Key Stats for BOX Stock

- 52-Week Range: $21.34 – $36.41

- Current Price: $25.39

- Street Mean Target: $32.50

- TIKR Target Price (Mid): ~$45

- TIKR Annualized IRR (Mid): ~7% per year

- Q1 FY2027 Revenue: $306M (up 11% year over year)

- Q1 FY2027 Non-GAAP EPS: $0.37

- Q1 FY2027 Non-GAAP Operating Margin: 27.7%

- FY2027 Revenue Guidance: ~$1.28B (up ~9% year over year)

- Remaining Share Buyback Authorization: ~$445M

Most investors never know if a stock is truly undervalued or overpriced. TIKR’s professional-grade valuation tools give you a clear, data-backed answer across 60,000+ stocks for free →

Enterprise Advanced Is Doing What Box Needed It to Do

Box (BOX) is an intelligent content management platform, a secure place for enterprises to store, manage, and increasingly, process unstructured data using AI. For most of its history, the market viewed Box as a mature file storage business growing slowly and fighting for relevance against Microsoft and Google.

The Enterprise Advanced tier, a higher-priced subscription that connects company content directly to AI agents, is the product that changes that framing.

Q1 fiscal 2027 marked Box’s first double-digit revenue growth quarter in over three years, with revenue reaching $306 million, up 11% year over year. Enterprise Advanced carries a 30-40% price premium over the standard Enterprise Plus tier, and customers are adopting it specifically to build intelligent workflows on top of their content.

CEO Aaron Levie noted that Box served as an early launch partner for GPT-5.4, Claude Opus 4.7, and the OpenAI Agent SDK, positioning it as content infrastructure for the agentic AI era rather than just a storage vendor.

Record Q1 bookings and four consecutive quarters of accelerating revenue growth suggest the product motion is gaining traction, not just generating early-adopter buzz.

See analysts’ full growth forecasts and estimates for BOX stock (It’s free) >>>

Revenue Is Climbing, and Margins Are Following

The revenue and operating margin chart captures Box’s transformation over the past five years. Revenue has grown steadily from $771 million in FY2021 to $1.18 billion in FY2026, while GAAP operating margins have moved from deeply negative territory to nearly 8%.

The non-GAAP picture is considerably stronger, Box is guiding for roughly 28% non-GAAP operating margin for the full fiscal year, a level that reflects genuine operating leverage as the business scales without proportionally adding headcount or infrastructure costs.

The combination of accelerating revenue and expanding margins is exactly what investors want to see from a maturing SaaS business.

Box is not growing at hypergrowth rates, but it is growing faster than it was a year ago while simultaneously becoming more profitable, which is the profile that tends to attract attention from value-oriented software investors.

Estimate a company’s fair value instantly (Free with TIKR) >>>

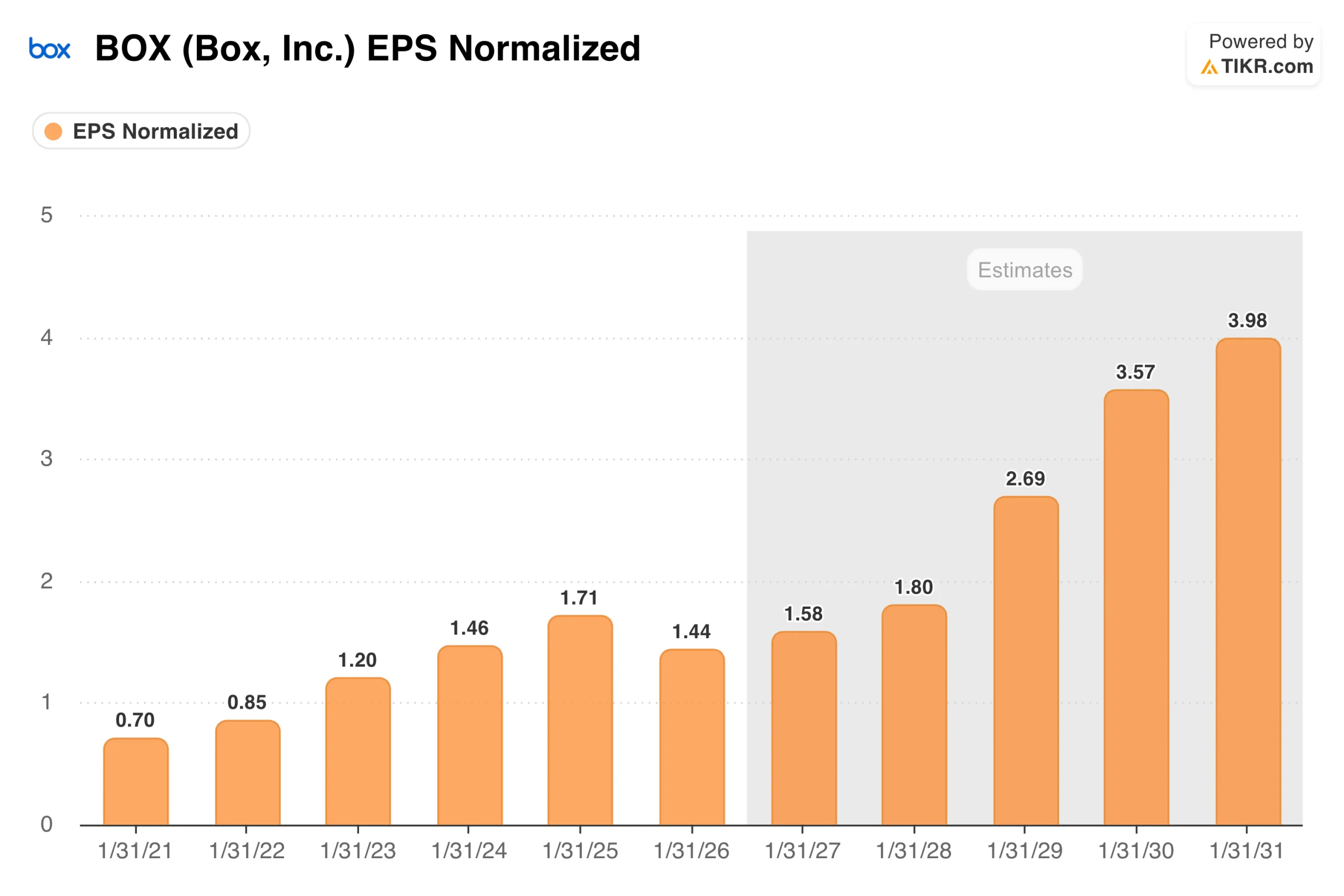

What the EPS Chart Shows About Box’s Long-Term Earnings Power

Normalized EPS dipped to $1.44 in FY2026 before the estimates curve projects a steady climb toward $3.98 by FY2031. The FY2026 dip is worth understanding in context; it reflects the transition period as Box invested in its AI platform while absorbing foreign-exchange headwinds that were 260 basis points worse than expected in Q1 alone.

Management guided full-year FY2027 non-GAAP EPS of approximately $1.56, and the consensus curve beyond that reflects analysts pricing in the compounding effect of Enterprise Advanced adoption on both revenue and margins.

The long duration of this chart matters for thinking about BOX as an investment. The earnings power being estimated in FY2029 and beyond depends on AI agents becoming routine consumers of enterprise content, with Box serving as the secure layer through which those agents operate.

That is a reasonable bet, but it is still early enough that the timing carries real uncertainty.

What the Valuation Model Says About a Stock Trading Near Its 52-Week Low

The TIKR model mid case targets around $45, implying a total return of roughly 78% over the next 4.6 years, or about 7% annually.

The high case reaches around $56, translating to roughly 10% per year. The return in both scenarios is driven by a combination of revenue growth around 6-7% annually and modest net income margin expansion toward 18%, with the P/E contracting slightly over time.

The scenario range skews to the upside, with the low case still implying a positive annual return of around 4%.

At $25, BOX trades near its 52-week low despite just posting its best revenue growth quarter in three years. The street mean target of $32.50 implies roughly 28% upside, and the TIKR model suggests the market may be underweighting the earnings power that Enterprise Advanced can generate as it scales.

What the Bulls Are Betting On

- Enterprise Advanced is a genuine re-rating catalyst. A 30-40% price premium on a growing share of the customer base compounds meaningfully on a $1.3 billion revenue base, and the net retention rate is guided to reach 105% by year’s end

- AI agents need a secure content layer. Box’s positioning as the enterprise-grade platform for unstructured data gives it a credible role in the agentic AI stack that pure storage vendors cannot easily replicate

- Margin expansion has room to continue. Moving from negative GAAP operating margins in FY2021 to nearly 28% non-GAAP today shows the cost structure is well-controlled, and further scale should push that higher

What the Bears Are Watching

- Revenue growth is still modest in absolute terms. Nine to ten percent growth is an improvement, but it is not the acceleration that typically commands a premium multiple in software

- Microsoft and Google remain formidable. Both competitors offer content management capabilities bundled into broader productivity suites, and enterprise IT consolidation could pressure Box’s standalone value proposition

- FX headwinds are a persistent drag. International revenue is a meaningful portion of Box’s business, and currency movements have consistently created gaps between reported and constant-currency results

Explore all three Box stock scenarios with the full model on TIKR and build your own assumptions from institutional-quality data. Run the Box stock valuation model on TIKR for free →

Should You Invest in Box

Box is a slow-burning story that just showed its first sign of acceleration. The Enterprise Advanced tier is working, margins are expanding, and the AI agent narrative gives the company a credible path to re-rating if it can demonstrate that its platform becomes essential infrastructure rather than just a premium storage option.

The TIKR model mid case at around 7% annually is not a high-conviction return, but the low case still implies positive returns, which limits the downside framing here.

The stock trading near its 52-week low while posting its best growth in three years is the kind of disconnect that tends to resolve one way or the other relatively quickly.

Put TIKR to work on your own research. You can build your own valuation model on BOX or analyze every other stock on your radar. No credit card required. Just the tools you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!