Key Stats for AMETEK Stock

- Past-Week Performance: -2.4%

- 52-Week Range: $145 to $242.1

- Current Price: $209.4

What Happened?

Record orders of $7.58 billion in 2025, up 11.3%, confirm that AMETEK, a maker of precision electronic instruments and electromechanical devices for industrial and defense markets, has shifted from a demand drought to a broad-based recovery, with shares at $209.37 sitting well below the 52-week high of $242.05.

On February 3, AMETEK reported Q4 2025 adjusted diluted earnings per share of $2.01, up 7% and ahead of the LSEG consensus of $1.94, while revenue of $2.00 billion beat estimates of $1.95 billion and marked 13% growth; the same day, the company acquired LKC Technologies, a maker of portable retinal diagnostic devices that expand AMETEK’s eye care instrumentation portfolio inside its Electronic Instruments Group.

The Electromechanical Group, which produces motors, interconnects, and precision motion components, drove the sharpest operating leverage in Q4, with organic sales up 14% and operating income up 28%, pushing segment margins to 22.7%, up 240 basis points, while free cash flow hit a record $527 million with 132% conversion against net income.

David Zapico, Chairman and Chief Executive Officer, stated on the Q4 2025 earnings call that “we have a tremendous capability of bringing those margins up,” referencing FARO Technologies, a 3D metrology and laser scanning business acquired for roughly $920 million in mid-2025, which currently runs at mid-teens EBITDA margins against AMETEK’s 31.5% company-wide EBITDA margin target.

On February 12, AMETEK raised its quarterly dividend by 10% to $0.34 per share, reinforcing capital return discipline even as management disclosed capacity to deploy over $5 billion on acquisitions while maintaining an investment-grade credit rating.

A $7.87 to $8.07 adjusted EPS guide for 2026, a $100 million incremental investment in R&D and commercial initiatives, a FARO margin expansion roadmap targeting 30% EBITDA by year three, and a record $3.58 billion backlog entering the year together make the forward earnings trajectory substantive, not speculative.

Wall Street’s Take on AME Stock

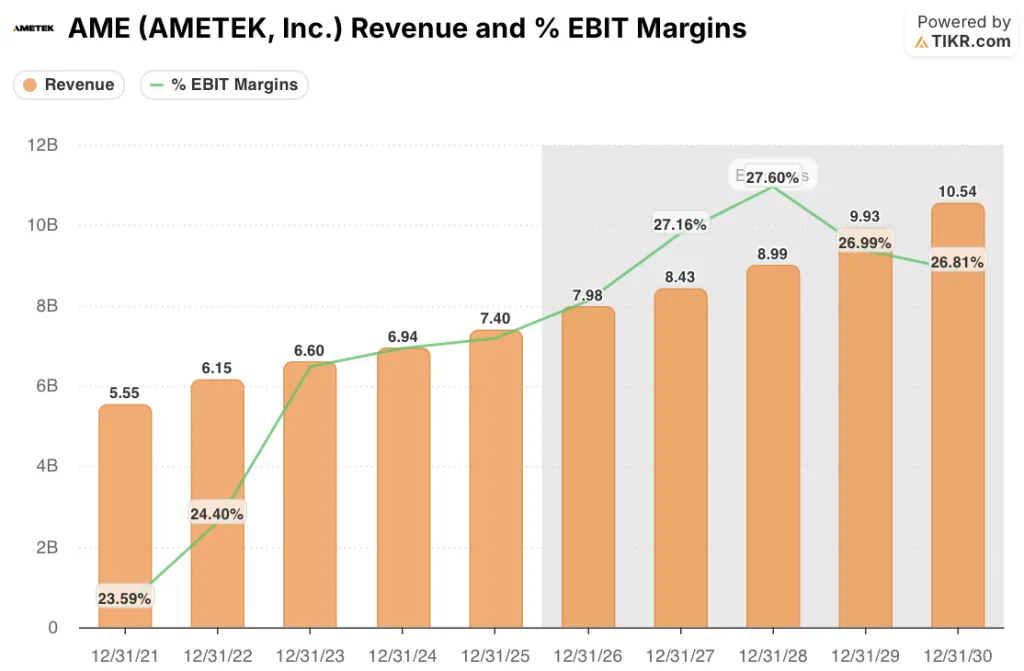

AMETEK’s record Q4 backlog of $3.58 billion, built on 18% total order growth and organic order growth of 7%, provides near-certain revenue visibility into 2026 and directly supports the TIKR model’s $7.98 billion revenue estimate, up 7.8% from 2025.

AMETEK’s EBIT stood at 26.2% in 2025 and is forecast to reach 27.6% by 2028, driven by FARO’s restructuring and the ongoing integration of Kern Microtechnik into AMETEK’s proven operating infrastructure.

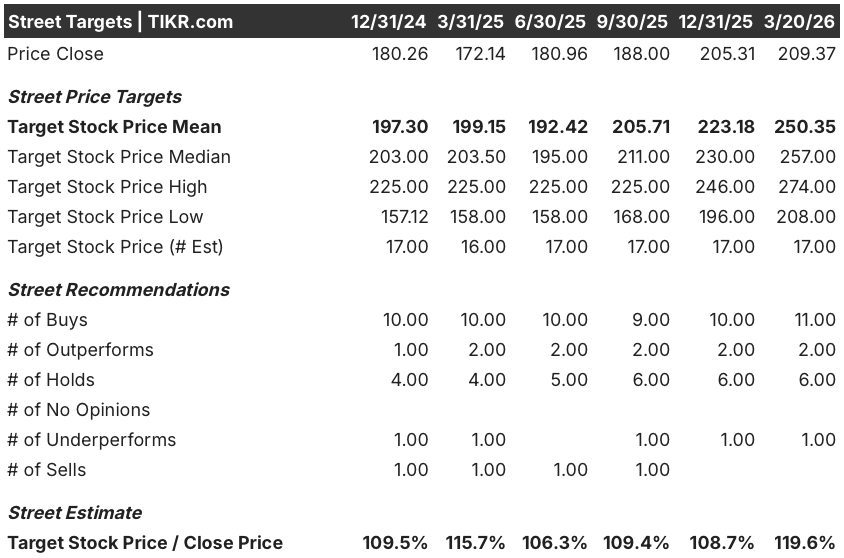

Thirteen analysts carrying buy or outperform ratings against six holds and one underperform have pushed the mean price target to $250.35, implying 19.6% upside from the current $209.37, anchored by expectations for normalized EPS of $8.05 in 2026 and $8.72 in 2027 as FARO margin improvement begins flowing through reported results.

The spread between the street low of $208.00 and the street high of $274.00 maps directly onto two known variables: the low reflects execution risk on FARO’s mid-teens EBITDA margin doubling to 30%, while the high assumes that the AMETEK Growth Model, its acquisition integration playbook, delivers FARO synergies on the three-year timeline management committed to on the February 3 earnings call.

What Does the Valuation Model Say?

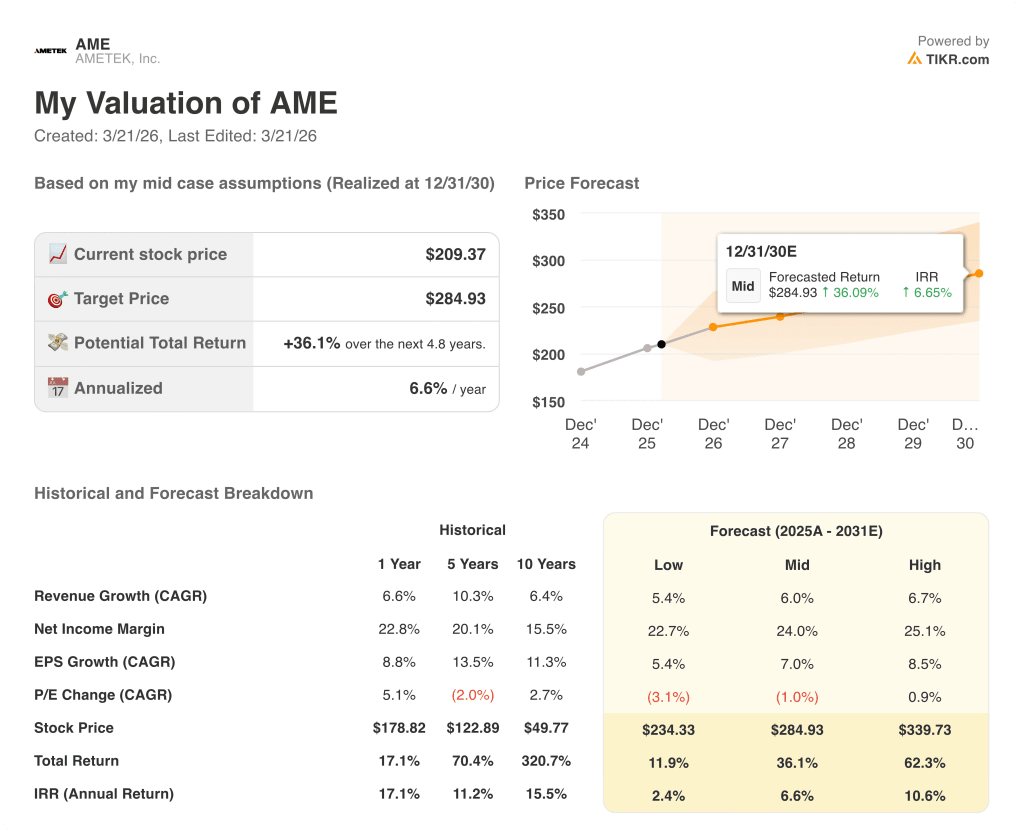

The TIKR mid-case model assigns a $284.93 price target on 6.0% revenue CAGR and a 24.0% net income margin assumption, both of which are conservative relative to AMETEK’s five-year historical revenue CAGR of 10.3% and its Q4 core operating margin of 27.6%, suggesting the model already discounts execution risk generously.

The market is pricing FARO’s margin dilution as permanent, but AMETEK’s Q4 core incremental margins of 45% prove its conversion capability is intact.

AMETEK’s $1.86 billion free cash flow estimate for 2026, up 11.5% from 2025, directly funds the $5 billion-plus acquisition capacity management quantified on February 3, supporting the TIKR model’s 6.0% revenue CAGR through compounding inorganic growth.

Zapico’s confirmation that December 2025 was AMETEK’s single strongest order month on record signals that the organic recovery the model assumes is already underway, not projected.

Tariff-driven demand disruption is the one risk that breaks the model’s low-to-mid-single-digit organic growth assumption, as any renewed pricing dislocation in AMETEK’s process instrumentation segment would delay the EIG organic inflection management is counting on in the second half of 2026.

Q1 2026 earnings, expected on or around May 7, will confirm whether FARO’s margin trajectory and EIG organic growth are tracking; watch for core EBIT margins above 26.5% and organic orders sustaining above 5%.

Should You Invest in AMETEK, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AME stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMETEK, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AME stock on TIKR for Free →