Key Stats for Cloudflare Stock

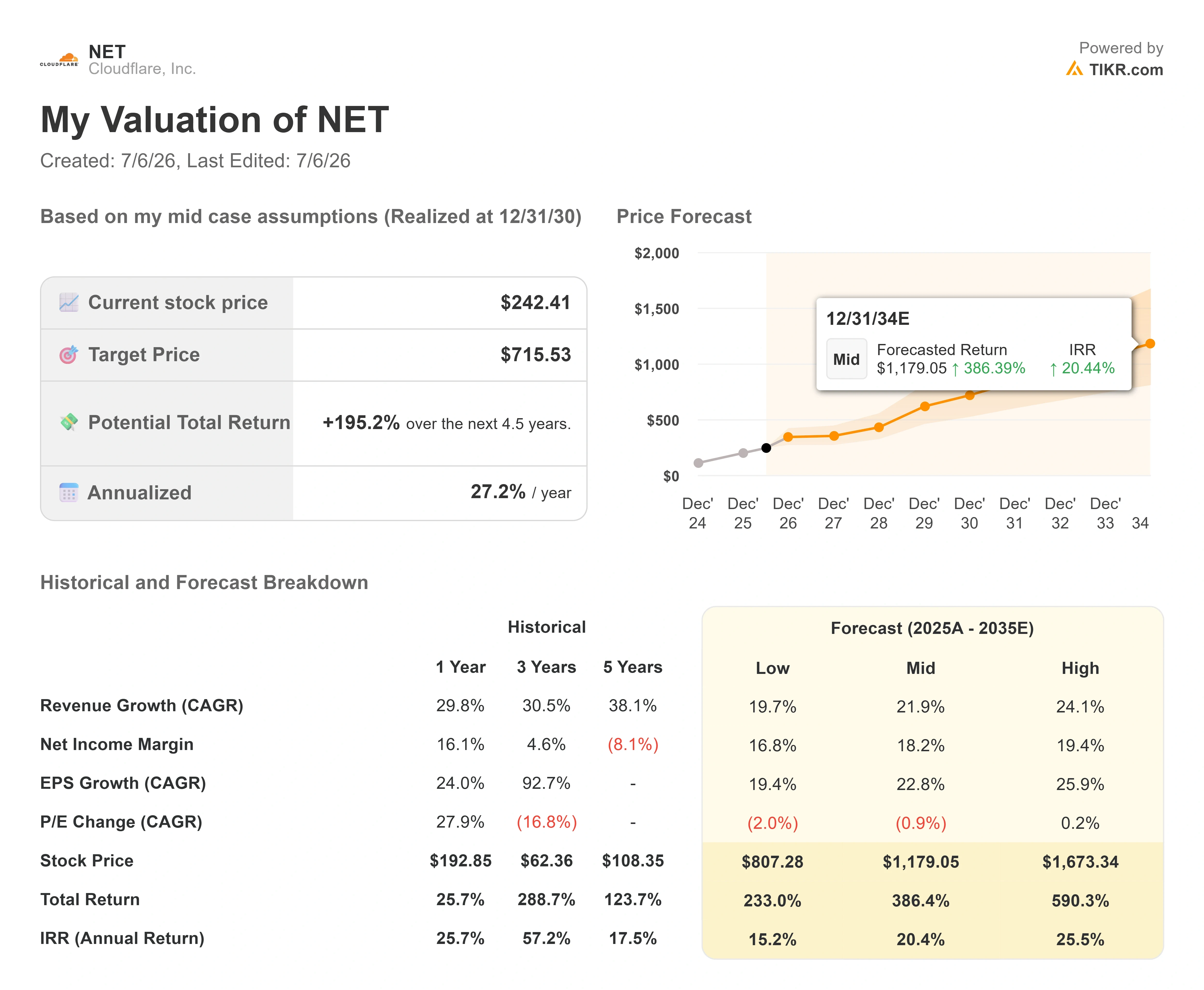

- Current Price: $241.00

- Target Price (Mid): ~$716

- Street Target: ~$244

- Potential Total Return: ~195%

- Annualized IRR: ~27% / year

- Earnings Reaction: -23.62% (May 7, 2026)

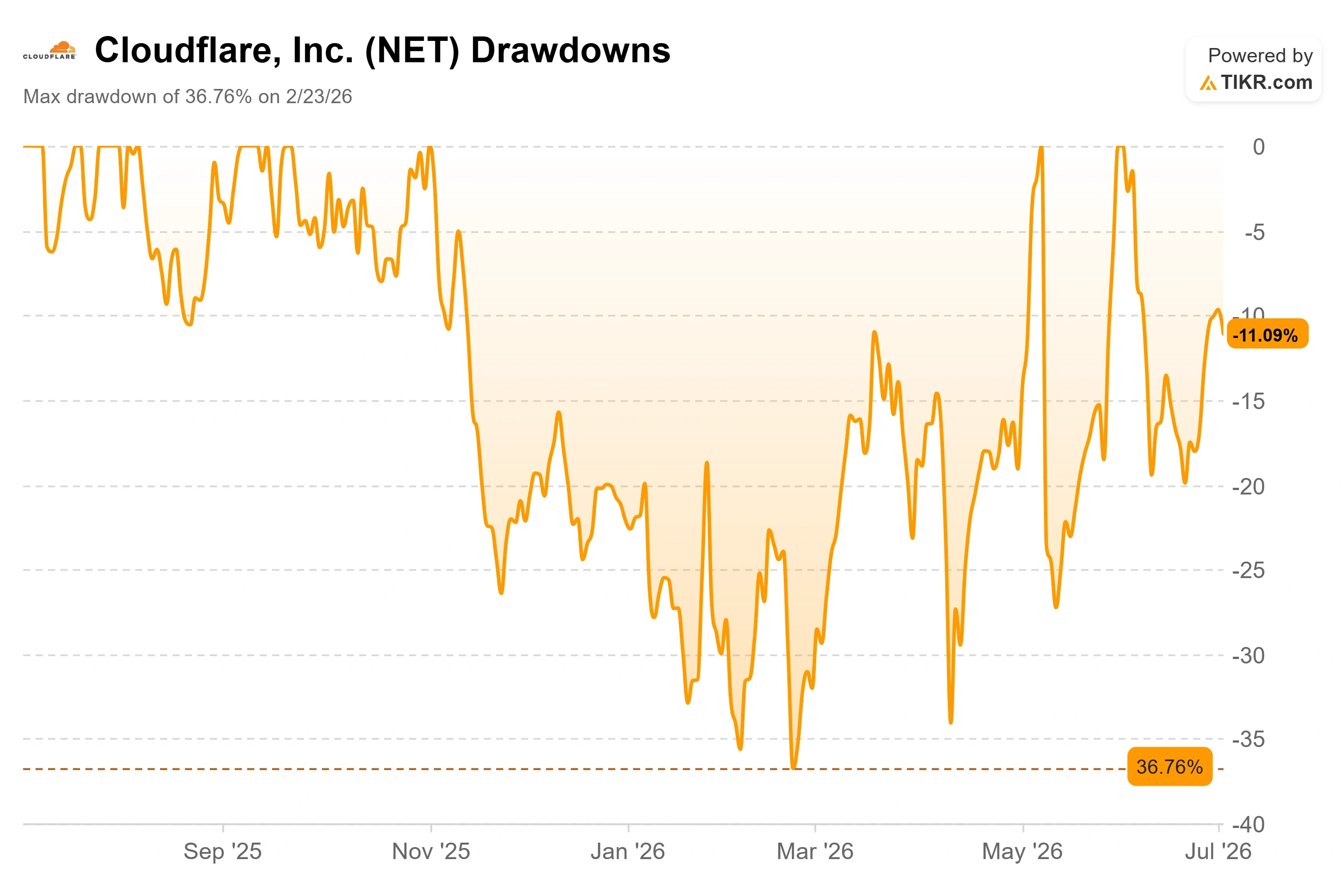

- Max Drawdown: 36.76% (February 23, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Cloudflare, Inc. (NET) spent its June 9 Investor Day telling investors that the business model of the internet was about to change, and that it would be the company writing the new rules. Three weeks later, on July 1, it put the first real product behind that claim. The gap between a compelling story and a working product is where most high-multiple software theses live or die, and Cloudflare just started closing that gap in public.

The launch matters because of where the stock sits. NET trades at $241.00, roughly 13% below its 52-week high of $276.82, having already round-tripped a 36.76% drawdown that bottomed on February 23, 2026. Bulls see a network that touches 20% of the web, finally building a toll booth on top of it. Bears see a company trading at 115x forward EBITDA that has to monetize a market that barely exists yet. The July 1 launch is the first hard evidence either side has to work with.

What Cloudflare Actually Launched on July 1

On its second annual “Content Independence Day,” Cloudflare opened a waitlist for its Monetization Gateway, a system that will let a site owner charge any automated caller for any resource behind Cloudflare, whether that is a web page, a dataset, an API, or an MCP (Model Context Protocol, the standard that lets AI agents call external tools) endpoint. Payments settle in stablecoins over x402, an open protocol that repurposes the long-dormant HTTP 402 “Payment Required” status code so machines can pay other machines without the site owner building any payment stack. The Gateway is opening to a waitlist rather than shipping to every customer at once, so this is an early-stage rollout, not a fully live revenue line.

Cloudflare also began moving from charging per crawl to charging per use. Instead of billing an AI crawler every time it fetches a page, publishers can now be paid when their content actually powers an answer or when an agent buys premium information for a task. Cloudflare’s first named partners for the effort include Ceramic.ai, You.com, and the newsletter platform beehiiv. The company justified the shift with a specific number: more than half of the crawl traffic from bots it classifies as legitimate goes toward re-fetching pages that have not changed since the last visit. Starting September 15, 2026, Cloudflare will also default to blocking mixed-use crawlers, meaning bots that gather data for both search indexing and AI training, on ad-supported customer pages unless owners opt out.

Matthew Prince, Co-Founder and CEO, framed the urgency directly in the July 1 announcement: “Now that the majority of traffic on the Internet is non-human, we must go further and act faster so that a sustainable ecosystem can emerge.” That line matters because the crossover already happened. At Investor Day, Prince said bot traffic surpassing human traffic was forecast for the first half of 2027, then admitted the company had already pulled the estimate forward twice and that bots had in fact already exceeded human traffic. The monetization layer is arriving into a market that got bigger faster than management planned.

See historical and forward estimates for Cloudflare stock (It’s free!) >>>

Why the Launch Confirms the Investor Day Thesis

The reason this launch reads as more than a press release is that it slots directly into the strategic architecture management laid out on June 9. Cloudflare describes its business as four “Acts” running on one network: application services (Act I), the Cloudflare One SASE security suite (Act II), the Workers developer platform (Act III), and agentic internet monetization (Act IV). The July 1 launch is Act IV, taking product shape for the first time.

Chief Strategy Officer Stephanie Cohen explained at Investor Day why Act IV compounds rather than cannibalizes: “Act 4, it’s not separate from the rest of Cloudflare. It’s only possible because of the foundations we built from Act 1 and Act 3.” The insight the transcript surfaces, which a headline cannot, is that the monetization layer does not need to generate much direct revenue to pay off. It drives demand into the existing, higher-margin businesses. Cohen noted that in the sectors most exposed to the agentic shift, Cloudflare is already seeing revenue growth north of 37%, pulling in customers like Reddit and People Inc. because publishers route content behind Cloudflare to control how agents reach it, and that control shows up in Act I and Act II revenue today.

The payment rail is further along than most investors realize. Cohen said Cloudflare already sees more than 2 billion “402 Payment Required” responses per day across its network, on rails built jointly with Coinbase and Stripe. Most of those do not yet result in a transaction. But the scaffolding is live and embedded in the internet, which is the hard part. As Cohen framed the opportunity, the goal is to move “from protecting websites and applications to monetizing trusted, automated demand.”

See how Cloudflare performs against its peers in TIKR (It’s free!) >>>

The Numbers Behind the Story

The financial reality checks both the enthusiasm and the risk. Cloudflare grew LTM revenue to $2.33 billion with a 73.3% gross margin, but LTM EBIT margin sits at negative 9.0%, and the company remains GAAP-unprofitable, with LTM diluted EPS of negative $0.25. The forward growth is what supports the story: analysts model a forward 2-year revenue CAGR of around 29% and a forward 2-year EBITDA CAGR of around 36%, per TIKR estimates. Management now targets a “Rule of 50” (revenue growth rate plus profit margin summing to 50 or more) for 2027, up from the Rule of 40 it has cleared for 22 straight quarters, and CFO Thomas Seifert guided to free cash flow margins reaching around 30% to 35% over time.

The most recent earnings reaction shows how little cushion the stock has when sentiment turns. On May 7, 2026, NET fell 23.62% in a single day. Its Q1 print beat on revenue, EPS, and free cash flow, but management paired it with a roughly 20% workforce reduction tied to an “agentic AI-first operating model.” The quarter was strong; the market punished the restructuring. That reaction is the clearest recent illustration of the bear case: at this multiple, execution ambiguity gets repriced fast.

Analyst sentiment reflects a genuinely divided market rather than a consensus buy. As of the July 2, 2026 TIKR data, the Street split is 17 Buys, 6 Outperforms, 9 Holds, 1 Underperform, and 1 Sell, with a mean target of around $244, essentially level with the current price. Wall Street, in other words, sees NET as roughly fairly valued today and is waiting for Act IV to prove it can convert traffic into revenue before underwriting more upside.

On valuation, the premium is stark and worth confronting directly. NET trades at 28.39x NTM EV/Revenue against an IT Services peer mean of 3.55x, per TIKR’s Competitors data. Akamai (AKAM) trades at 4.47x, GoDaddy (GDDY) at 2.68x, and Fastly (FSLY) at 3.94x on the same measure. That is roughly 8x the peer average. The premium is only defensible because those peers are largely bandwidth and hosting businesses growing at a fraction of Cloudflare’s rate, while NET is being priced as programmable infrastructure for AI workloads. Whether the July 1 monetization layer justifies paying that multiple is the exact question every NET holder has to answer, because if agentic revenue disappoints, there is no valuation floor near current levels.

TIKR Advanced Model Analysis

- Current Price: $242.41 (model entry price)

- Target Price (Mid): ~$716

- Potential Total Return: ~195%

- Annualized IRR: ~27% / year

See analysts’ growth forecasts and price targets for Cloudflare stock (It’s free!) >>>

Two revenue drivers carry the mid-case: continued Workers developer platform expansion, where Cloudflare added roughly one million net new developers in Q1 2026 alone, nearly matching all of 2025, and sustained enterprise deal momentum, with $1 million-plus deals up 73% year-over-year. The margin driver is the operating leverage Seifert is targeting through G&A automation and a lower cost to serve on developer and Act IV traffic. The primary risk is gross margin, which has compressed toward the low 70s over eight quarters; if that decline outruns operating leverage, the earnings base the model discounts never materialize. The upside is a world where agentic traffic monetization converts into real, high-margin revenue faster than the Street expects. The downside is a 20%-plus multiple de-rating on any single quarter of decelerating growth or renewed margin pressure.

Conclusion

The one number to watch is dollar-based net retention when Cloudflare reports Q2 2026 on July 30, alongside whether Seifert confirms the gross margin stabilization he flagged for the June quarter. Net retention held at 118% in Q1, down 2 points sequentially. A hold at or above 118% with confirmed margin stabilization tells you the enterprise flywheel is intact and the restructuring is working. A slip below that, or another quarter of margin decline, and the May 7 reaction stops looking like an overreaction. The July 1 launch gave the Act IV thesis a product to point at. July 30 is when investors find out whether the rest of the business is healthy enough to let that bet play out.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Cloudflare?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cloudflare, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cloudflare alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Cloudflare on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!