Key Stats for Pfizer Inc. Stock

- 52-Week Range: $23.11 – $28.75

- Current Price: $26.04

- Street Mean Target: $29.19

- Street High Target: $36.00

- Dividend Yield: ~6.6%

Pfizer’s (PFE) story since 2022 has been defined by one uncomfortable fact: the company built a revenue base on COVID vaccines and treatments that would never last. At their peak, Comirnaty and Paxlovid generated tens of billions of dollars annually.

As those tailwinds faded, Pfizer’s revenue fell sharply, the stock followed, and the narrative shifted from pandemic hero to turnaround candidate. What gets lost in that framing is that the underlying business, oncology, cardiology, vaccines, and rare disease, has been quietly growing throughout, and the dividend has never stopped increasing.

That tension between the headline story and the underlying reality is what makes Pfizer interesting at $26.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Q1 Actually Showed

Total revenue came in at $14.5 billion in Q1 2026, up 5% year over year. Strip out Comirnaty and Paxlovid entirely, and the rest of the business grew 7% operationally.

The launched and acquired products category, which includes recent additions from the Seagen acquisition and other pipeline investments, grew 22% operationally, which is the number management is most focused on and investors should be watching most closely.

A few individual products stood out. Padcev, the bladder cancer treatment acquired through Seagen, grew 39% operationally as it gained share in first-line treatment. Nurtec, the migraine therapy, grew 41% operationally on strong demand. Lorbrena, used to treat ALK-positive lung cancer, grew by 32%.

These are not small, speculative pipeline assets, they are commercially launched products with growing physician adoption and expanding indications.

The FCF chart captures the COVID distortion better than any narrative can. Free cash flow peaked near $30 billion in 2021, collapsed to under $5 billion in 2023 as COVID revenue normalized and Pfizer absorbed the costs of the Seagen acquisition, and has since recovered to around $9 billion.

Those $9 billion fund the dividend, the R&D pipeline, and balance sheet deleveraging, and they have been enough to do all three simultaneously.

See historical and forward estimates for Pfizer stock (It’s free!) >>>

The Dividend Is the Anchor

For many investors, Pfizer is primarily an income holding, and the dividend case is straightforward. At $26, the stock yields roughly 6.6% annually, which is among the highest yields available in large-cap pharmaceuticals. Pfizer paid $2.4 billion in dividends in Q1 2026 alone, and management has been explicit that maintaining and growing the dividend is a core capital allocation priority.

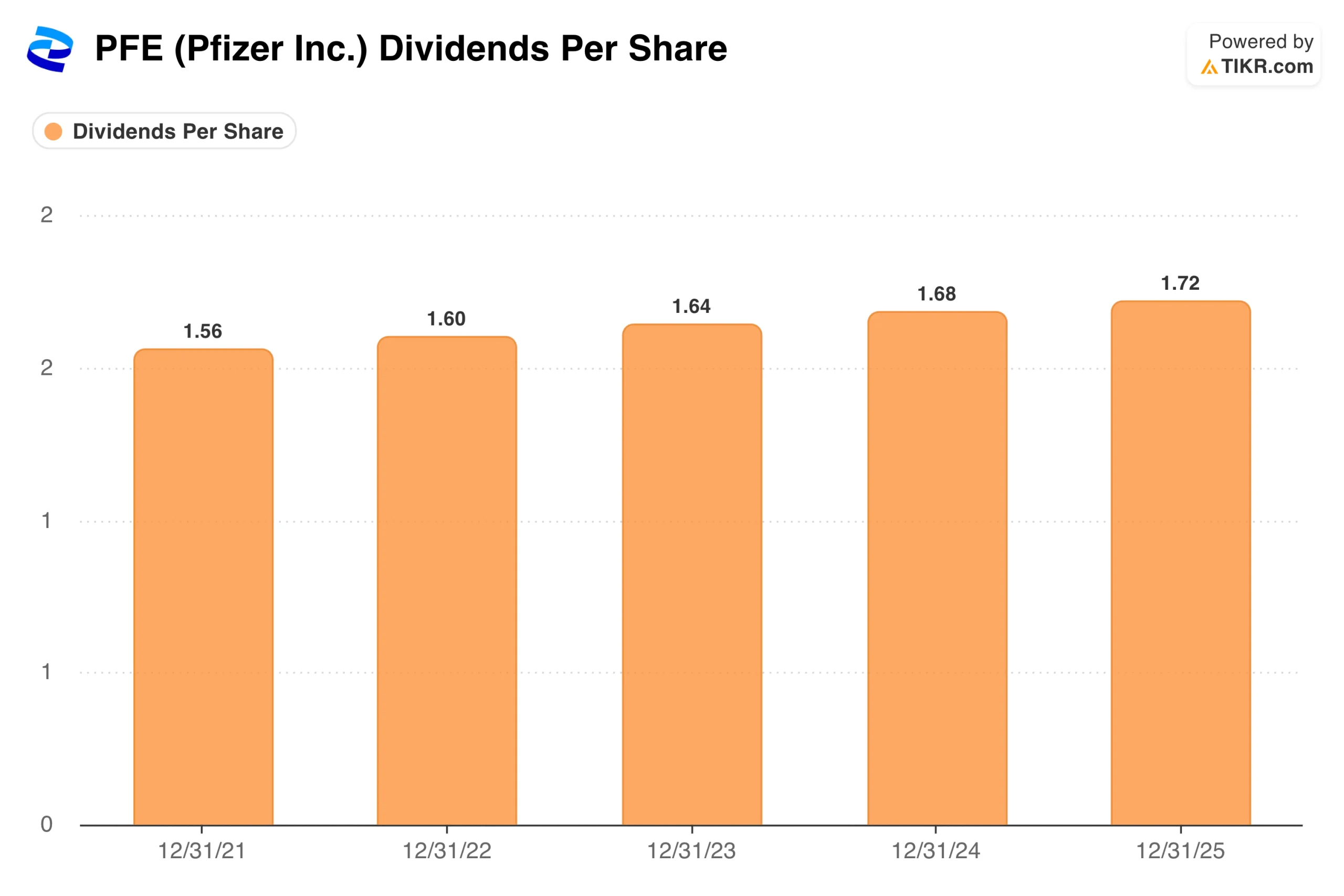

That chart tells a story no earnings slide can replicate. Through the COVID boom, the revenue collapse, a massive acquisition, and a multiyear restructuring program, the dividend per share has increased every single year.

From $1.56 in 2021 to $1.72 in 2025, the increases have been modest, but consistency matters more than size when income investors are evaluating whether a yield is sustainable. With $9 billion in annual free cash flow against roughly $9.7 billion in total annual dividends, coverage is tight but manageable, and management has shown no inclination to cut dividends.

See how Pfizer performs against its peers in TIKR (It’s free!) >>>

The Pipeline Bet: Oncology and Obesity

The income thesis gets investors in the door, but the pipeline is what determines whether Pfizer grows from here or simply maintains. CEO Albert Bourla has been particularly direct about two areas: oncology and obesity.

On the Q1 call, he noted that Pfizer intends to advance 10 Phase 3 obesity studies in 2026, building on the Metsera acquisition, which brought next-generation GLP-1 receptor agonist candidates into the portfolio. The first obesity approval is targeted for 2028, which puts Pfizer several years behind Eli Lilly and Novo Nordisk but still early enough in the market’s development to matter.

The oncology story is more immediate. The Seagen integration has strengthened Pfizer’s position in antibody-drug conjugates, a class of cancer treatments that deliver chemotherapy directly to tumor cells, and multiple Seagen products are now growing at double-digit rates.

Pfizer also secured a patent settlement for Vyndamax that extends exclusivity to mid-2031, adding meaningful revenue visibility not included in prior estimates.

What the Street Says About Pfizer’s Value

With the stock at $26 and a mean analyst target of around $29, the implied upside is modest, roughly 12% before accounting for the dividend. The distribution of views is telling, though: 27 analysts cover the stock, with 9 buys, 11 outperforms and holds combined at 16, and just 1 sell.

That’s not a stock the Street is negative on, it’s a stock the Street is cautious about, waiting for cleaner evidence that the non-COVID business can sustain its growth trajectory through the patent cliff years of 2026 to 2028.

The high target of $36 reflects the bull case if oncology and obesity deliver on their promise and the base business holds up better than feared. The low target of $24 reflects the bear case if patent expirations bite harder than expected and the obesity pipeline disappoints.

At $26, the stock is trading near the bottom of the analyst range, suggesting the market is currently pricing in a more pessimistic scenario.

Should You Invest in Pfizer Inc.

Pfizer is not a growth stock and shouldn’t be evaluated like one. The right frame is a high-yield income holding with a speculative overlay, the 6.6% dividend is real and well supported by cash flow, and the pipeline in oncology and obesity gives investors optionality on outcomes that aren’t yet priced in.

The patent cliff risk is real, and the next two years will be bumpy, but management has navigated the COVID hangover without cutting the dividend or abandoning the R&D program, underscoring operational discipline.

For income investors comfortable with the uncertainty, the setup at $26 is more interesting than the stock’s recent history suggests.

See analysts’ growth forecasts and price targets for Pfizer stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!