Key Stats for Airbnb Stock

- Current Price: $132.28 (June 12, 2026 close)

- Target Price (Mid): ~$303

- Street Target: ~$156

- Potential Total Return: ~129%

- Annualized IRR: ~20% / year

- Earnings Reaction: +0.73% (May 7, 2026)

- Max Drawdown (1-yr): 21.54% (November 20, 2025)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Airbnb (ABNB) keeps doing the things that move a stock, and the stock keeps not moving. Revenue grew 18% last quarter, management raised guidance, and in May, the company shipped its largest product release ever. Shares still closed at $132.28 on June 12, about 11% lower than five years ago and stuck mid-range between a 52-week low of $110.81 and a high of $147.25.

That is the tension. Airbnb stock 2026 is not a broken-business story. It is a market that has watched the company compound for three years and paid roughly the same price the whole time. Bulls see a platform entering new verticals from a net cash position and call the flat chart a coiled spring. Bears see slowing core growth and call it fair value. The question neither side can answer: what forces the re-rating?

The catalysts are already on the table. They just haven’t shown up in the numbers yet.

The Quarter That Should Have Mattered More

On May 7, Airbnb reported Q1 revenue up 18% to $2.7 billion, beating the high end of guidance. Gross booking value, the total dollar value booked on the platform, rose 19% to $29 billion. Free cash flow hit $1.7 billion in the quarter and $4.5 billion over the trailing twelve months, a 36% margin. The next day, the stock rose just 0.73%.

The shrug traces to the guidance. Management raised the full-year outlook but framed growth as accelerating only to “low to mid-teens” and held adjusted EBITDA margin at “at least 35%,” because it plans to keep reinvesting. CFO Ellie Mertz was blunt: “We are actively looking to reinvest to drive growth,” citing marketing, international expansion, and AI. Airbnb is choosing the long game over a clean margin beat, and the market hasn’t decided whether to reward it.

The engine looks healthier than the price suggests. Nights booked on the app grew 22% and now make up 63% of total nights, up from 58% a year ago. First-time bookers grew 10%, the fastest since 2022. Reserve Now, Pay Later, which lets guests book now and pay closer to the stay, drove about 20% of global GBV.

See historical and forward estimates for Airbnb stock (It’s free!) >>>

The Real Catalyst Shipped on May 20

Two weeks after earnings, Brian Chesky announced 220 new features in the 2026 Summer Release, the most ambitious update in company history. Airbnb added boutique hotels in 20 cities and bookable services across the whole trip: airport pickups, luggage storage, grocery delivery, and car rentals. The stock barely registered it.

That muted reaction is why the release matters. On the call, Chesky reached for a comparison: “I do see Amazon as a pretty good inspiration for us,” Airbnb Co-Founder and CEO Brian Chesky told investors, describing a path from one product into adjacent categories that get cheaper to add each time, because “once you solve one service, the next service is only 20% different.” If that holds, Airbnb is turning a booking app into a travel ecosystem, and the market is paying for the app.

Hotels are the clearest near-term test. Mertz said they are still a single-digit share of nights but growing at more than double the overall rate, and flagged why Airbnb cares: “over 55% of people who book a hotel on the platform come back to book a home.” Hotels are a top-of-funnel machine for the core homes business.

What the Market Is Worried About

The bear case is real. Core Nights and Seats Booked grew 9% in Q1, decelerating from prior years, and management guided Q2 slightly lower on an estimated 100 basis point headwind from the Middle East conflict. Director and co-founder Joseph Gebbia also sold about $35.9 million of stock on June 1 under a pre-arranged plan, the kind of insider selling skeptics cite even when scheduled in advance.

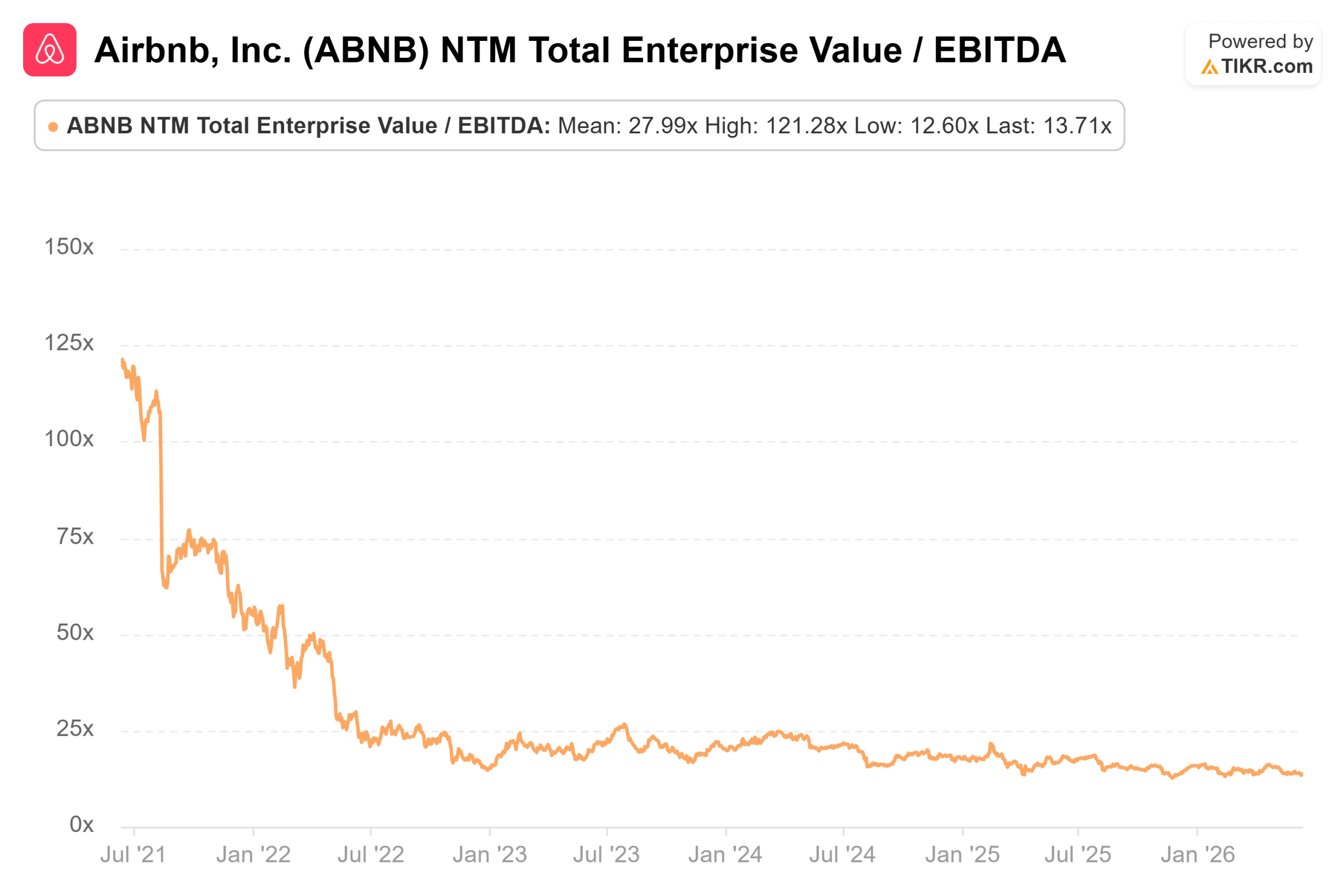

On valuation multiples, Airbnb is not screening cheaply. Its NTM EV/EBITDA of 13.71x, based on next-twelve-month estimates, sits above Booking Holdings at 11.74x and Trip.com at 7.71x, though below asset-heavy operators Marriott at 20.48x and Hilton at 22.15x. The honest read: Airbnb is priced as a capital-light platform expected to grow faster than the hotel chains and convert more revenue to cash than the online agencies, supported by its 36% free cash flow margin and net cash. Whether that premium holds depends on one thing: can the new verticals re-accelerate growth? The Street is waiting, with 19 Buys, 4 Outperforms, 18 Holds, no Underperforms, and 2 Sells, and a mean target of ~$156, about 18% above the current price.

See how Airbnb performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Target Price (Mid): ~$303

- Potential Total Return: ~129%

- Annualized IRR: ~20% / year

See analysts’ growth forecasts and price targets for Airbnb stock (It’s free!) >>>

- Revenue drivers: mid-to-high single-digit core nights growth as expansion markets (Brazil, Japan, India) compound, plus rising monetization from new services, fee simplification, and insurance lifting the take rate

- Margin driver: AI-led operating leverage, with ~60% of code now AI-authored and cost per booking down about 10% year-over-year

- Primary risk: core nights growth keeps slowing, and new verticals scale too slowly to offset it

- Upside: the ecosystem strategy works, take rate climbs, and shares re-rate toward ~$303.

- Downside: growth settles into a steady mid-teens and the stock stays range-bound, exactly as it has for three years.

Conclusion

Watch the take rate, and watch it on August 6, when Airbnb reports Q2. Management has now told investors twice that monetization, not just nights, drives the raised second-half guidance. If the Q2 implied take rate ticks up and management quantifies early traction from hotels and services, the ecosystem thesis stops being a slide and becomes a number, which is what a flat stock needs to break higher. If the take rate is flat and core nights slip below the high single digits, the bears get their proof that Airbnb is a mature platform, fairly priced. The take rate line in the Q2 shareholder letter is the cleanest tell on whether the next five years rhyme with the last five.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Airbnb?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Airbnb, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Airbnb alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!