Key Takeaways for Caterpillar Stock

- Total revenues grew 22% year-over-year to $17.4 billion in Q1 2026, beating Street estimates by roughly 6%.

- Operating margins recovered to 18%, up from a trough of 16% in the prior quarter, as favorable manufacturing costs offset $600 million in tariff headwinds.

- Caterpillar raised its full-year 2026 revenue outlook to low double-digit growth, supported by a record $63 billion backlog.

- TIKR’s model values CAT stock at approximately $1,291 by December 2030, implying around 42% total return from the current price of $911.

CAT Stock Posts 22% Revenue Growth: Can Operating Margins Hold the Recovery Through Tariffs?

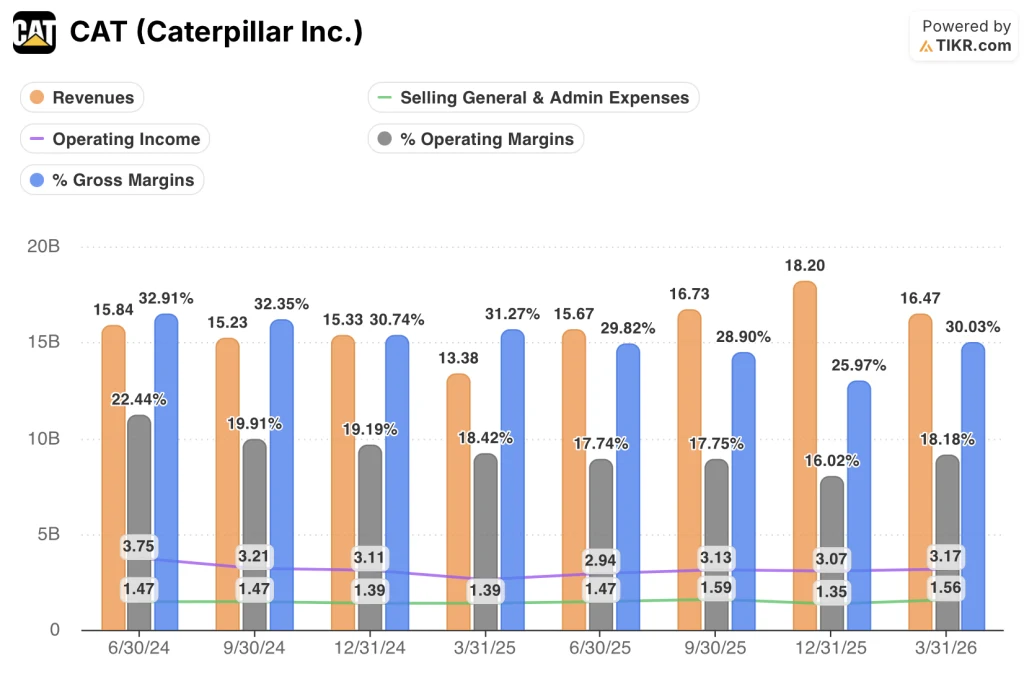

Caterpillar Inc. (CAT) delivered $17.4 billion in Q1 2026 revenues following its April 30 earnings call, marking a 22% year-over-year jump that beat Street expectations and signaled the company’s strongest demand environment in years.

The headline growth was broad-based: Power and Energy (the segment supplying generators and turbines for data centers, oil and gas pipelines, and industrial applications) posted 22% sales growth to $7.0 billion, while Construction Industries surged 38% to $7.2 billion on a seasonally typical dealer inventory build.

Backlog grew to a record $63 billion, a 79% increase versus Q1 2025, with CEO Joe Creed noting in Q1 earnings call that “total first quarter orders were an all-time record.”

The forward catalyst is the company’s decision to expand large reciprocating engine capacity from 2x to nearly 3x 2024 levels, targeting power generation demand driven by data center build-out for cloud computing and AI.

Creed made the investment case explicit: “Since we first announced our initial capacity expansion plans in January of 2024, our large reciprocating engine backlog has grown by more than 3.5x.”

Power generation sales to users grew 48% in the quarter for large gensets and turbines, with an increasing mix shifting toward prime power applications that carry significantly higher long-term services revenue than standby diesel gensets.

Management now expects full-year 2026 revenues to grow in the low double digits and raised its MP&E free cash flow outlook above the $9.5 billion achieved in 2025.

Caterpillar’s Operating Margin Recovery in 2026: One Quarter Doesn’t Confirm the Inflection

Caterpillar’s operating margin recovered to 18% in Q1 2026, bouncing from a trough of 16% in Q4 2025 as favorable manufacturing costs partially absorbed a $600 million tariff headwind.

Revenue of $17.4 billion represented a 22% year-over-year gain, the sharpest acceleration in the trailing eight quarters.

Gross margin recovered to 30% in Q1 2026, reversing a compression that had run from 33% in the June 2024 quarter down to a trough of 26% in December 2025.

SG&A of $1.56 billion in Q1 2026 is running at the highest level in the eight-quarter window, as capacity investment and higher incentive compensation build ahead of peak engine installation activity in 2027 through 2029.

Operating income of $3.17 billion recovered 21% year-over-year, confirming revenue growth absorbed the cost expansion with margin to spare.

The tension the income statement surfaces is this: operating margins are recovering, but tariff costs are expected to increase to approximately $700 million in Q2 2026, and SG&A is at a record, which means the recovery is real but not yet confirmed as durable.

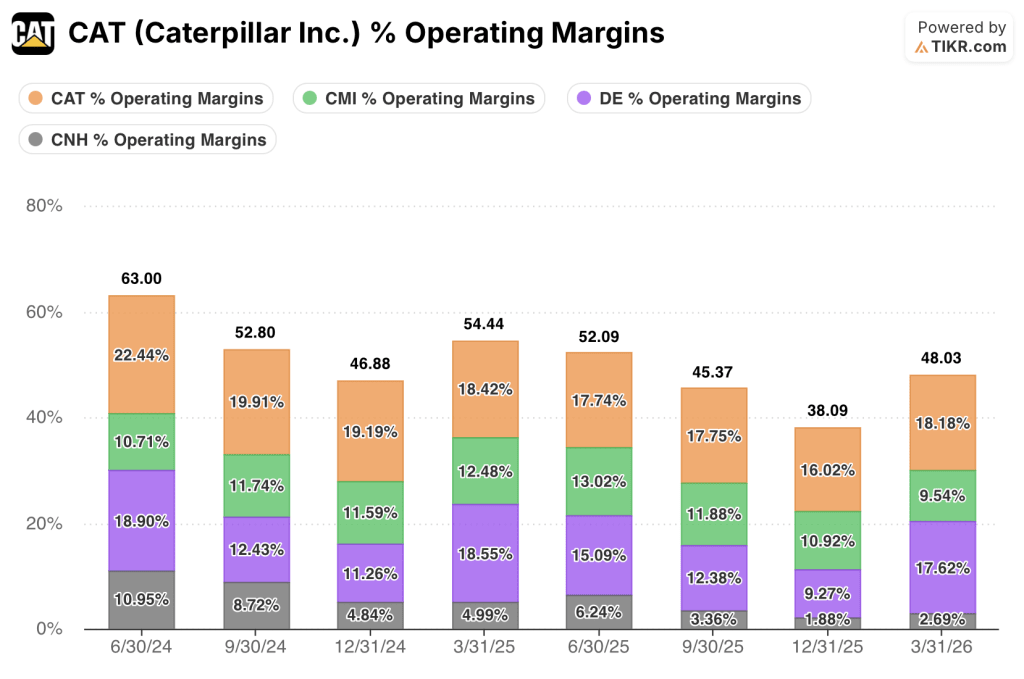

CAT Leads Peers on Operating Margins, but the Compression Gap Tells the Real Story

Caterpillar posted an 18% operating margin in Q1 2026, leading Deere (DE) at 18%, CNH Industrial (CNH) at 3%, and Cummins (CMI) at 10% across the same period.

The CAT and DE comparison is the one that matters most: both entered the eight-quarter window at similar margin levels, with Caterpillar at 22% and Deere at 19% in June 2024, but Caterpillar compressed harder through the cycle, bottoming at 16% in December 2025 versus Deere’s 9%.

Caterpillar’s sharper compression and sharper recovery suggest a business with more operating leverage in both directions, which is precisely the mechanism the income statement thesis depends on to reach the TIKR target.

CNH’s margin collapsed from 11% in June 2024 to 3% by March 2026, confirming that the tariff and demand cycle hit agriculture-heavy peers far harder than Caterpillar’s diversified Power and Energy mix allowed.

Cummins held the most stable margin band across the eight quarters, ranging from 10% to 13%, reflecting a more services-weighted revenue mix with less exposure to the equipment volume swings that drove Caterpillar’s compression and recovery.

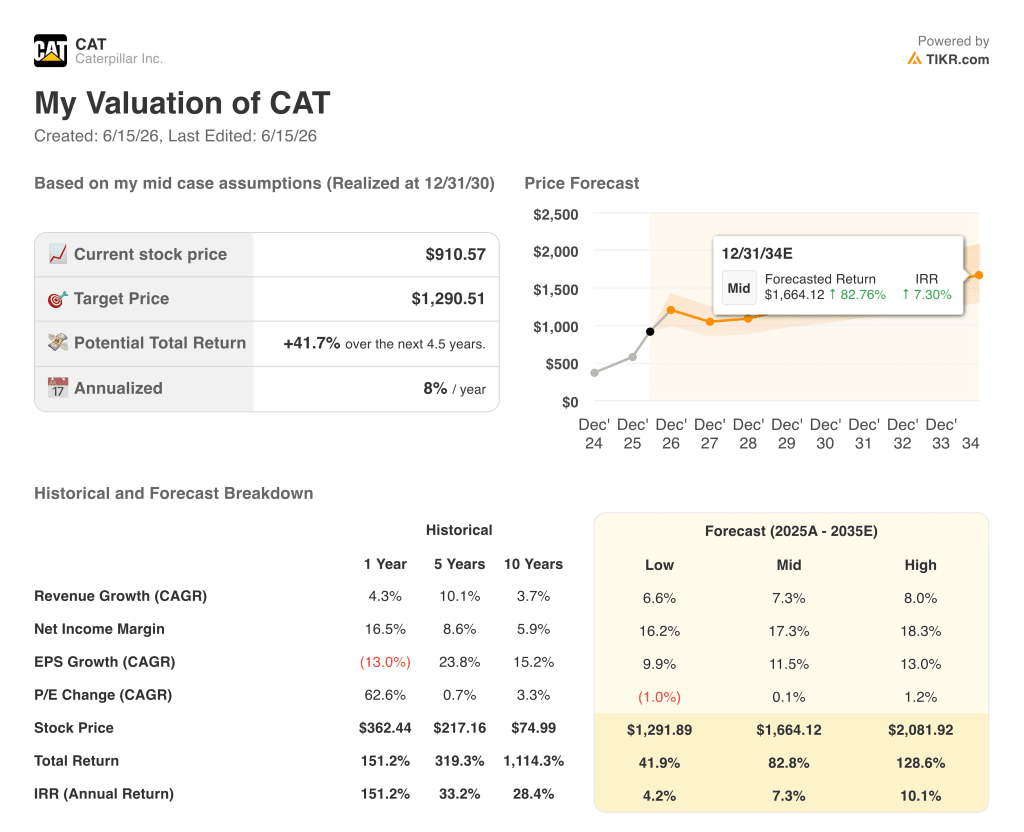

Is Caterpillar Stock Undervalued in 2026? TIKR’s $1,291 Model Makes the Case

TIKR’s model values Caterpillar at approximately $1,291 by December 2030, implying around 42% total return from the current price of $911, or roughly 8% per year.

That target is credible if gross margin continues its Q1 recovery trajectory and operating expenses stabilize as capacity investments mature after 2027, which is exactly the dynamic the income statement began to signal this quarter.

The risk the model has to navigate is a tariff environment the company itself calls fluid, with full-year 2026 tariff costs now estimated between $2.2 billion and $2.4 billion.

Should You Invest in Caterpillar Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Caterpillar Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Caterpillar Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CAT stock on TIKR for Free →