Key Stats for PayPal Stock

- Current Price: $44.16

- Target Price (Mid): ~$70

- Street Target: $52.53

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

- Earnings Reaction: -0.47% (May 5, 2026)

- Max Drawdown: -50.04% (February 12, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

PayPal Holdings (PYPL) has given investors two years of reasons to doubt it. The stock peaked at $79.50 last July, bottomed at $38.46 in February 2026, and sits at $44.16 today, a 44% decline from its high. The company’s investor relations materials tell the story of a business that is profitable and cash-generative but unable to convert that strength into the kind of branded checkout growth investors expected when it was worth three times its current price.

That context makes May 5 worth paying attention to. On that date, new CEO Enrique Lores held his first earnings call and delivered the most specific turnaround plan PayPal has put forward in years. Wall Street’s response was a -0.47% stock move. Thirty-two of 45 analysts still rate the stock a Hold. The market is not skeptical so much as it is waiting. The TIKR model argues the wait may be worth it.

Two Years of Damage, and a New Starting Point

The 50.04% max drawdown PayPal hit on February 12, 2026, reflected compounding problems: slowing branded checkout growth, take rate compression, and a CEO departure after barely a year in the role. When Lores was appointed President and CEO effective March 1, replacing Alex Chriss, the board’s language was direct. The pace of execution had not met expectations.

Lores is not a payments insider. He spent more than six years running HP through a complex technology and services transformation, and the board appears to have prioritized operational discipline over domain familiarity.

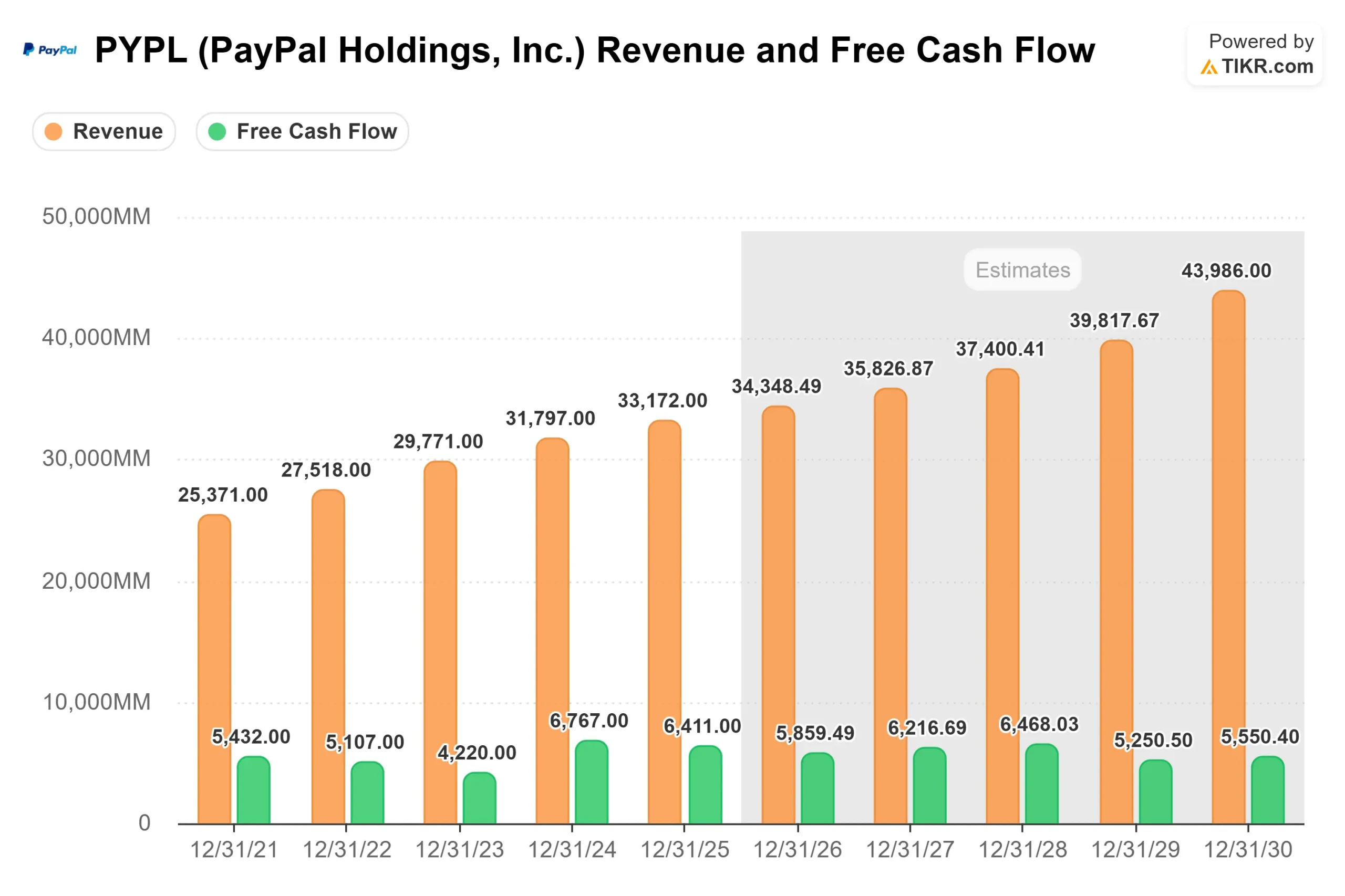

Q1 2026 results were solid on the surface. Revenue came in at $8.353 billion, up 7% year-over-year and 3.71% ahead of consensus. Non-GAAP EPS of $1.34 beat estimates by 5.59%. Total payment volume, the total dollar value of all transactions processed on PayPal’s platform, reached $464 billion, up 11% at spot rates. None of it moved the stock, because what investors are actually pricing is what happens over the next two years, not last quarter.

See historical and forward estimates for PayPal stock (It’s free!) >>>

What Lores Actually Said

Lores named five specific problems on the call: a fragmented technology platform, too much investment in merchants at the expense of consumers, organizational complexity that slowed decisions, a bloated cost structure, and a pattern of launching products without investing enough to drive real adoption.

That last point came with an unusually direct example. Lores described a PayPal NFC (near-field communication, the technology behind tap-to-pay) launch in Germany that got a strong initial reception before PayPal failed to invest enough in local consumer awareness. “We have moved to launch the next version before really maximizing the value that we got from what we were launching,” he said.

The response is a three-business structure announced on April 29: Checkout Solutions and PayPal, Consumer Financial Services and Venmo, and Payment Services and Crypto (which includes Braintree, PayPal’s unbranded payment processing platform). Each line has a single accountable leader. A new Chief AI Transformation and Simplification Officer, Anshu Bhardwaj, reports directly to Lores and is tasked with redesigning key processes before deploying AI, rather than running isolated pilots. The financial commitment behind it all is a $1.5 billion gross run-rate cost savings program over the next two to three years, with most savings earmarked for reinvestment in growth rather than near-term earnings.

What the Business Is Doing Right Now

Branded checkout grew 2% on a currency-neutral basis in Q1, the headline number driving most of the skepticism. The rest of the business looks different. Venmo TPV grew 14% year-over-year, its sixth consecutive quarter of double-digit growth. Buy now, pay later volume, which lets shoppers split purchases into installments, grew 23%. Pay with Venmo grew 34%. Braintree and Enterprise Payments, PayPal’s unbranded processing segment for larger merchants, accelerated to mid-teens volume growth after sitting at 7% in the back half of 2025.

On the capital allocation front, PayPal completed $1.5 billion in share repurchases in Q1 alone. Management’s adjusted free cash flow for the trailing twelve months was approximately $6.8 billion, as stated by CFO Jamie Miller on the earnings call, with full-year 2026 guidance of at least $6 billion.

Two pieces of recent news are worth noting. On May 20, PayPal expanded its PYUSD stablecoin (PayPal’s dollar-pegged digital currency) to 70 markets globally. And on May 12, PayPal reached a DOJ settlement over a 2020 program for minority-owned businesses, agreeing to waive approximately $30 million in processing fees for eligible small businesses, with no admission of wrongdoing and no separate fine. The stock did not react to either.

See how PayPal performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $44.16

- Target Price (Mid): ~$70

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for PayPal stock (It’s free!) >>>

The TIKR model’s mid-case uses a revenue CAGR of around 5% and a net income margin of around 13%, arriving at a target price of $69.72 by December 31, 2030. The two primary growth drivers in the model are Venmo monetization (converting Venmo users into paying customers through debit cards, BNPL, and Pay with Venmo) and continued PSP volume expansion via Braintree and Enterprise Payments, where mid-teens growth is already visible. The margin driver is the $1.5 billion cost savings program. Even partial realization would generate meaningful operating leverage.

The upside path requires branded checkout to recover to mid-single-digit currency-neutral growth and cost savings to arrive near the top of management’s guidance. The downside is that branded checkout deterioration is structural, Braintree takes rates continue compressing as enterprise volume scales, and savings are consumed entirely by reinvestment with no improvement in earnings. In that scenario, the stock likely stays range-bound, and the ~10% annualized return does not materialize.

At 6.15x NTM EV/EBITDA and 8.13x NTM P/E, PayPal is priced for continued disappointment. The mid-case does not require a dramatic recovery. It requires around 5% annual revenue growth and margins that normalize modestly as transformation spending rolls off. Whether Lores earns the time to get there is the only open question.

Conclusion

Q2 2026 results, expected in late July, are the first real test of the Lores thesis. Management guided for an approximately 9% non-GAAP EPS decline year-over-year, which the market already knows. What investors do not know is whether branded checkout holds at 2% or slips further, given the softening travel vertical and European weakness management flagged as quarter-to-date trends. That is the number to watch: branded checkout TPV growth at 2% or better, with stable Venmo and PSP momentum, keeps the mid-case model intact. A further deceleration raises harder questions about whether the problem is executional or structural. Late July is when the answer arrives.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in PayPal?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PayPal, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PayPal alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!