Key Takeaways for IDEXX Laboratories Stock as of July 2026

- Five buy ratings and five holds now sit against a $709 mean target, a 27% gap to the $558 close that Wall Street has not closed despite three straight quarters of raised guidance.

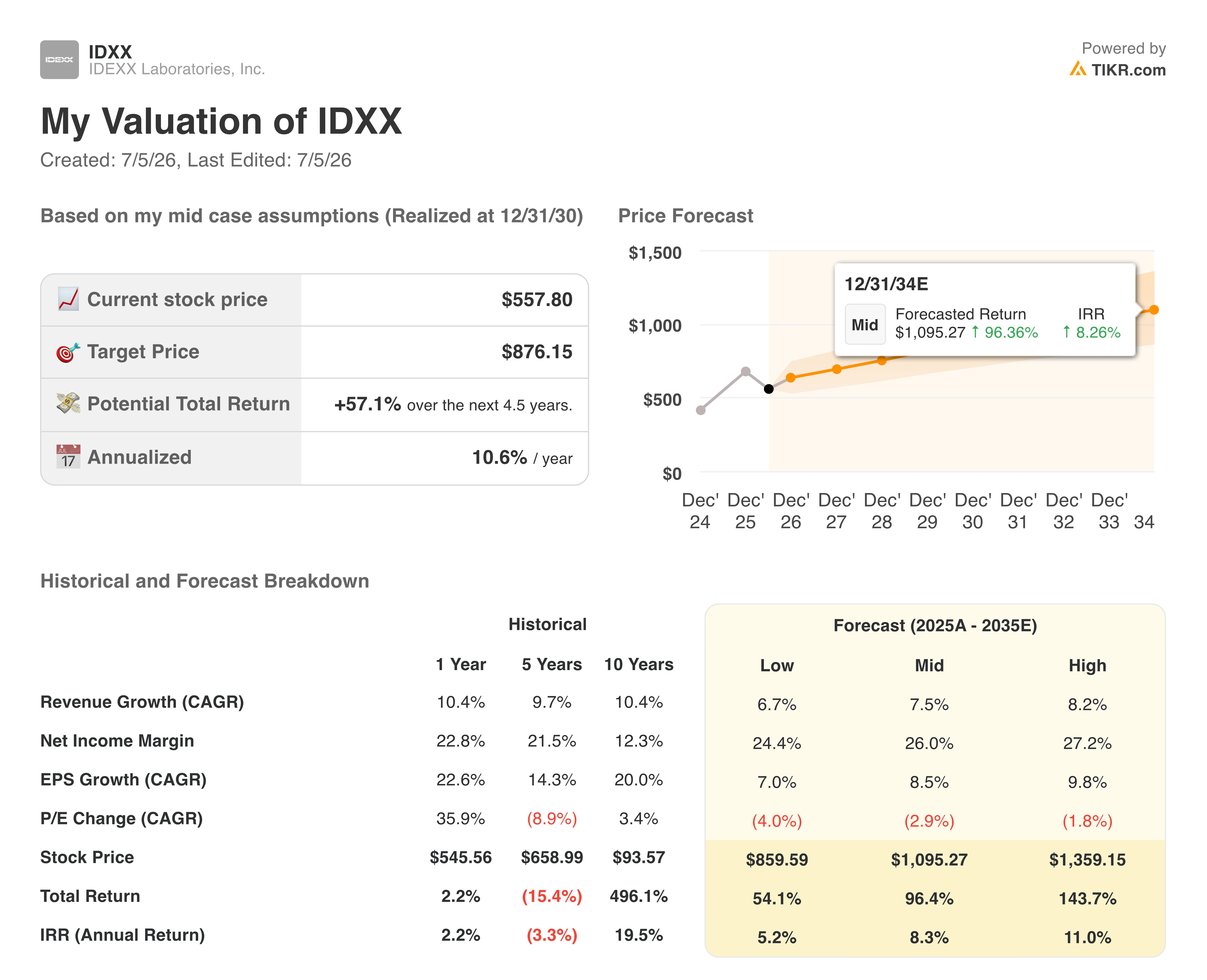

- TIKR’s mid-case model targets $876 by December 2030, translating into 57% total return and a 11% annualized rate on IDEXX Laboratories stock from current levels.

- Normalized EPS is set to climb from $3.47 in Q1 to a projected $4.42 by June 2027, an 11% year-over-year gain that suggests the stock trades cheap against its own earnings trajectory.

- Following the May 5 print, IDEXX raised full-year EPS guidance to $14.45-$14.90 and revenue to $4.68-$4.76 billion, with inVue Dx placements up 12% and Cancer Dx adoption spreading to 7,500 practices.

IDEXX Stock Rises as inVue Dx and Cancer Dx Adoption Broadens Recurring Revenue

IDEXX Laboratories (IDXX) posted first-quarter 2026 revenue of $1.14 billion, up 14% year over year, beating the consensus estimate of $1.11 billion by a wide margin. Diluted EPS climbed 17% to $3.47, and the Westbrook, Maine-based diagnostics maker used the print to raise its full-year outlook for the third time in recent memory.

That beat traced back to the Companion Animal Group, IDEXX’s largest segment, where revenue rose 15% to $1.05 billion. CAG Diagnostics recurring revenue grew 14% on a reported basis and 11% organically, with international regions posting 21% reported growth against 12% growth in the U.S.

Underneath that number sat a tension the company has wrestled with for over a year: U.S. same-store clinical visits fell roughly 1% in the quarter. Yet IDEXX still outgrew that visit decline by about 1,100 basis points, a gap CFO Andrew Emerson attributed to diagnostic frequency and utilization gains rather than volume alone.

Instrument placements told a similar story of quality over headline volume. IDEXX placed 1,100 inVue Dx analyzers in Q1, a number some analysts viewed as light against the 5,500 full-year target. CEO Mike Erickson pushed back on that read directly at the Stifel Jaws & Paws conference on May 27: “we’re already comfortably in that band” referring to the $3,500-$5,500 revenue-per-box range the company had flagged for the platform.

That comfort extended to Cancer Dx, IDEXX’s oncology diagnostic now used across 7,500 practices, with nearly 70% of North American volume run as part of a broader panel. Roughly 20% of that volume comes from practices that are not primary IDEXX reference-lab customers, meaning the test is pulling in business the company did not previously have.

Operating leverage followed the top-line strength. Operating margin widened to 31.8% for the quarter, up 0.1 percentage point, while gross margin expanded 90 basis points to 63.4% on the back of recurring revenue growth in VetLab consumables and reference lab volumes.

Management used that combination of visit resilience and margin expansion to lift full-year EPS guidance to $14.45-$14.90 per share, up from $14.29-$14.80, and raised revenue guidance to $4.68-$4.76 billion. The leadership transition from Jay Mazelsky to incoming CEO Mike Erickson, finalized in May, adds a variable to the multi-year growth algorithm the market is now pricing.

Wall Street Holds a Split Rating on IDXX Stock at a $709 Target

Wall Street’s consensus on IDEXX Laboratories stock stands at five buy ratings, four outperforms, five holds and one underperform, with the sell-side split roughly evenly between bullish and neutral camps.

The mean target price of $709 sits 27% above the July 2 close of $558, and the median target of $713 confirms the gap is not being driven by outliers. That target has held in a tight band since March 2026, even as the stock itself dropped from $676 to $526 before recovering to $558, suggesting analysts are anchoring to the raised guidance rather than short-term price action.

Wall Street Expects IDXX Stock’s Normalized EPS to Climb to $4.42 by Mid-2027

Normalized EPS came in at $3.47 for the quarter ended March 2026, up from $3.08 a year earlier, a 17% increase that beat what the Street had modeled heading into the print.

Consensus now calls for normalized EPS of $3.94 for the June 2026 quarter, an 8% year-over-year gain that reflects the raised full-year guidance range of $14.45 to $14.90.

Looking further out, the Street models normalized EPS reaching $3.89 by December 2026 and climbing to $4.42 by June 2027, representing 12% growth in both periods. That trajectory implies accelerating earnings power even as the comparison base gets tougher in the back half of 2026, precisely the dynamic Jon Block pressed management on during the Q1 call.

The unresolved question sits in the acceleration math: can international utilization gains and Cancer Dx’s expanding panel offset the tougher second-half comps enough to hit the top end of that EPS range, or does the Street’s $4.42 mid-2027 figure already assume more visit stabilization than IDEXX has delivered so far.

TIKR’s $876 Target on IDEXX Laboratories Stock Holds if Cancer Dx Scales Into 2028

TIKR’s mid-case model values IDEXX Laboratories at $876 by December 2030, implying 57% total return from the current price of $558, or 11% annualized over 4.5 years.

That annualized rate outpaces the 3% ten-year revenue CAGR embedded in most mature diagnostics peers, positioning IDEXX Laboratories stock as a premium-growth compounder rather than a defensive healthcare holding.

The target is reachable if the same forces driving Q1 hold: instrument placements staying within the $3,500-$5,500 revenue-per-box band, Cancer Dx expanding toward the 2028 target of covering 50% of major cancers, and international CAG Diagnostics recurring revenue sustaining double-digit organic growth.

Erickson’s confirmation that inVue Dx has already reached that revenue band with only two of three planned menu items live suggests the runway TIKR’s model assumes is not yet fully reflected in the current placement pace.

Should You Invest in IDEXX Laboratories, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up IDEXX Laboratories, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track IDEXX Laboratories, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze IDXX stock on TIKR for Free →