Key Stats for MercadoLibre Stock

- 52-Week Range: $1,495 – $2,549

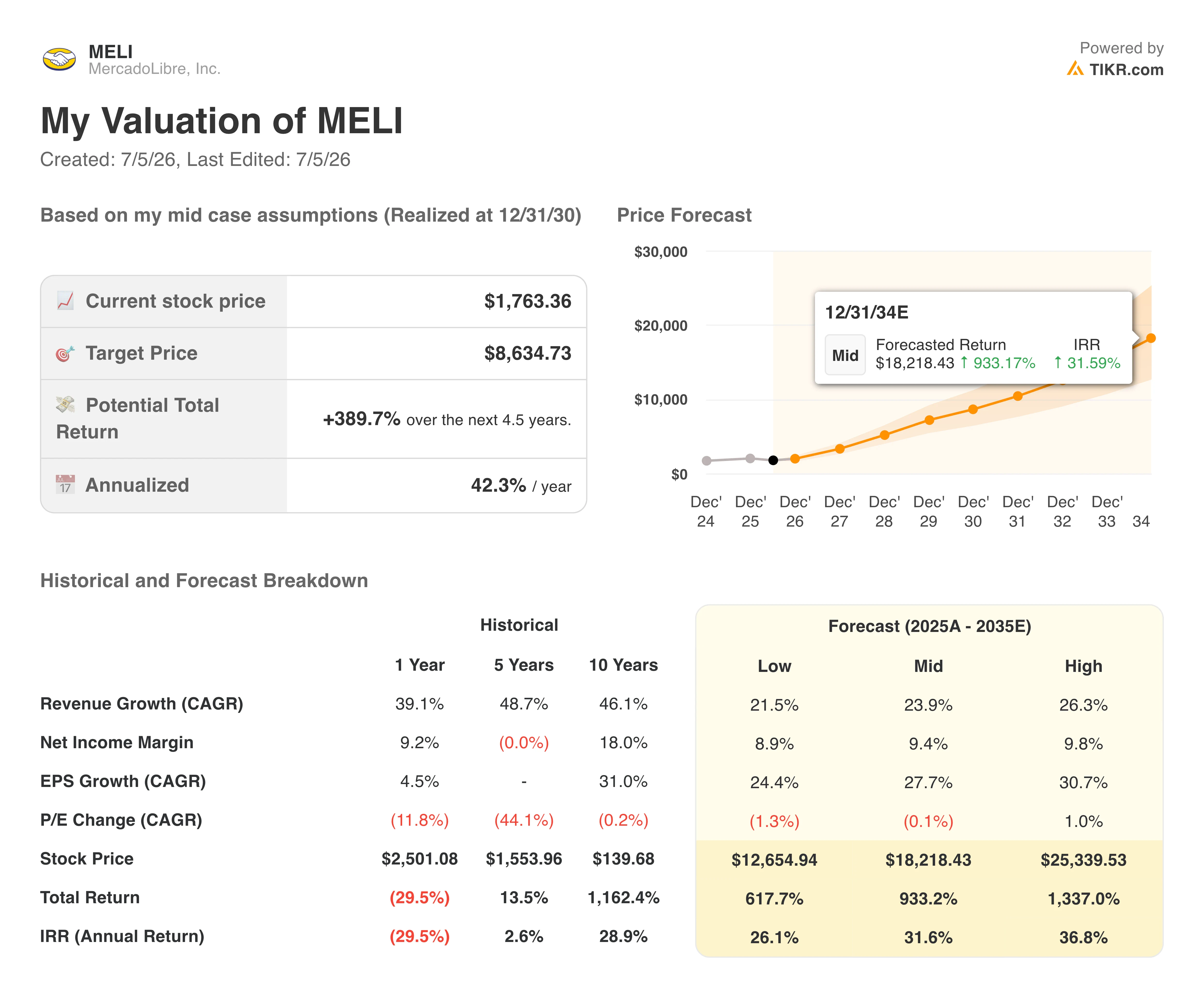

- Current Price: $1,763

- Street Target Price: around $2,216

- TIKR Model Target (Mid Case, 2030): around $8,635

- Potential Total Return: around 390% over the next 4.5 years

- Annualized Return (IRR): around 42% per year

- Market Cap: $89.4 billion

- Max Drawdown: 33% from 52-week highs

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

A Steep Drawdown Meets the Fastest Growth in Four Years

MercadoLibre’s (MELI) stock has spent most of 2026 sliding lower, and the chart below shows how uneven that decline has been.

The drawdown deepened through the first quarter, eased briefly into April, then fell off a cliff in mid-May, touching a max drawdown of around 33% before recovering slightly to roughly 23% below its high today. That sharp drop lines up almost exactly with the company’s first quarter earnings release in early May.

What makes the market’s reaction notable is the quarter itself. Net revenue and financial income grew 49% year over year to $8.85 billion, the fastest pace since 2022, and came in well ahead of analyst expectations.

Commerce revenue rose 47%, and Fintech revenue rose 51%, with Brazil alone accelerating to 55% growth as a lower free shipping threshold pulled in new buyers and pushed item volume higher. Investors did not sell the top line.

They sold the direction management signaled it would keep taking margin pressure, and the earnings-per-share miss that came with it.

See historical and forward estimates for MercadoLibre stock (It’s free!) >>>

Why Operating Margins Are Compressing on Purpose

The chart below shows the trend behind that concern. Operating margin expanded from 6% in 2021 to a peak near 15% in 2023, then began sliding, falling to around 11% by the end of 2025.

That decline continued into the first quarter, with operating income falling 20% year over year to $611 million and margin compressing to 6.9% from 7.5% a year earlier. Earnings per share came in at $8.23, missing consensus estimates of around $9 by a wide margin.

Management has been direct about why. Free shipping expansion in Brazil, an aggressive credit card rollout across Brazil, Mexico, and Argentina, and continued fulfillment investment are compressing margins by design today, aimed at widening MercadoLibre’s competitive position across Latin American commerce and fintech.

Unit shipping costs are already falling faster than expected, credit card delinquency is improving even as the loan book grows 87% year over year, and management has said this margin dial is unlikely to shift materially in the near term.

The underlying bet is that today’s scale converts into meaningfully higher margins later, the same pattern that played out after the original free shipping investment a decade ago.

See how MercadoLibre performs against its peers in TIKR (It’s free!) >>>

What the Valuation Model Says About the Path Back

TIKR’s valuation model targets around $8,630 for MercadoLibre by the end of 2030 in the mid case, implying a potential total return of around 390% and an annualized return of near 42%.

That outcome leans mainly on continued revenue compounding rather than multiple expansion, with the model assuming annual growth in the low- to mid-20 % range and a net income margin expanding toward around 9% as the credit card and advertising businesses mature and dilute today’s investment costs.

The scenario range skews toward the upside. The low case still implies a return above 600% through 2034, while the high case tops 1,300%, reflecting how much of today’s valuation gap is tied to the pace of margin recovery rather than whether growth continues at all.

Wall Street’s average price target of around $2,215 is far more conservative, implying roughly 26% upside from current levels and reflecting a shorter, less optimistic view of how quickly margins normalize from here.

Should You Invest in MercadoLibre?

MercadoLibre remains a clear example of a company trading near-term profitability for long-term scale rather than losing control of its cost structure.

The current drawdown reflects real earnings pressure, not a broken business, and management has consistently explained the margin trade-off over several quarters.

Investors comfortable holding through continued volatility across Latin American markets may find today’s price an attractive entry into a multi-decade growth story. Those who prioritize near-term earnings stability may want to wait for clearer signs that margins have bottomed.

See analysts’ growth forecasts and price targets for MercadoLibre stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!