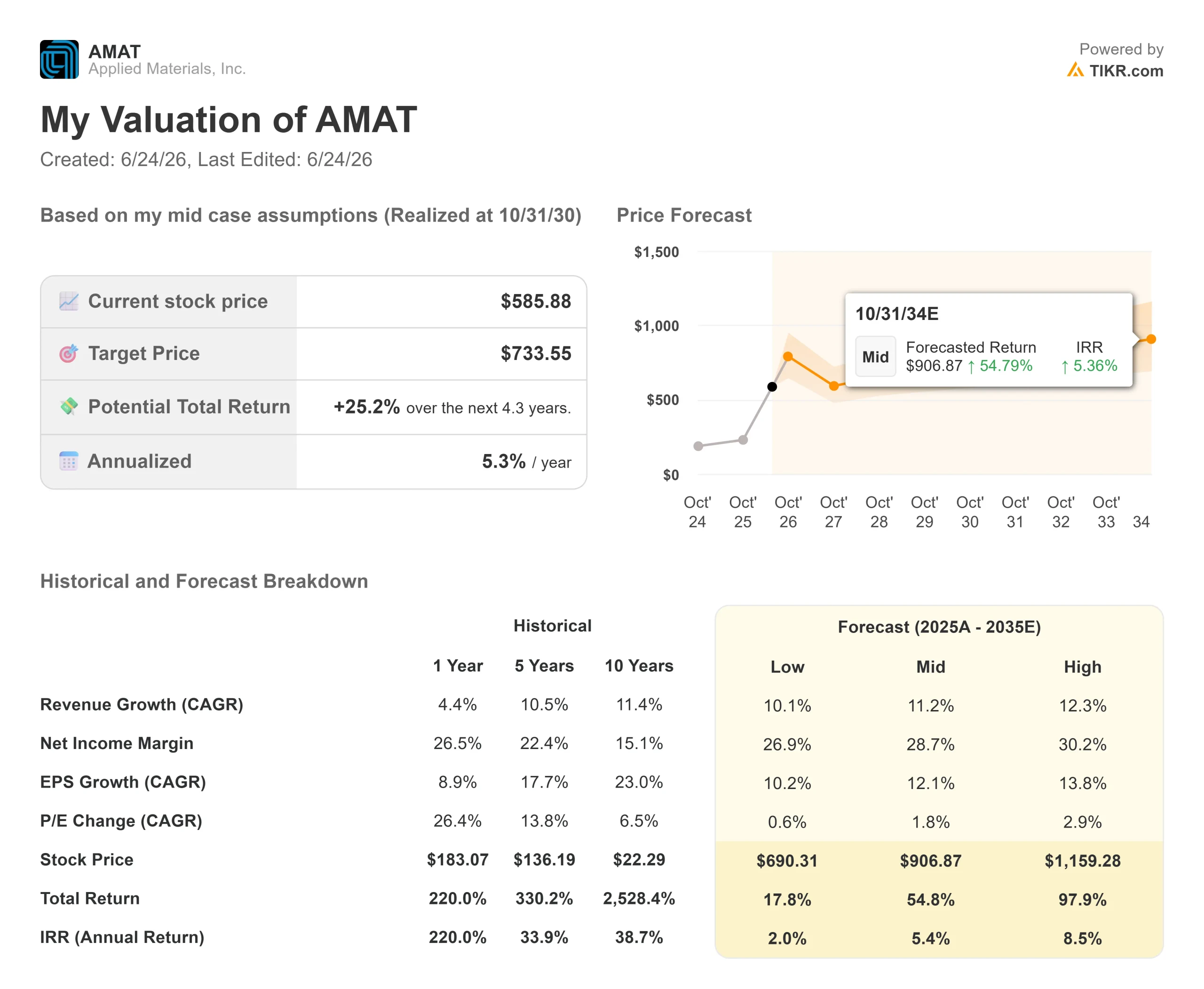

Key Stats for Applied Materials Stock

- Current Price: $585.88

- Target Price (Mid): ~$730

- Street Target (Mean): ~$530

- Potential Total Return: ~25%

- Annualized IRR: ~5% / year

- Earnings Reaction: -0.89% (May 14, 2026)

- Max Drawdown: -21.60% (September 3, 2025)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Applied Materials, Inc. (AMAT) fell 8.48% on June 23 to close at $585.88, a sharp reversal from a stock that had just touched its 52-week high of $641.18. That drop landed the same day Bank of America raised its price target to $720 from $540.

That contradiction is the story. A major bank told clients the stock was worth more, and it fell anyway. When a target hike and a selloff arrive together, the market is usually pricing something the upgrade ignored.

Why the Stock Dropped on an Upgrade

The selloff was about positioning, not the business. Applied makes the deposition and etch tools chipmakers use to build transistors, and demand is near record levels. But shares had run up sharply over the prior month, leaving the stock priced for perfection on a day the Nasdaq fell 2.22%.

Underneath the profit-taking sat a sharper signal. In mid-June, insiders sold more than $65 million of stock, disclosed through SEC Form 4 filings, led by CEO Gary Dickerson’s roughly $42.6 million sale. Insiders still hold large stakes, and such sales often follow preset plans. Still, when leadership trims near a high, the market reads it as caution on price.

There was also a fundamental wrinkle. Despite record revenue, free cash flow came in at just $210 million last quarter, well below the roughly $1.6 billion analysts expected. Investors paying 55 times earnings for a cyclical name noticed.

What Management Actually Said About Demand

The bull case did not weaken, which is why targets keep rising. At the Bank of America Global Technology Conference on June 2, CFO Brice Hill described demand with almost no ceiling, citing the raised “over 30% growth” outlook for the semiconductor systems business.

His framing of the constraint matters most. “Demand right now is metered by clean room space,” Hill said, explaining that customers optimize existing fabs while new ones take three to four years to build. The orders are real and waiting, not speculative. Hill also flagged a margin story, noting the equipment business runs at 54.8% gross margins on more disciplined, value-based pricing.

The case in one line: demand is visible, the constraint is physical, and pricing power is improving. The debate is how much of that the stock already reflects at $586.

See historical and forward estimates for Applied Materials stock (It’s free!) >>>

How the Valuation Stacks Up Against Peers

On forward EV/EBITDA, Applied trades at 33.88x, below KLA Corporation at 42.54x and Lam Research at 42.13x, and near ASML Holding at 34.86x. That discount to KLA and Lam is the re-rating question bulls keep raising, since Applied’s portfolio is the broadest in the group.

Part of the discount is earned. China ran at roughly 24% of systems and services revenue last quarter, per Hill, and that exposure weighs on the multiple in a way it does not for less China-reliant peers. A gap partly earned, and partly opportunity, tends to close slowly, and only if the China overhang fades.

See how Applied Materials performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $585.88

- Target Price (Mid): ~$730

- Potential Total Return: ~25%

- Annualized IRR: ~5% / year

See analysts’ growth forecasts and price targets for Applied Materials stock (It’s free!) >>>

That is a modest return, because the run-up already captured much of the upside. The mid-case rests on two revenue drivers: AI equipment demand across leading-edge logic, DRAM, and advanced packaging, where Hill says Applied leads; and services compounding in the mid-teens as the installed base grows. The margin driver is value-based pricing, which lifted equipment gross margins to 54.8%. The main risk is China, where tighter export rules could cut a quarter of core revenue fast.

The upside: if AI capacity sustains the over-30% systems growth into 2027, the high case opens above the mid-case target.

The downside: a China shock or a memory-pricing pause would expose a stock at 55 times earnings with little room for error.

Conclusion

The next test is fiscal Q3 earnings, expected August 13, 2026. A revenue beat with Hill’s 8-quarter customer visibility holding firm confirms the demand is converting and keeps the high case alive. Any guidance wobble says the stock priced a cycle the fundamentals had not yet delivered.

Watch free cash flow alongside the headline number. Record revenue with weak cash conversion is a divergence that rarely lasts in either direction. August 13 is when the market finds out which way it breaks.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Applied Materials?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Applied Materials, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Applied Materials alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Applied Materials on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!