Key Stats for Seagate Stock

- Current Price: $812.73

- Street Target (Mean): ~$815

- TIKR Model Target Price (Mid): ~$1,952

- Potential Total Return: ~140%

- Annualized IRR: ~24% / year

- Earnings Reaction: +11.10% (April 28, 2026)

- Max Drawdown: 21.00% on 3/6/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Seagate Technology Holdings (STX) dropped roughly 7% on May 19 after CEO Dave Mosley said at the JPMorgan Global Technology, Media and Communications Conference that building new factories would “take too long.” It dragged Micron, Western Digital, and SanDisk down with it. Investors who stopped at the headline, though, missed what Mosley was actually saying and why it may matter more for long-term holders than the one-day move.

The tension is real: AI-driven demand for high-capacity hard disk drives (HDDs, the mass-storage hardware central to modern data centers) is running well ahead of what Seagate can produce. Bulls see a supply-constrained business with meaningful pricing power. Bears see a company that just admitted it cannot scale fast enough.

The Selloff Was Built on a Misread

Mosley’s answer on factory expansion was deliberate: new plants would take too long, pull engineering teams off the technology transitions that actually drive exabyte growth, and risk creating surplus capacity. The market heard “we cannot grow.” What Mosley was describing is a different growth model.

More exabytes, the unit of storage output that hyperscaler customers actually buy, come from higher-density platters, not more factory floor space. Moving from 3 terabytes per platter to 4, then to 5, delivers more storage from the same components and the same production lines. As Mosley explained at the conference: “If you’re making a 20-terabyte drive today, at 4 terabytes per platter, that’s 5 discs. At 5 terabytes per platter, it’s 4 discs.” Fewer components, same factory, more exabytes, and, as management has described in prior quarters, 70% incremental margins as volumes scale.

Seagate is targeting mid-20% exabyte CAGR and expects the technology transitions to get there without adding bricks and mortar.

See historical and forward estimates for Seagate stock (It’s free!) >>>

The HAMR News the Market Missed

Mosley confirmed that Mozaic 3, Seagate’s HAMR-based (heat-assisted magnetic recording, a platform using iron-platinum media to store data at higher density) drive, is now qualified at all planned cloud service providers. He also confirmed that Mozaic 4, which supports up to 44TB per drive and was announced in production at two hyperscalers in March 2026, qualified at near-conventional timelines. His expectation for what follows: “I think Mozaic 5 and 6 should be qualified in a much quicker time with the same group of customers.”

That matters because Mozaic 3 took years to qualify at its first hyperscaler. Compressing that timeline removes a risk that weighed on the stock through much of 2024. Seagate expects HAMR to cross 50% of total nearline exabyte shipments in the second half of calendar 2026, the point at which the cost structure fully shifts toward the new platform.

What the Build-to-Order Model Is Doing to the Financials

Seagate’s build-to-order model, where customers commit to volumes four to five quarters in advance, has changed revenue visibility in a way that the old Seagate never had. Lead times on recording head wafers already exceed nine months, so forward commitments align production to real demand rather than forecasts. “Revenue predictability was what I really wanted out of it when we started,” Mosley said. “Now it appears that not only are the forecasts real, but the demand is significantly higher.”

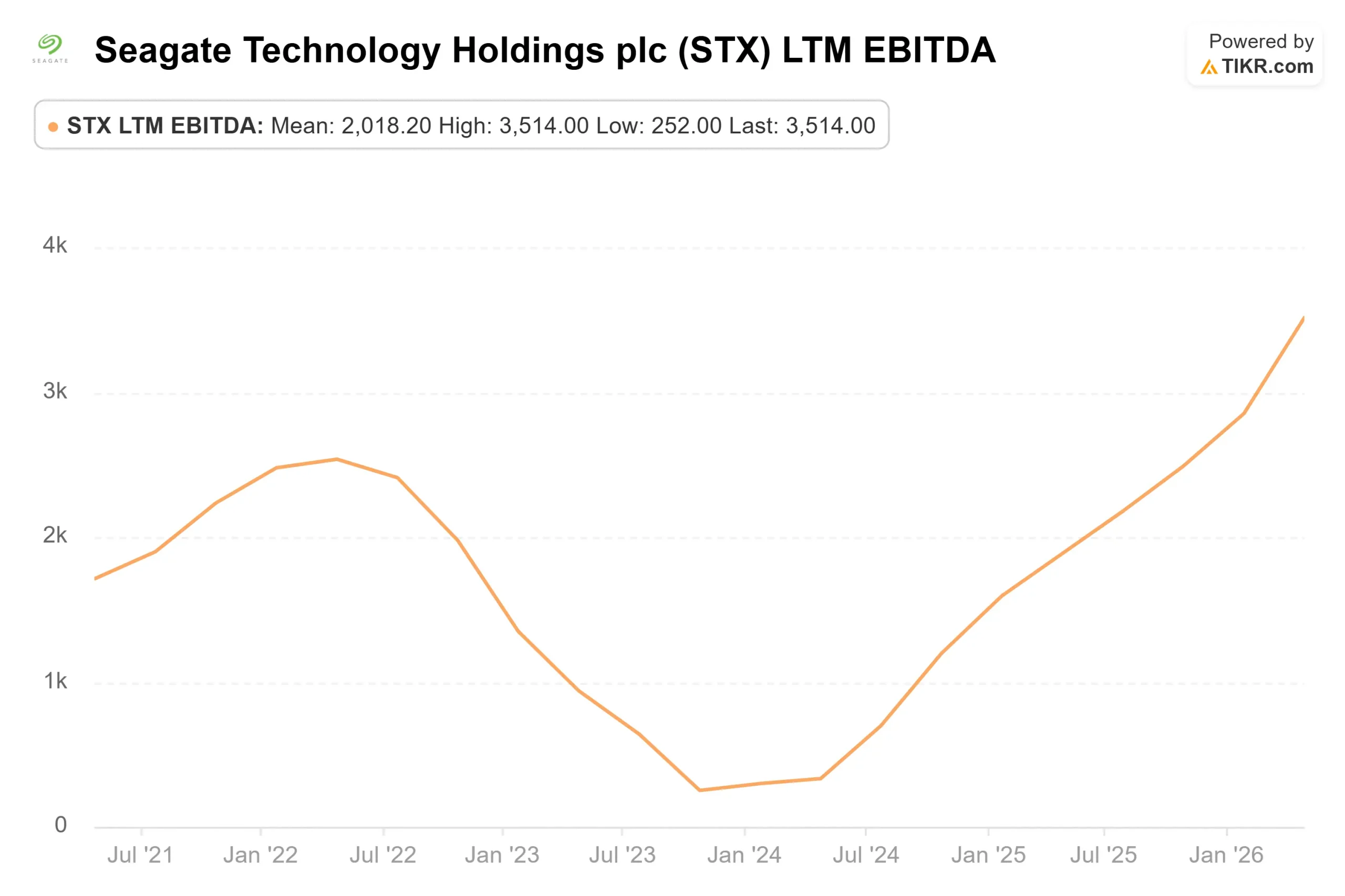

That visibility is showing up in results. According to TIKR’s Beats & Misses data, Seagate beat revenue estimates in five consecutive quarters. In Q3 FY2026, the company reported $3.112 billion in revenue against a $2.963 billion estimate, with adjusted EPS of $4.10, beating the $3.51 consensus by nearly 17%. EBITDA of $1.233 billion beat the $1.104 billion estimate by nearly 12%.

TIKR consensus estimates show revenue growing from around $12 billion in fiscal 2026 toward $33 billion by fiscal 2030, with free cash flow growing faster as operating leverage accumulates.

Is Seagate Undervalued Today?

At 25.94x NTM EV/EBITDA and 34.41x NTM P/E, STX carries a meaningful premium to peers. Western Digital (WDC) trades at 21.02x NTM EV/EBITDA and 31.51x NTM P/E. NetApp (NTAP) trades at 11.88x NTM EV/EBITDA. Seagate’s premium reflects its HAMR technology lead and nearline dominance. It also means execution has to stay ahead of the multiple every quarter.

The Street’s mean target of around $815 based on 22 analysts with price estimates implies the stock is essentially fairly valued on near-term numbers alone. That said, 20 of 26 covering analysts rate it Buy or Outperform, meaning the broader consensus still believes in the multi-year story even if near-term upside looks limited.

The risks are concrete. If hyperscaler capital spending pulls back, pricing power reverses. If HAMR qualification timelines slip, the exabyte crossover gets pushed out. And Seagate is still working through its balance sheet: the company disclosed on May 21 a $185.9 million exchange of convertible notes due 2028 as part of a deliberate debt reduction effort. Mosley confirmed at the conference that returning to 75% free cash flow shareholder returns comes after the balance sheet is in better shape, a meaningful catalyst if the demand cycle holds long enough to get there.

Seagate’s investor relations materials detail the company’s capital return framework and nearline demand outlook for investors wanting to track that timeline.

See how Seagate performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $812.73

- Target Price (Mid): ~$1,952

- Potential Total Return: ~140%

- Annualized IRR: ~24% / year

See analysts’ growth forecasts and price targets for Seagate stock (It’s free!) >>>

The mid case uses a forward revenue CAGR of around 23%, driven by nearline HDD exabyte demand from AI data center buildout and pricing improvement as build-to-order contracts renew. The margin driver is operating leverage, with mid-case net income margins modeled at around 42% over the forecast period. EBITDA is expected to grow from around $4.4 billion in fiscal 2026 toward $17.5 billion by fiscal 2030.

The primary downside: if hyperscaler spending decelerates, revenue growth and the valuation multiple compress together, a double hit that the current P/E does not leave room to absorb. The upside scenario is one where HAMR executes as Mosley described, pricing holds through renewal cycles, and the incremental margin story compounds through the end of the decade.

Conclusion

Watch one number in the Q4 FY2026 earnings report, due in late July 2026: HAMR’s share of total nearline exabyte shipments. Mosley guided HAMR to exceed 50% in the second half of calendar 2026. If Q4 delivers at or above that threshold, the JPMorgan selloff looks like noise. If HAMR comes in well below 40%, the bear case that Seagate’s technology-first strategy cannot meet demand fast enough gains real traction. July will answer the question the conference raised.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Seagate?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Seagate, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Seagate alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Seagate on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!