Key Stats for SanDisk Stock

- Current Price: $1,963.60

- Target Price (Mid): ~$2,810

- Street Target: ~$1,750

- Potential Total Return: ~43%

- Annualized IRR: ~9% / year

- Earnings Reaction: +8.25% (April 30, 2026)

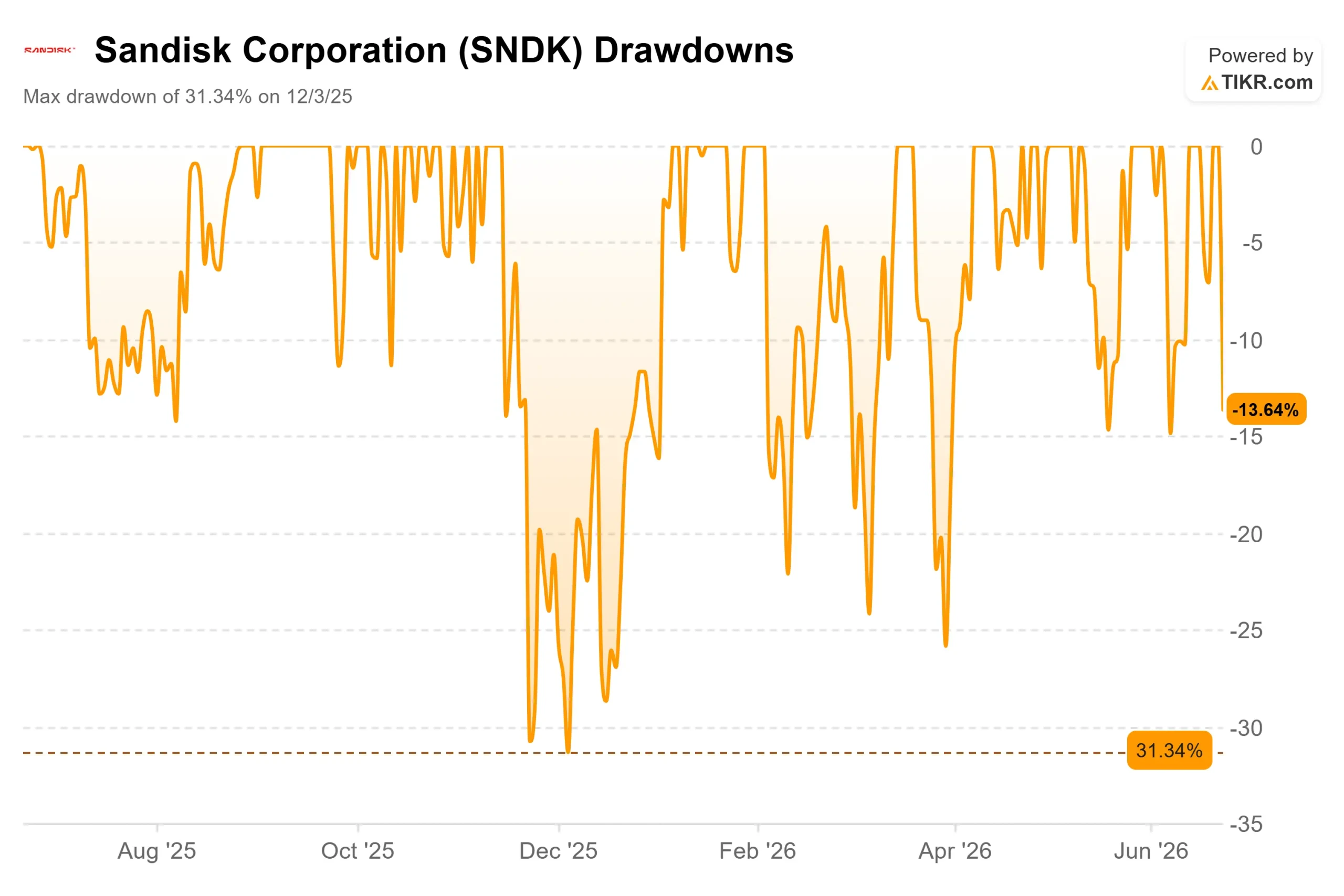

- Max Drawdown: 31.34% (December 3, 2025)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

SanDisk (SNDK) just had the kind of day that reminds everyone what a memory stock can do in reverse. Shares closed June 23, 2026, at $1,963.60, down 13.64%, the worst single session since the company spun out of Western Digital. Nothing broke inside the business. The drop came from 7,000 miles away.

A historic selloff in South Korean chip stocks set it off. SK Hynix and Samsung Electronics both fell more than 12%, the KOSPI dropped roughly 10%, and circuit breakers halted trading twice. That fear crossed the Pacific fast. Micron fell about 11%, and SanDisk led the slide among U.S. memory names. The selloff also landed one day before Micron’s June 24 earnings, the next demand checkpoint for the group.

So the question is no longer whether SanDisk can execute. It is whether a stock up more than 600% in 2026 was ever priced for a day like this. This was the first broad test of the AI memory trade since the spinoff, and it exposed how much optimism sat in the price.

What the selloff was actually about

This was a valuation reset, not a fundamental one. No SanDisk-specific news drove the move. The trigger was sentiment: profit-taking after an extreme run, a fragile tape ahead of Micron, and a Morgan Stanley note flagging stretched memory valuations. When a stock goes vertical, it does not take a broken thesis to spark a 14% drop. Korea just handed the market a reason to sell.

The vulnerability is structural. As a pure-play NAND flash maker, SanDisk has no DRAM or high-bandwidth memory business to cushion a swing in flash sentiment. That focus is the bull case in an upcycle and the risk in a wobble. On a day when the whole memory complex sold off, there was nowhere to hide.

Still, the move barely dents the trend. SanDisk has run from a 52-week low of $40.10 to a high of $2,354.39, and even after this drop it sits near $1,964. The deeper question is whether the gains underneath rest on something durable.

Why the business keeps getting stronger

The fundamentals have moved in one direction. In the March 2026 quarter, SanDisk reported revenue of $5.95 billion and GAAP EPS of $23.03, and the stock rose 8.25% the session after the April 30 release. LTM gross margin now sits at 56.0%, with an LTM EBIT margin of 41.6%. For a business that lost money as recently as fiscal 2025, that is a violent turn.

Management argues this is not the usual cyclical bounce. Speaking at the Mizuho Technology Conference on June 9, CEO David Goeckeler framed the company’s supply deals as the way out of NAND’s boom-and-bust reputation: “We’re not trading duration for price. The value proposition is continuity of supply.” That matters because NAND’s volatility is exactly why the group has always carried a low multiple. Smooth the cycle, and a higher valuation follows.

The mechanics sit with the CFO. Luis Visoso said SanDisk has signed five New Business Model agreements, each with a pricing floor and ceiling so neither side gets whipsawed. His key line: even at the floor, margins “will be consistent with the margins that we guided for the fourth quarter.” A floor that high reframes the cyclicality debate.

There is a second leg still loading. Goeckeler confirmed that fiscal Q4 2026 is the first quarter SanDisk recognizes meaningful revenue from Stargate, its high-capacity enterprise SSD line for AI workloads. One growth engine, the performance NAND used in AI inference caching, is fully ramped. The other is just starting.

See historical and forward estimates for SanDisk stock (It’s free!) >>>

How the valuation looks against peers

Here is what complicates the bubble narrative. After the selloff, SanDisk trades at 11.76x NTM P/E and 8.50x EV/EBITDA. That is not an expensive stock on forward earnings. Western Digital, its former parent, trades at 42.54x P/E and 29.01x EV/EBITDA. Samsung sits cheaper at 5.52x and 3.50x, reflecting its conglomerate mix.

So SanDisk sits between a far pricier WDC and a cheaper, more diversified Samsung. The discount to Western Digital is hard to square given SanDisk’s faster growth and stronger near-term margins, which suggests the market is pricing real doubt about how long elevated NAND pricing lasts. On forward earnings, this is not a stock that has detached from reality. The risk lives in the durability of the “E,” not the multiple.

The balance sheet supports the case. SanDisk now holds a net cash position, with LTM net debt of negative $3.53 billion, and management announced a $6 billion buyback alongside earnings.

See how SanDisk performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $1,963.60

- Target Price (Mid): ~$2,810

- Potential Total Return: ~43%

- Annualized IRR: ~9% / year

See analysts’ growth forecasts and price targets for SanDisk stock (It’s free!) >>>

The mid case is the right anchor because it leans on contracted revenue rather than peak-cycle pricing, the exact variable the market is worried about. Two revenue drivers do the work: data center and enterprise SSD demand pulling NAND into its largest-ever end market, and the New Business Model agreements that convert spot-priced commodity sales into multi-year contracted volume. The margin driver is mixed, as enterprise SSD and Stargate volume lift blended margins above anything the consumer business produced. The primary risk is the oldest one here: an oversupply cycle that breaks pricing before contracts can absorb it.

The upside: supply agreements hold, margins stay near the floor, and NAND earns a higher multiple as its cyclicality fades.

The downside: AI memory demand cools, new capacity floods the market, and the stock re-rates back toward commodity-cycle math.

Conclusion

The next answer comes from Micron, then from SanDisk itself. Micron’s June 24 earnings will tell the group whether AI memory demand is still accelerating, and SanDisk will trade on that read before it reports fiscal Q4 in early August. On that print, watch whether margins land near management’s contracted floor. Hold the line, and the structural story holds. A clear miss would be the first hard evidence that the cycle is reasserting itself. The Street is still firmly behind the name, with 15 Buys, three Outperforms, three Holds, one Underperform, and one Sell. Until the data says otherwise, this was a stock catching its breath near a record, not a thesis coming apart.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in SanDisk?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SanDisk, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SanDisk alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze SanDisk on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!