for June 1 in San Francisco, and the $1.1B remaining buyback authorization still active, Snowflake enters FY27 with more monetization levers, a deeper enterprise footprint, and faster product velocity than at any prior point in its history.

Wall Street’s Take on SNOW Stock

The $9.77B RPO growing 42% year over year, accelerating for the second consecutive quarter, directly pulls forward the FY27 product revenue guide of $5.66B and makes the 27% growth target look conservative rather than aspirational.

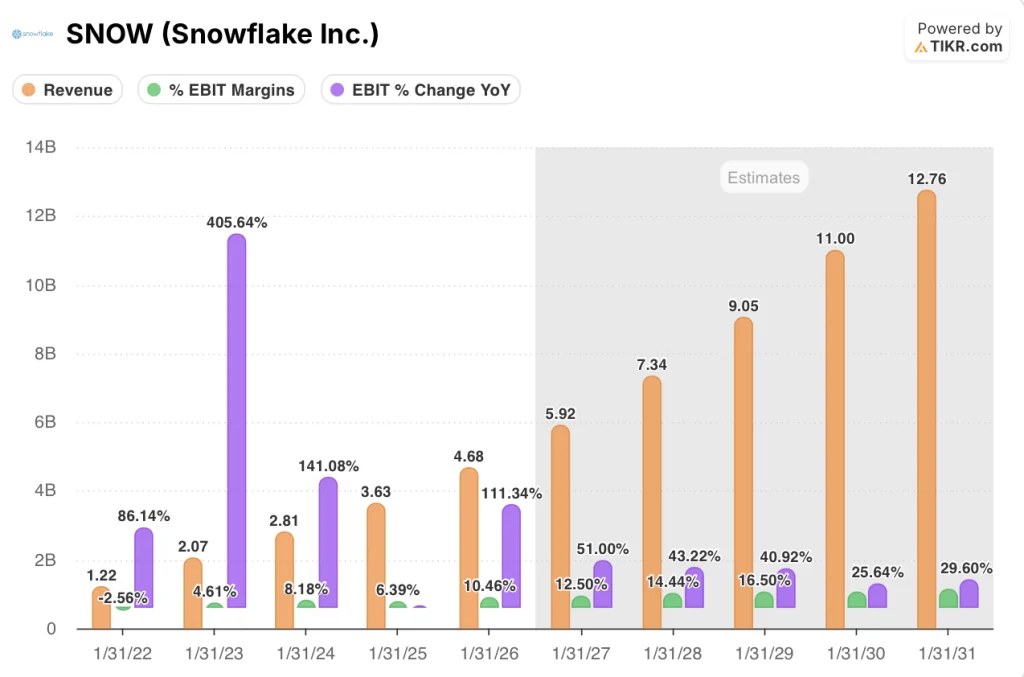

FY26 product revenue reached $4.68B, up 29.2% year over year, while EBIT expanded 111.3% and EBIT margins doubled from 6.4% to 10.5%, proving the growth is now compounding alongside meaningful operating leverage, not against it.

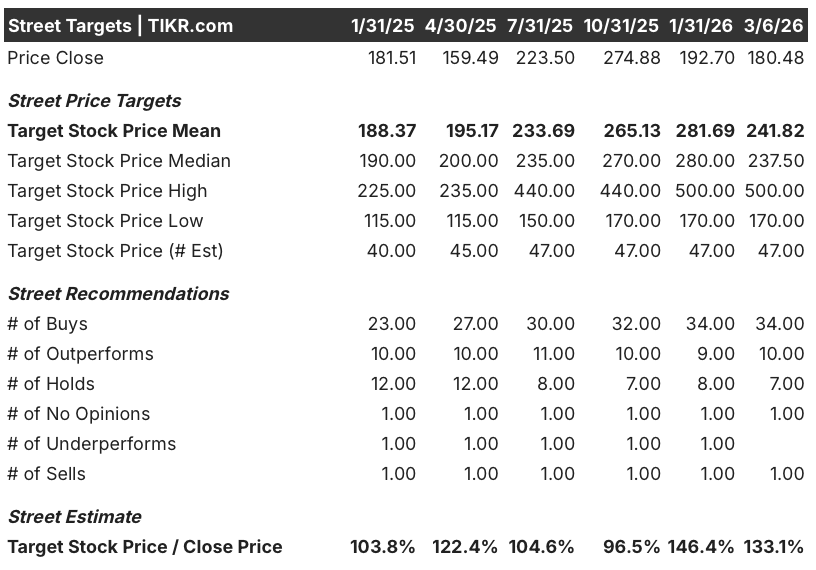

Of the 47 analysts covering SNOW as of March 6, 34 rate it a Buy, 10 Outperform, and 7 Hold, with a mean price target of $241.82 implying 34% upside from the current $180.48, with analysts specifically watching AI product monetization and RPO durability.

The analyst target range spans $170 on the low end to $500 on the high end, where the bear case anchors on the ongoing securities class action and any reemergence of consumption headwinds, while the bull case prices in Cortex Code and Snowflake Intelligence scaling materially into FY27 revenue.

What Does the Valuation Model Say?

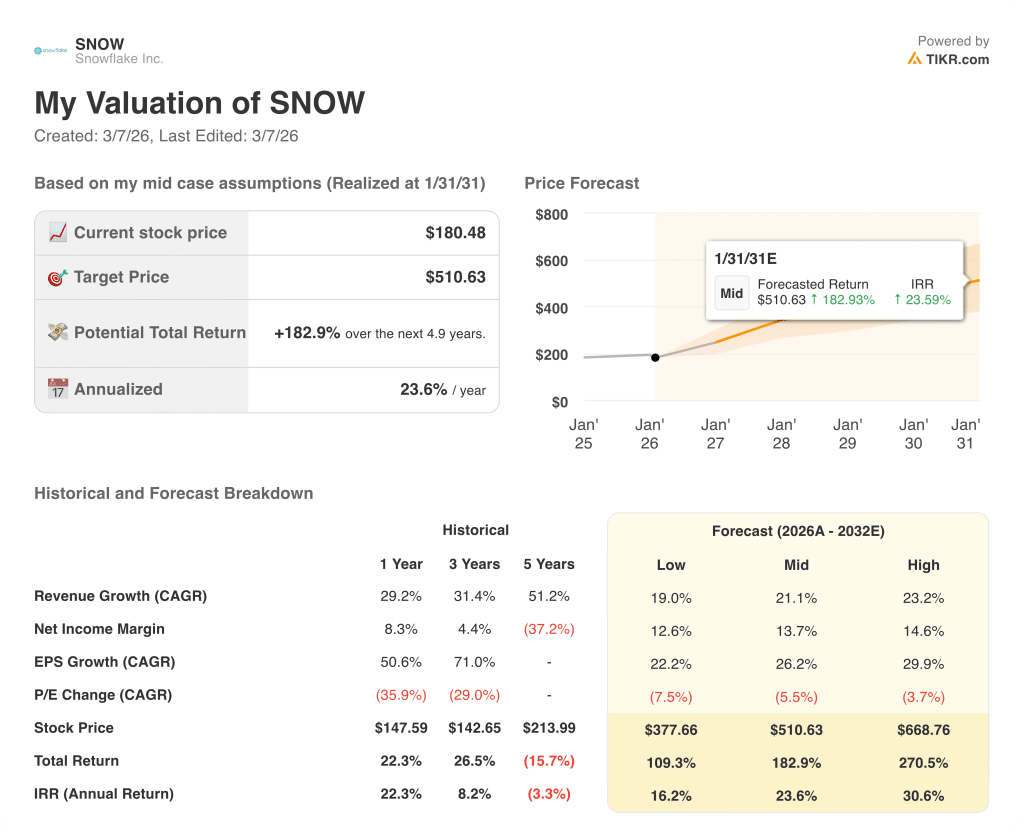

The TIKR mid-case target of $510.63, implying 183% total return and a 23.6% annualized IRR, assumes a 21.1% revenue CAGR and net income margins expanding to 13.7% by FY31. The $400M single-contract win and 7 nine-figure Q4 deals directly support the durability of that revenue growth assumption.

The market is treating SNOW as a consumption-risk name, yet RPO growing 42% and normalized EPS up 50.6% year over year make that discount increasingly difficult to justify.

The Observe acquisition, a $600M platform targeting the $50B IT operations market, expands monetization beyond core data warehousing and directly supports the TIKR model’s multi-year margin expansion path.

Management guided FY27 non-GAAP operating margin at 12.5% while simultaneously absorbing 178 Observe employees, signaling structural efficiency gains that the current $180 price does not reflect.

If AI product adoption stalls and Cortex Code’s 4,400-customer base fails to scale consumption materially, the TIKR model’s 21.1% revenue CAGR assumption breaks and the $510 target collapses toward the $377 low case.

The June 1 Investor Day in San Francisco will be the first major test of whether Snowflake Intelligence and Cortex Code are translating early adoption into durable consumption growth, the single number to watch is Q1 product revenue against the $1.262B–$1.267B guide.

Should You Invest in Snowflake Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SNOW stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snowflake Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SNOW stock on TIKR for Free →