Netflix Inc. (NASDAQ: NFLX) has become one of the market’s biggest comeback stories. After a sharp rebound, the stock now trades near $1,188/share, up about 73% in the past year. Stronger streaming demand, a growing ad-supported tier, and a crackdown on password sharing have fueled the surge. But with the valuation looking stretched and competition still intense, analysts appear split on what comes next.

This article explores where Wall Street analysts think Netflix could trade by 2027. We have pulled together consensus targets, growth forecasts, and valuation models to get a sense of the stock’s possible trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

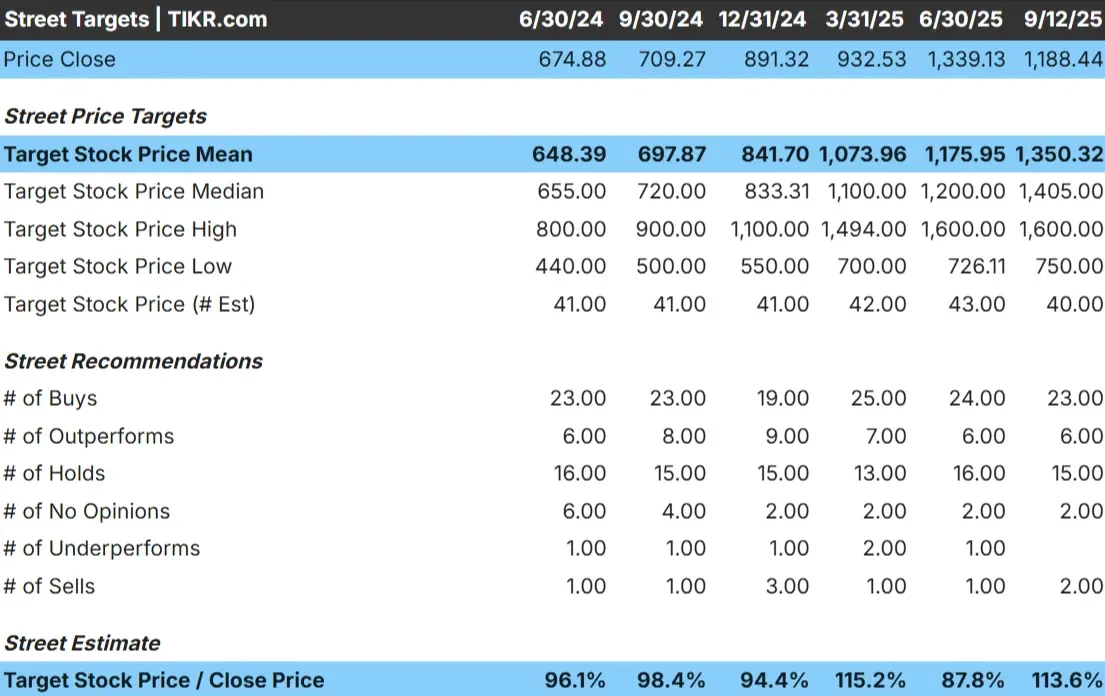

Netflix trades at about $1,188/share today. The average analyst price target is $1,350/share, which points to around 13% upside. Forecasts show a wide spread and reflect divided sentiment:

- High estimate: ~$1,600/share

- Low estimate: ~$750/share

- Median target: ~$1,405/share

- Ratings: mix of Buys, Holds, and a few Sells

It looks like analysts see some room for gains, but the broad range of targets suggests that conviction is weak. The takeaway is that expectations are already high, and Netflix may need to deliver stronger-than-expected results to break meaningfully above current levels.

Investors should weigh whether the potential 13% upside justifies the risks of owning a premium-priced stock.

See analysts’ growth forecasts and price targets for Netflix (It’s free!) >>>

Netflix: Growth Outlook and Valuation

The company’s fundamentals still appear solid, but not extreme:

- Revenue is projected to grow ~13% annually through 2027

- Operating margins may expand from ~30% today to ~33%

- Shares trade at ~40x forward earnings, close to the 5-year average

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 34x forward P/E suggests ~$1,472/share by 2027

- That implies ~24% upside, or about 10% annualized returns

These numbers suggest Netflix can keep compounding steadily, but not at the breakneck pace of its earlier years. The valuation looks fair relative to growth, which means the stock is not a screaming bargain but not drastically overpriced either.

Investors may see Netflix as a dependable long-term holding, though meaningful upside likely depends on stronger margin gains or faster international growth.

Value stocks like Netflix in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Netflix has managed to keep growing even as streaming has matured. The ad-supported tier is seeing strong adoption, creating a new revenue stream that also helps expand margins. International expansion remains a big driver, with emerging markets adding subscribers at a steady pace.

On top of this, content efficiency appears to be improving. Netflix still spends heavily on original content, but its ability to generate strong engagement at scale is boosting returns on that investment. Combined with its global brand and distribution reach, these factors help explain why bulls believe Netflix can maintain its leadership position in streaming.

These trends provide confidence that Netflix can keep margins healthy and justify its valuation premium, even in a crowded competitive landscape.

Bear Case: Valuation and Competition

Despite the positives, Netflix’s valuation looks demanding compared to some analyst targets. Competition remains fierce, with Disney, Amazon, and YouTube all investing heavily in content and distribution. If rivals capture market share or slow Netflix’s subscriber momentum, growth could come under pressure.

There is also the risk of slowing additions in mature markets like the U.S. and Europe, where penetration is already high. Rising content costs may also weigh on profitability if they outpace revenue growth. Taken together, these risks suggest Netflix has little room for error.

The bear case is that Netflix’s valuation assumes near-perfect execution. If revenue growth slows or margins fail to expand as projected, the stock could face a significant re-rating.

Outlook for 2027: What Could Netflix Be Worth?

Based on current forecasts, Netflix could trade near $1,472/share by 2027. That would represent about a 24% gain from today’s level, or roughly 10% annualized returns. The outcome assumes consistent double-digit revenue growth and margin expansion to the low-30s.

While this would represent healthy performance, the scenario already builds in a fair amount of optimism. To deliver stronger upside, Netflix would need to outperform on subscriber growth, ad-tier monetization, or international expansion. Without that, gains may be steady but unspectacular.

Netflix looks like a solid long-term compounder, but the path to outsized returns depends on the company beating current expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.