Key Stats for Eli Lilly Stock

- Current Price: $1,213.91

- Target Price (Mid): ~$2,076

- Street Target: ~$1,220

- Potential Total Return: ~71%

- Annualized IRR: ~13% / year

- Earnings Reaction: 3.07% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Eli Lilly and Company (LLY) walked into the Goldman Sachs Global Healthcare Conference on June 9 with a message that reframes how big this story could still get. Ken Custer, an EVP at the company, told the room that despite tens of millions of people already on these medicines, the obesity category sits at roughly 3% penetration of the patients who could benefit. That is the number the bulls keep coming back to. It is also the number the bears think is already priced into a stock that has risen about 54% over the past year to trade near $1,214, just under the record close of $1,229.93 it set on June 29.

That tension is what makes Eli Lilly stock 2026 such a hard call right now. The company is executing at a level almost no large-cap can match, yet it carries a valuation that leaves no margin for a stumble. This week sharpened both sides of the argument at once. A landmark Medicare access program went live on July 1, and a Congressional probe into the company’s China clinical trials set a July 17 response deadline.

What Management Actually Revealed at Goldman Sachs

The conference was not a routine update. Custer used it to argue that Lilly is no longer a one-drug obesity company but a platform. The most important disclosure was about retatrutide, the investigational triple receptor agonist (a drug that activates three metabolic pathways at once) that could become Lilly’s third obesity medicine.

Most of the market has modeled retatrutide as a high-dose product for the most severe patients, given weight loss that reached 30.3% at 104 weeks in the TRIUMPH-1 study. Custer pushed back on that framing. He pointed to the low-dose data instead. “On that dose, patients lost 19% of their body weight, which is not bad, competitive with our other dual agonists and they got there with just a single dose titration step,” Custer said, adding that discontinuations were “nominally lower than placebo.” That matters because it turns retatrutide from a niche drug into what he called a potential “workhorse” across the broader obesity market.

The strategic vision went further. Custer described a future where patients “start, stay and switch” between Zepbound, Foundayo, and retatrutide on a common platform. “Maybe someday rather than worrying about whether they’re taking retatrutide or Zepbound or Foundayo, they’ll just be taking Lilly for overweight obesity,” he said. For investors, that reframes the internal competition worry: new drugs are meant to expand the pool, not cannibalize the existing one.

See historical and forward estimates for Eli Lilly stock (It’s free!) >>>

Why the Stock Is Near a Record

The catalyst pushing Eli Lilly stock back toward its highs in 2026 is access, not a new drug. Starting July 1, the Centers for Medicare and Medicaid Services launched the Medicare GLP-1 Bridge, a demonstration program that lets eligible Part D members get covered weight-loss drugs for a flat $50 monthly copay through the end of 2027. This is a government program, not a Lilly exclusive: the covered list also includes Novo Nordisk’s Wegovy, so the read-through is shared across large-cap pharma. What makes it a Lilly story is the share of shelf. Lilly holds two of the covered products, Zepbound and its oral pill Foundayo, and the program could reach roughly 20 million eligible Medicare patients.

Mike Czapar, a Lilly commercial leader on the call, confirmed the timeline directly. “Beginning in July 1, we actually have access as part of the Medicare GLP bridge program,” Czapar said, noting the consumer ad campaign had just started during NBA broadcasts. That is the volume story the bulls want: a policy shift that widens the door for new patients rather than squeezing price. For six months, bears argued that every pricing concession Lilly made would bleed margin faster than volume could refill it. A Medicare access expansion complicates that frame.

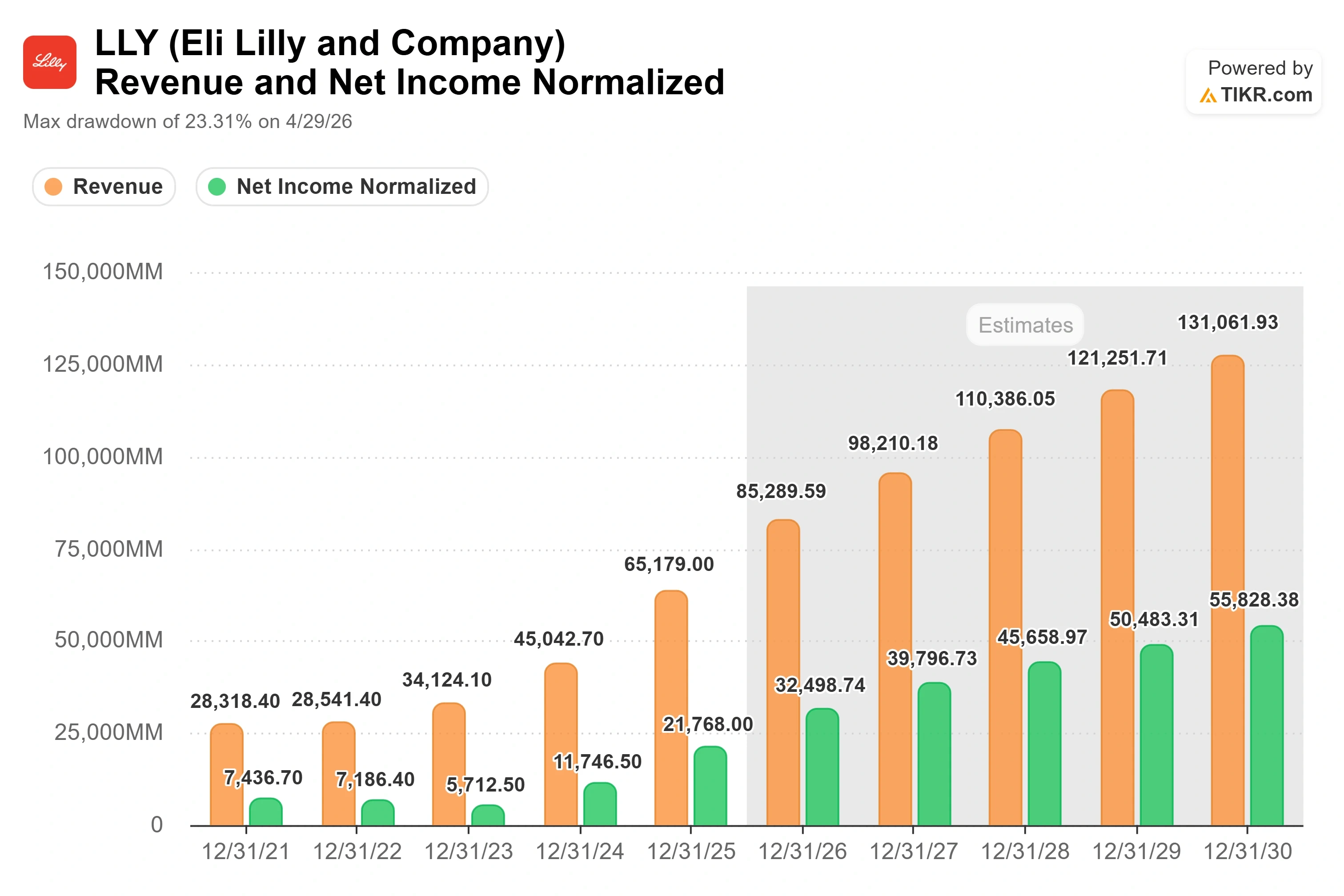

The financial base underneath this is real. Q1 2026 revenue came in at $19.8 billion, and the stock rose 3.07% on April 30 after that report beat estimates, per TIKR data. On the earnings call, management said Mounjaro and Zepbound, the tirzepatide franchise, generated $12.8 billion in combined global revenue that quarter. Custer noted at Goldman Sachs that Lilly has committed “a little over $50 billion in manufacturing commitments announced since just 2020” to keep supply ahead of demand, much of it on a common platform that can flex between tirzepatide, retatrutide, and future molecules.

The Overhang the Market Is Watching

The reason this is not a clean bull story arrived on June 30. The House Select Committee on the Chinese Communist Party, chaired by Rep. John Moolenaar, sent letters to five major drugmakers, including Lilly, seeking records on clinical trials conducted in China, some at military-affiliated hospitals and in the Xinjiang region. Lilly stock closed down 2.48% at $1,199.43 that day. According to the committee, there is no evidence Lilly engaged in illegal activity or wrongdoing, and the records request is due July 17.

The concern is strategic rather than legal. Lilly has deepened its China footprint, including an oncology and immunology collaboration with Innovent Biologics worth up to $8.8 billion announced in February, and on June 30, it handed Innovent commercial control of its breast cancer drug Verzenios in mainland China. For a company whose growth thesis depends on global scale, any friction between U.S. policy and its China research base is a variable investors now have to price. It is unlikely to move the GLP-1 numbers directly, but it adds a headline risk that a premium-valued stock does not shrug off easily.

Where Lilly Trades Against Its Peers

Lilly’s valuation only makes sense next to its growth. The stock trades at around 25x NTM EV/EBITDA and around 33x NTM P/E, per TIKR. That is a steep premium to the peer group. Merck sits at roughly 18x NTM EV/EBITDA and about 21x NTM P/E, while Novo Nordisk, Lilly’s most direct GLP-1 rival, trades at around 11x NTM EV/EBITDA and about 16x NTM P/E, per TIKR’s Competitors page. Johnson & Johnson trades near 18x NTM EV/EBITDA.

The premium is defensible only if the growth holds. Lilly’s forward 2-year revenue CAGR is around 23%, and its forward EPS CAGR is around 36%, versus low-single-digit or declining growth at most of that peer set. Novo has warned its own 2026 sales could fall. So the market is paying up for the only mega-cap pharma name with a GLP-1 franchise and no credible near-term generic threat. Whether that premium compresses depends on execution, not on the multiple re-rating higher from here.

See how Eli Lilly performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $1,213.91

- Target Price (Mid): ~$2,076

- Potential Total Return: ~71%

- Annualized IRR: ~13% / year

See analysts’ growth forecasts and price targets for Eli Lilly stock (It’s free!) >>>

This analysis uses the TIKR mid-case, which reflects the middle of the scenario range rather than the more aggressive high case. On mid-case assumptions realized by December 31, 2030, the model reaches a target of around $2,076, a total return of around 71%, and an annualized return of around 13% per year over roughly 4.5 years.

Two revenue drivers carry the case. The first is sustained GLP-1 volume growth from Mounjaro and Zepbound, now amplified by Medicare access, widening the eligible patient pool. The second is Foundayo’s ramp into the oral obesity market, where the pill format is pulling in patients new to the category rather than switching existing users. The margin driver is operating leverage: a largely fixed manufacturing base absorbing rising volume, which lifts net income margin toward around 43% in the mid case. The primary risk is U.S. pricing pressure, where net realized price is drifting lower even as volume grows.

The upside case is that Medicare access plus retatrutide as a broad-use “workhorse” pushes revenue growth above the model’s roughly 12% mid-case assumption and the high-case target near $3,720 comes into view. The downside case is that pricing erosion outpaces volume gains and the China overhang caps the multiple, leaving the low-case path near $2,219 or below.

Conclusion

The clean test comes at Lilly’s next earnings call, expected around August 5, 2026. Watch Foundayo’s weekly prescription run rate. Good looks like scripts accelerating through the back half of Q3 as the July 1 Medicare switch and full TV advertising compound, with management quantifying early Bridge enrollment. Bad looks like flat script growth, which would tell the pricing bears the access expansion is not converting patients into volume and would put the premium multiple under real pressure. Before that, the July 17 China response deadline is the near-term headline risk. The stock is priced for Lilly to keep executing. August is when it has to show the patients actually showed up.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Eli Lilly?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Eli Lilly, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Eli Lilly alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Eli Lilly on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!