Key Stats for POOL Stock

- 52-Week Range: $172.68 – $345.00

- Current Price: $195.00

- Street Mean Target: ~$256

- TIKR Target Price (Mid): ~$285

- TIKR Annualized IRR (Mid): ~9% per year

- Q1 2026 Net Sales: $1.14B (up 6% year over year)

- Q1 2026 Diluted EPS: $1.45 (up 2%, or 8% excluding tax items)

- Q1 2026 Operating Income: $82.6M (up 7% year over year)

- FY2026 EPS Guidance: $10.87 – $11.17

- Share Buybacks Last 12 Months: ~$349M

Value your favorite stocks like POOL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The Business Nobody Talks About That Touches 6 Million Pools

Pool Corporation (POOL) is not a pool builder. It is the distributor that sits between manufacturers and the contractors, retailers, and service companies that build, maintain, and repair pools.

With 455 sales centers across North America, Europe, and Australia, POOL controls roughly a third of the U.S. pool supply distribution market, a dominant position built over decades that gives it pricing leverage, supplier relationships, and logistics scale that competitors cannot easily replicate.

The installed base of roughly 6 million pools in the United States is the foundation of the business. Pools require year-round maintenance regardless of whether anyone is building new ones.

Chemicals, filters, pumps, and replacement parts keep selling through housing downturns, rate cycles, and swings in consumer sentiment. CEO Peter Arvan described Q1 as a continuation of that dynamic, noting that maintenance demand remained resilient while discretionary categories like new construction and remodeling continue to recover gradually.

Net sales grew 6% to $1.14 billion in Q1, beating analyst estimates by nearly 4%. Operating income grew 7%, and the operating margin expanded 10 basis points to 7.3%, a modest but meaningful improvement that shows the cost structure is beginning to be leveraged after years of greenfield investment.

Pool Corporation beat Q1 estimates, and insiders are buying in size. Track POOL stock’s revenue trends, EPS path, and valuation on TIKR for free →

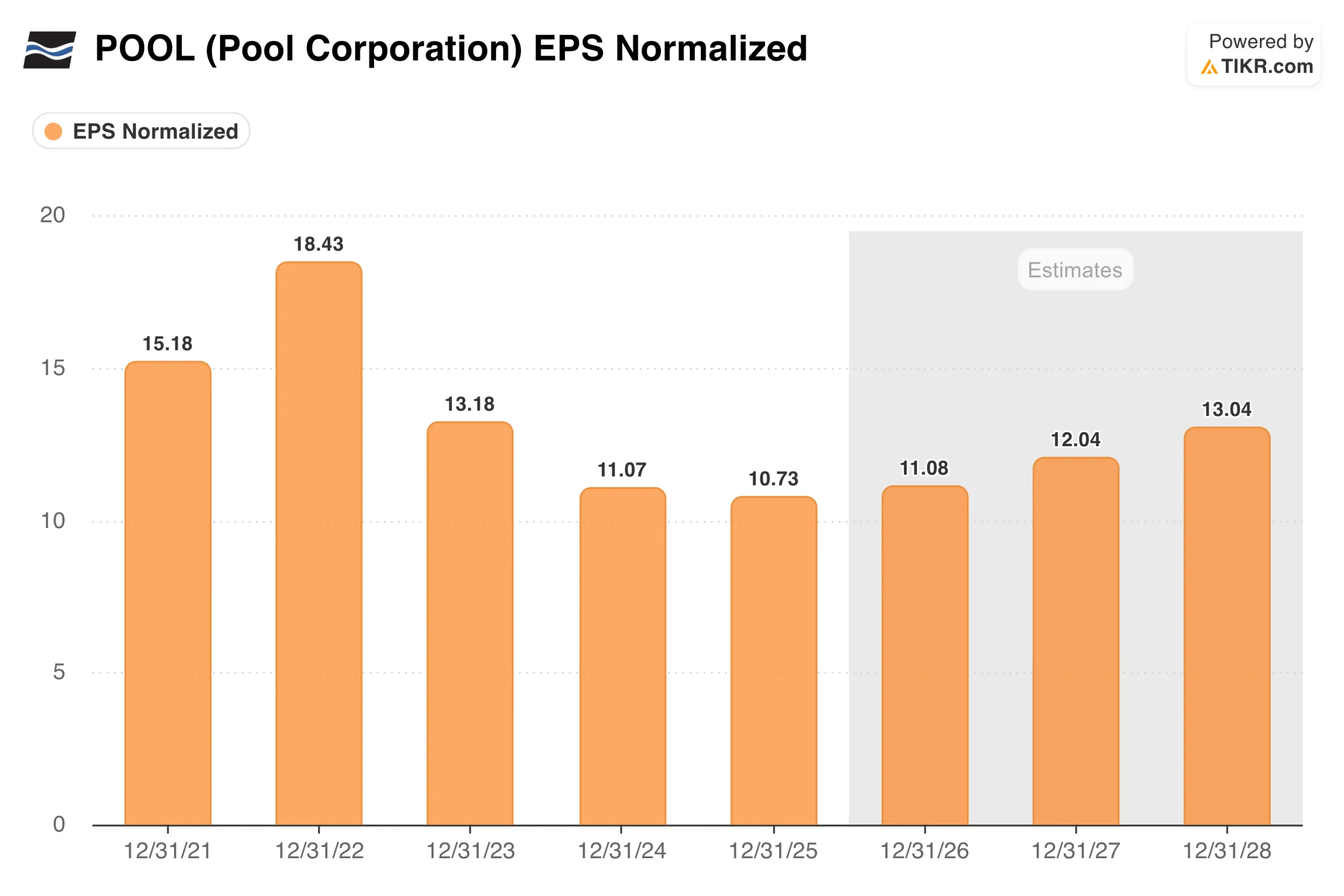

What the EPS Chart Shows About Where POOL Has Been and Where It’s Going

The EPS chart tells the clearest version of the Pool Corporation investment story. Earnings peaked at $18.43 in 2022, the height of the pandemic pool construction boom when backlog was long, pricing was strong, and new pool permits hit multi-decade highs.

The hangover has been real, EPS has declined every year since, reaching $10.73 in 2025, a 42% drop from the peak.

The consensus estimate embedded in the forward curve is a slow, modest recovery toward $13 by 2028. That path assumes new pool construction stabilizes near current levels of around 58,000 units annually, maintenance demand holds steady, and pricing initiatives gradually restore some of the margin that compressed during the downcycle.

It does not assume a housing boom or a return to pandemic-era demand. The question for investors is whether $10.73 represents a durable earnings floor or whether further pressure from weak discretionary spending could push it lower before the recovery begins.

See analysts’ growth forecasts and price targets for POOL stock (It’s free!) >>>

Free Cash Flow Tells a More Nuanced Story Than the Headlines Suggest

The FCF chart needs context to read correctly. The $828 million peak in 2023 was not a reflection of business acceleration, it was largely the result of inventory destocking after the pandemic boom, as POOL worked down elevated stock levels and converted inventory back to cash.

The subsequent decline to $310 million in 2025 reflects the business returning to a more normal inventory investment cycle as it stocks for new greenfield locations and supports a broader product range ahead of the season.

The more instructive data point is that POOL has generated positive free cash flow in every year shown, including through the worst of the post-boom correction. For a distributor operating in a cyclical industry, that consistency is the core of the quality argument.

The company used that cash to repurchase roughly $349 million in shares over the past twelve months while maintaining a manageable leverage ratio of 1.73x EBITDA, well within its target range of 1.5 to 2.0x.

What the Valuation Model Says About a Stock Trading Near a 3-Year Low

The TIKR model mid-case targets around $285, implying roughly 9% annually over the next 4.5 years, driven by modest revenue growth and slight margin expansion.

At $195 and roughly 17x forward earnings, the stock trades below its historical average, with the street mean target of around $256 implying 31% upside. The scenario range skews positive, making this less a debate about business quality and more a question of how long investors are willing to wait for the construction cycle to turn.

What the Bulls Are Betting On

- The maintenance base provides a durable earnings floor. Roughly 6 million pools require regular chemical treatments, equipment servicing, and parts replacement, regardless of new construction activity, giving POOL a recurring revenue stream that competitors cannot disintermediate

- Variable speed pump replacement is a near-term tailwind. Pumps installed during the 2018 regulatory transition are now entering their natural replacement cycle, providing a non-discretionary equipment demand boost that management specifically called out

- Greenfield investments are beginning to leverage. POOL opened 50+ new sales centers over the past five years and is starting to see operating expense leverage as those locations mature, which should expand margins as revenue grows

What the Bears Are Watching

- New pool construction remains depressed. At around 58,000 units annually, new builds are running well below the 2021 to 2022 peak of over 100,000, and a sustained housing market recovery requires both lower rates and improved consumer confidence

- The EPS recovery is slow and dependent on macro conditions. The consensus path back toward prior earnings levels assumes several years of modest growth, leaving limited room for error if discretionary spending weakens further

- The stock has been a value trap since 2022. Investors have been waiting for the construction cycle to turn for three years, and each quarter of gradual improvement has not been enough to re-rate the multiple

See analysts’ growth forecasts and price targets for POOL stock (It’s free!) >>>

Should You Invest in Pool Corporation

Pool Corporation is a high-quality business going through a cyclical trough. The maintenance base keeps it profitable, the balance sheet is sound, and the company is buying back stock near multi-year lows. The question is not whether the business is good, it clearly is, but whether the discretionary recovery arrives on the timeline the model assumes. At 17x forward earnings with a street target implying 31% upside, the stock offers a reasonable entry point for investors willing to be patient. For those who need the cycle to turn quickly, the wait has already been longer than most expected.

Put TIKR to work on your own research. You can build your own valuation model on POOL or analyze every other stock on your radar. No credit card required. Just the tools you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!