Key Stats for McDonald’s Stock

- Past-Week Performance: -5.4%

- 52-Week Range: $283.5 to $341.8

- Current Price: $308.9

What Happened?

McDonald’s (MCD) drove the strongest quarterly comparable guest count gap over near-end competitors in recent history during Q4 2025, as the world’s largest fast-food chain by systemwide sales converted a full-year value push into $139.4 billion in systemwide revenue and closed at $308.85 per share.

The Q4 2025 earnings call on February 11 confirmed U.S. comparable sales rose 6.8%, beating expectations, as two promotions — MONOPOLY, a digital loyalty game that generated nearly 500 million plays, and the Grinch Meal, which set the highest single-day sales record in company history — delivered the strongest traffic performance in years.

Loyalty membership, the digital program that tracks frequent customers and drives repeat visits, reached 210 million 90-day active users across 70 markets in 2025, nearly doubling the $20 billion in annual systemwide loyalty sales recorded in 2023, while U.S. loyalty members more than doubled their visit frequency after enrolling compared to the prior year.

Chief Financial Officer Ian Borden stated on the Q4 2025 earnings call that “a customer in the 12 months before they joined our loyalty program visited us 10.5x — in the 12 months after they became a loyalty member, they visited us 26x,” directly supporting McDonald’s April 2026 McValue 2.0 launch of $3-or-less menu items and $4 breakfast deals as the next lever to sustain low-income traffic share.

McDonald’s targets 50,000 restaurants by end of 2027 through approximately 2,600 gross openings in 2026, while a planned McCafe beverage lineup targeting a $100-plus billion global category and a fall 2026 investor update are set to reframe the company’s long-term growth identity beyond burgers and fries.

Wall Street’s Take on MCD Stock

The Q4 2025 comp sales acceleration, which pushed U.S. traffic to its widest gap over near-end competitors in recent history, directly changes the forward earnings trajectory by anchoring EPS growth on volume rather than price, a more durable foundation heading into a value-pressured 2026.

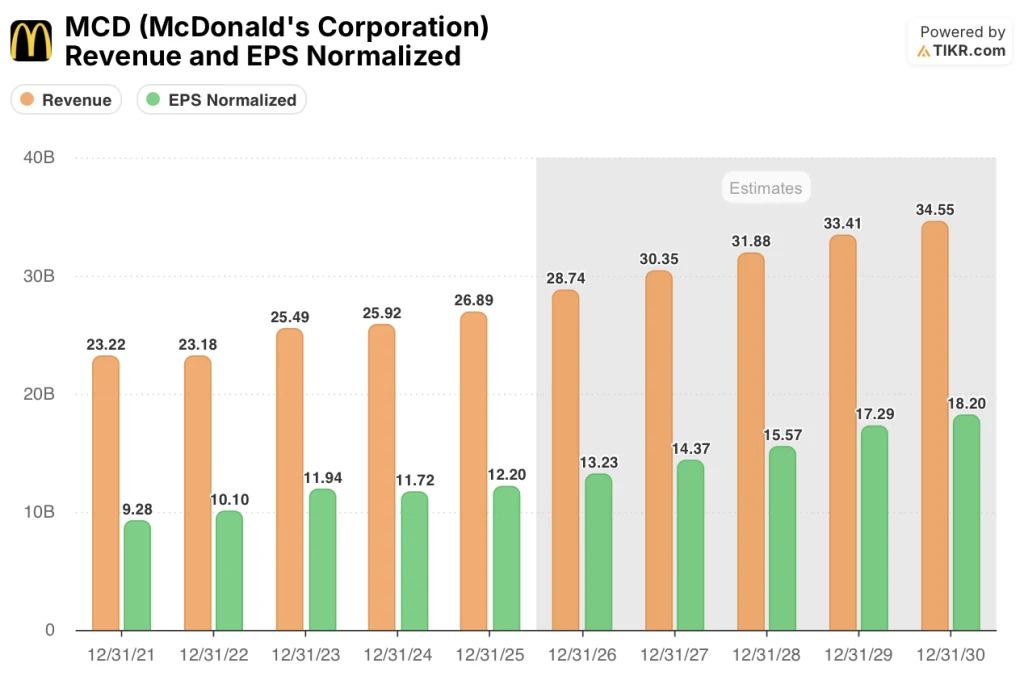

TIKR consensus estimates revenue growing from $26.9 billion in 2025 to $28.7 billion in 2026, a 6.9% increase, while normalized EPS advances from $12.20 to $13.23, supported by the McValue 2.0 rollout in April and the McCafe beverage launch later in 2026 that together expand check size across dayparts.

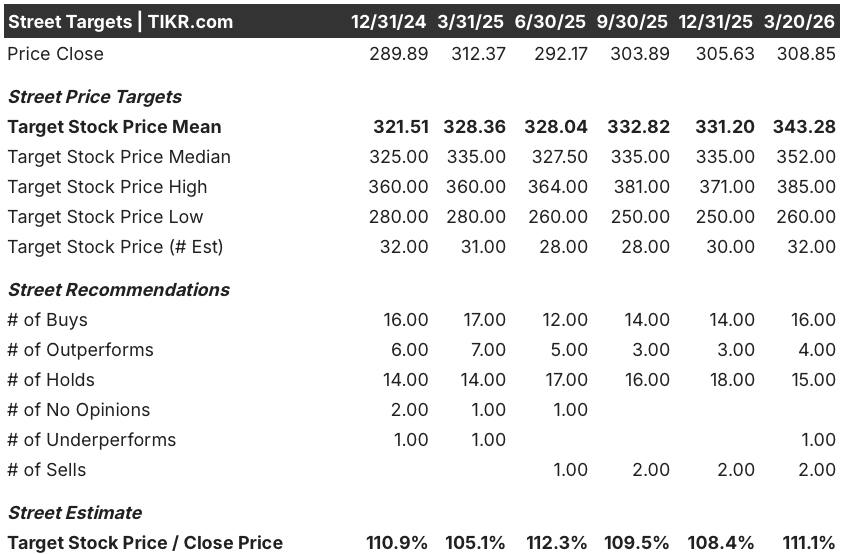

Sixteen buy ratings, four outperforms, fifteen holds, one underperform, and two sells from 32 analysts put the mean price target at $343.28, implying 11.1% upside from $308.85, with the consensus anchored to steady unit growth and loyalty-driven traffic rather than a re-rating event.

The $260 bear target reflects the risk that franchisee margin pressure forces McDonald’s to extend EVM subsidies beyond the planned timeline, while the $385 bull target prices in a successful McCafe national rollout and the loyalty program reaching its 250 million 90-day active user target by end of 2027.

What Does the Valuation Model Say?

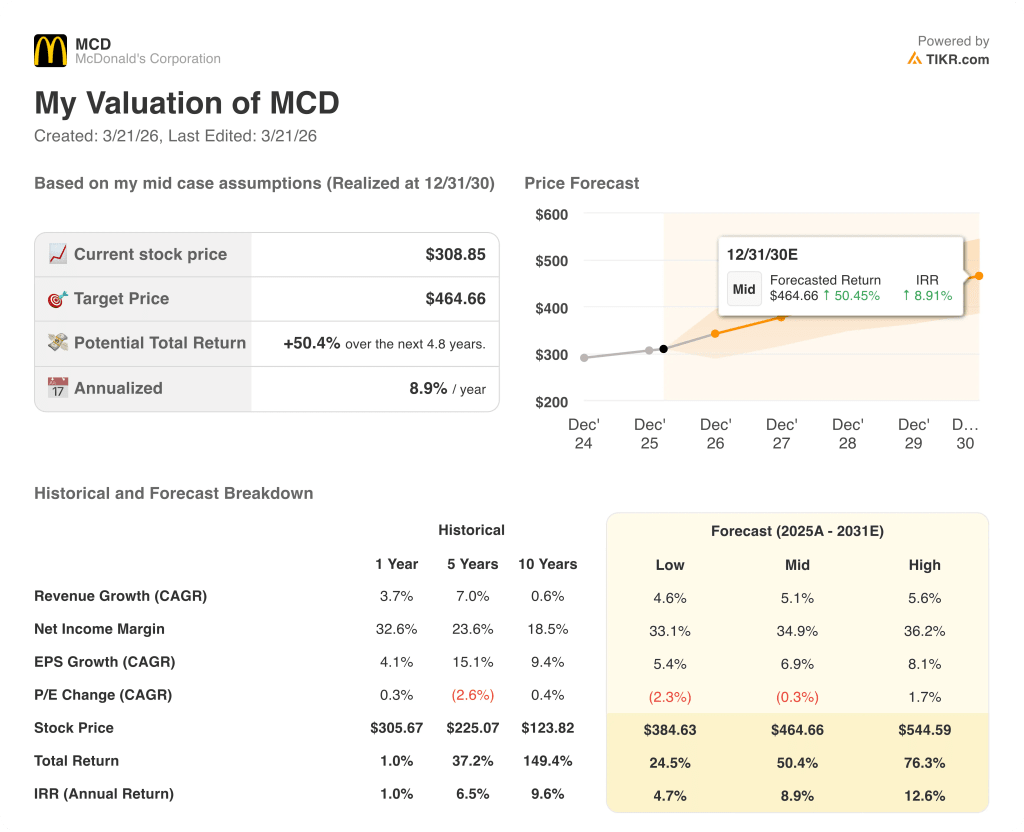

The TIKR mid-case target of $464.66 implies a 50.4% total return at an 8.9% IRR by December 2030, driven by a mid-case revenue CAGR of 5.1%, EBIT margin expansion from 46.9% to 51.4%, and FCF nearly doubling from $7.2 billion to $14.4 billion as the asset-light franchise model scales without proportional cost growth.

The market prices MCD as a low-single-digit grower, but FCF margins expanding 14.8 percentage points to 41.5% by 2030 make the compounding case structural, not cyclical.

Loyalty members visiting 26x annually versus 10.5x before enrollment confirms the McCafe beverage rollout and McValue 2.0 are frequency levers, not discounting tactics, directly justifying the TIKR $464.66 target.

The April McValue 2.0 launch and the 46 million U.S. 90-day active users confirm the digital and value infrastructure is live, not in development, making this a execution story, not a speculation.

Franchisee EVM subsidy withdrawal is the single variable that breaks the margin expansion model; if operators pull back on value pricing to protect cash flow, low-income traffic share reverses and the volume thesis collapses.

Q1 2026 comparable sales, due in May, confirm whether the 100-basis-point weather drag in late January masked underlying momentum or signaled the start of a sequential deceleration; watch the U.S. guest count number specifically.

Should You Invest in McDonald’s Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MCD stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track McDonald’s Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MCD stock on TIKR for Free →