Key Takeaways for Tesla Stock

- Tesla (TSLA) posted Q1 2026 revenue of $22.39 billion, up 16% year-over-year.

- Gross margins expanded to 21% in Q1 2026, recovering from a trough of 16% in mid-2025.

- Operating income rebounded 91% year-over-year to $0.94 billion in the most recent quarter.

- TIKR’s model values Tesla stock at approximately $1,624 by December 2030, implying around 300% total return.

The Q1 gross margin recovery is real, but TSLA’s operating cost structure is absorbing every dollar of it. Pull up Tesla’s full income statement on TIKR to see exactly where the leverage is — and where it isn’t. Access the data on TIKR for free →

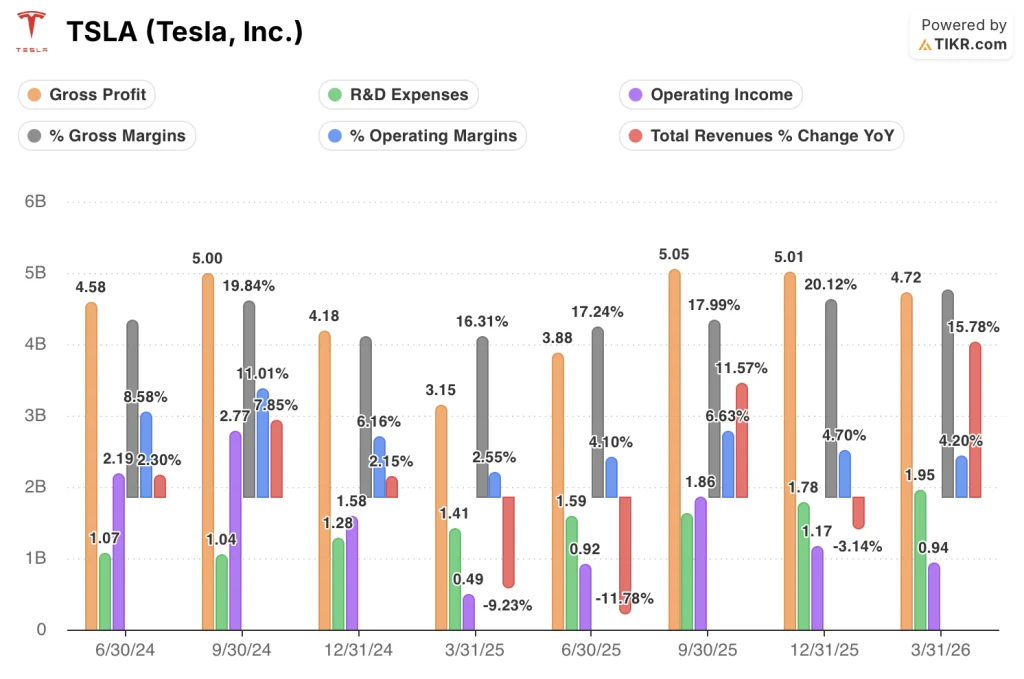

Tesla Stock’s Gross Margin Climbs Back to 21% While R&D and SG&A Reset the Floor

Tesla, Inc. (TSLA) posted Q1 2026 revenue of $22.39 billion, a 16% year-over-year increase that reversed five consecutive quarters of declining or flat top-line growth.

The revenue recovery was broad-based: CFO Vaibhav Taneja cited EMEA as a standout, with France and Germany each posting over 150% quarter-over-quarter growth in deliveries.

The company ended Q1 with its highest order backlog in over two years, a signal that underlying demand has recovered independently of macro support.

FSD paid subscriber growth reached nearly 1.3 million customers globally, with Taneja noting that subscriber churn is declining as product quality improves.

Cybercab production began at Gigafactory Texas during Q1, and Tesla Semi volume production is expected to follow in the coming months.

Elon Musk stated that Optimus start-of-production is targeted for the late July to August window, with a second Optimus factory under construction at Giga Texas.

Musk also confirmed over $25 billion in planned 2026 capital expenditure, approximately triple 2025 levels, with investments spanning AI infrastructure, new factories, and a research semiconductor fab.

On Robotaxi, Tesla expanded unsupervised operations to Dallas and Houston, with Musk targeting roughly a dozen states by year-end, while noting that Robotaxi revenue will not be material until 2027.

Q1’s gross margin story is the clearest signal Tesla has printed in two years — explore the full income statement on TIKR to see how operating leverage is building behind it. Access the income statement on TIKR for free →

Tesla’s 21% Gross Margin Signals Pricing Power Recovery, but R&D Spending Holds Operating Margins Near 4%

Tesla’s gross margin reached 21% in Q1 2026, the highest level since Q3 2024 and a meaningful recovery from a trough of 16% in mid-2025.

Gross profit grew 50% year-over-year to $4.72 billion, compounding at roughly three times the rate of the 16% revenue gain.

Meanwhile, R&D hit $1.95 billion, a record high in the data set, as Tesla accelerated investment in AI5 chip development, Optimus, Cybercab, and FSD software architecture.

Operating income rebounded 91% year-over-year to $0.94 billion, confirming the year-over-year improvement is real.

Operating margins came in at 4%, still near multi-year lows, because expanding R&D absorbed the gross profit recovery before it could convert to operating leverage.

Tesla Leads Ford and GM on Gross Margin at 21%, but the Gap Has Narrowed Over Eight Quarters

Tesla’s gross margin reached 21% in Q1 2026, the highest in the three-company peer set and a recovery from a trough of 17% in Q2 2025.

Ford (F) posted 12% gross margin in Q1 2026, its strongest reading since Q3 2024, recovering from a low of 6% in Q2 2025.

General Motors (GM) held at 11% in Q1 2026, roughly flat across the eight-quarter data set, with no meaningful expansion or contraction in either direction.

Tesla’s gross margin lead over Ford widened from roughly 11 points at the Q2 2025 trough to roughly 9 points in Q1 2026, as Ford’s recovery outpaced Tesla’s on a relative basis during the rebound period.

The structural picture is that Tesla maintains a gross margin premium of roughly 10 points over both legacy peers, but Ford’s Q1 2026 reading of 12% represents its strongest quarterly gross margin since the data set begins, narrowing the gap at the margin.

Is Tesla Stock Undervalued in 2026? TIKR’s $1,624 Model Points to 300% Upside

TIKR’s model values Tesla at approximately $1,624 by December 2030, implying around 300% total return from the current price of $406, or roughly 36% per year.

For that target to hold, the gross margin recovery demonstrated in Q1 needs to compound while R&D and operating costs scale more slowly than gross profit.

The 91% year-over-year rebound in operating income sets the directional case, but the cost trajectory through Tesla’s $25 billion capex cycle will determine whether operating leverage follows.

TIKR’s valuation model lays out exactly what revenue, margin, and earnings assumptions are embedded in that $1,624 target. Explore the full model on TIKR for free →

Should You Invest in Tesla, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Tesla, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Tesla, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TSLA stock on TIKR for Free →

What did Tesla say about Robotaxi revenue in Q1 2026?

Elon Musk stated on the Q1 2026 earnings call that Robotaxi revenue will not be material in 2026, with meaningful contribution expected in 2027 as unsupervised operations expand across states.