Palantir Technologies (NYSE: PLTR) has become one of the most polarizing names in tech. Known for its government contracts and expanding commercial business, Palantir stock is up 437% this year, and has likely made many investors rich. But with the stock’s valuation stretched and AI competition rising, analysts are divided on what comes next.

This article explores where Wall Street analysts think Palantir could go by 2027. We’ve compiled consensus targets, valuation assumptions, and recent price action to get a sense of the stock’s possible trajectory. These figures reflect current analyst models and are not TIKR’s own predictions.

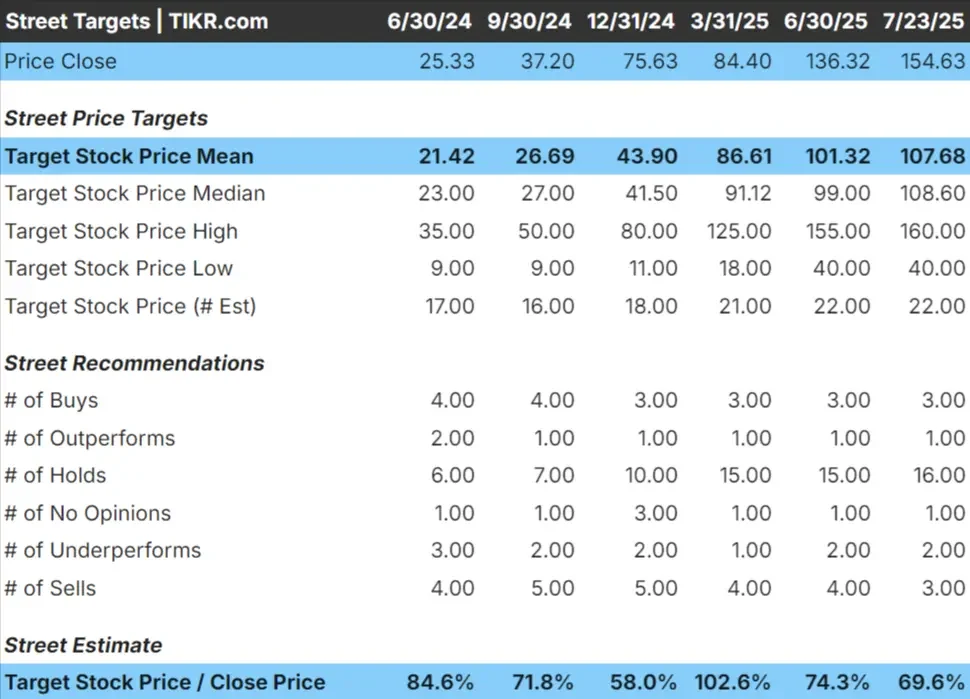

Analyst Price Targets Suggest the Stock Is Well Overvalued

Palantir’s stock has surged to over $150 per share as of July 2025, but the 18-month average price target is just $108, implying more than 25% downside from current levels. However, that is pretty consistent with what analysts have seen for the past year, when analysts thought the stock was woefully overvalued in late 2024 when it was trading at $37/share.

Forecasts now range from a high of $160 to a low of $40, highlighting the wide gulf between bulls and bears. Still, it seems as though all of the 22 analysts covering Palantir feel as though the current price already bakes in too much optimism as reflected in their share price targets.

See analysts’ growth forecasts and price targets for Palantir (It’s free!) >>>

Palantir: Growth Outlook and Valuation Concerns

Palantir’s revenue is projected to grow 32.1% annually through 2027, with operating margins forecasted to rise significantly to 44.6%. That combination of strong top-line growth and expanding profitability supports a pretty strong valuation, but current prices already reflect heavy optimism.

As of July 2025, Palantir trades at 250x next-twelve-months expected earnings, which is pretty significant for a business expected to grow earnings at a little under 40% annually over the next several years. In our Guided Valuation Model, we used a 91x forward P/E ratio (which is already strong given analysts expect ~40% annual EPS growth), which gives us a target price of $116 per share by the end of 2027. That implies a 25.1% downside from today’s stock price of $155/share, which would be –11.1% on an annualized basis.

To justify the current valuation, the company would likely need to exceed both revenue and margin forecasts, or prove that it can dominate key categories like AI infrastructure and government data platforms at scale.

Value stocks like Palantir in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Palantir’s expanding AI platform, strong government ties, and commercial momentum have helped drive the stock up sharply. Bulls believe Palantir is building the backbone of enterprise and defense AI. If the company maintains its growth trajectory and becomes a dominant platform, it could justify a premium valuation.

Palantir also has a strong balance sheet and no debt, which gives it room to keep investing aggressively in product development and customer expansion.

Bear Case: Overvaluation and Lofty Expectations

Despite the growth story, the stock looks expensive. At $155 per share, Palantir trades at 250 times projected next-12-month earnings. The guided valuation model suggests the stock is 25% overvalued based on current assumptions.

The AI market is getting crowded, with heavyweights like Microsoft and Google competing for enterprise customers. Palantir’s valuation already assumes dominant positioning and continued margin expansion. If revenue growth slows or customers delay AI adoption, the stock could re-rate lower, which leaves little room for execution risk.

Outlook for 2027: What Could Palantir Be Worth?

Under the current forecast, Palantir’s stock could fall to $116/share by the end of 2027. That would represent a 25% drop from today’s price and a negative annual return of 11.1%.

That forecast assumes Palantir delivers strong revenue growth and hits 44.6% operating margins. Even with strong performance, the valuation is stretched.

For long-term upside, Palantir would need to outperform expectations or prove it can build a must-have AI platform that scales across industries. Otherwise, investors may end up paying too much for a good story.

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.