Key Stats for Xometry Stock

- Past-Week Performance: +6.2%

- 52-Week Range: $18.6 to $73.9

- Current Price: $39.2

What Happened?

Xometry (XTMR), an AI-native marketplace that digitally connects buyers to custom manufacturing suppliers across 50 countries, crossed into full-year profitability for the first time in FY2025, posting $18.5 million in adjusted EBITDA against a $9.7 million loss the prior year, even as the stock sits at $39.20, well below its 52-week high of $73.87.

On February 24, Q4 revenue of $192.4 million beat the $183.1 million consensus by 5%, with marketplace revenue, the core platform business that drives gross margin expansion, accelerating to 33% growth and pushing adjusted EBITDA to $8.4 million against a $6.6 million estimate.

Marketplace gross margin, the share of each transaction dollar Xometry keeps after paying suppliers, reached 35.3% in Q4, up from 25% four years ago, as the company’s proprietary pricing algorithms improve continuously with each new buyer and supplier interaction added to the network.

On the same day, Xometry announced that President Sanjeev Singh Sahni will succeed co-founder Randy Altschuler as CEO effective July 1, with Altschuler transitioning to Executive Chair, a deliberate succession framed around accelerating the product-led growth strategy that drove FY2025’s profitability inflection.

James Miln, Chief Financial Officer, stated on the Q4 2025 earnings call that “as we progress towards $1 billion in revenue, we anticipate to continue to deliver at least 20% incremental adjusted EBITDA leverage annually,” directly anchoring the company’s margin expansion commitment to its revenue scaling path.

Xometry’s path to durable profitability rests on three compounding drivers: scaling enterprise accounts with $10 million-plus annual spend potential, expanding international revenue from 18% toward a 30% to 40% long-term target, and deploying the March 3 Enterprise Machining Lead Time Prediction Model, which uses a training dataset four times larger than its predecessor to deepen supplier matching precision and extend Xometry’s pricing moat.

Wall Street’s Take on XMTR Stock

The Q4 2025 earnings beat, which confirmed Xometry’s first full year of adjusted EBITDA profitability, directly sets up a FY2026 where TIKR estimates EBITDA nearly triples from $18.5 million to $50 million as enterprise account revenue and marketplace gross margin continue compounding.

XMTR’s revenue accelerates from $686.6 million in FY2025 to an estimated $830 million in FY2026 and $990 million in FY2027, driven by enterprise accounts growing 40% in FY2025 and the March 3 Enterprise Machining Lead Time Prediction Model, which deepens supplier matching precision and expands auto-quoting across more materials and processes.

EBITDA margins are also forecasted to expand from 2.7% in FY2025 to 5.8% in FY2026 and 8.2% in FY2027, reflecting the inherent leverage of an asset-light marketplace model where operating costs grow at half the rate of revenue, as demonstrated in Q4 when non-GAAP expenses rose 15% against 30% revenue growth.

Meanwhile, its normalized EPS rises from $0.38 in FY2025 to $0.72 in FY2026 and $1.16 in FY2027, compounding at 89.7% and 61.2% respectively as the profitability inflection already visible in Q4 carries into the full-year results.

Ten analysts cover XMTR, with 6 rated “buy” or “outperform” and 4 “hold,” and their mean price target of $62.22 implies 58.7% upside from $39.20 as the Street prices in the profitability trajectory but has not yet fully credited the enterprise account scaling story.

The PT spread from $54 to $75 reflects a clear binary: the $54 floor prices a scenario where enterprise account growth stalls and the CEO transition disrupts product-led momentum, while the $75 ceiling aligns with Xometry sustaining 30%-plus marketplace growth and accelerating accounts past the $10 million spend threshold.

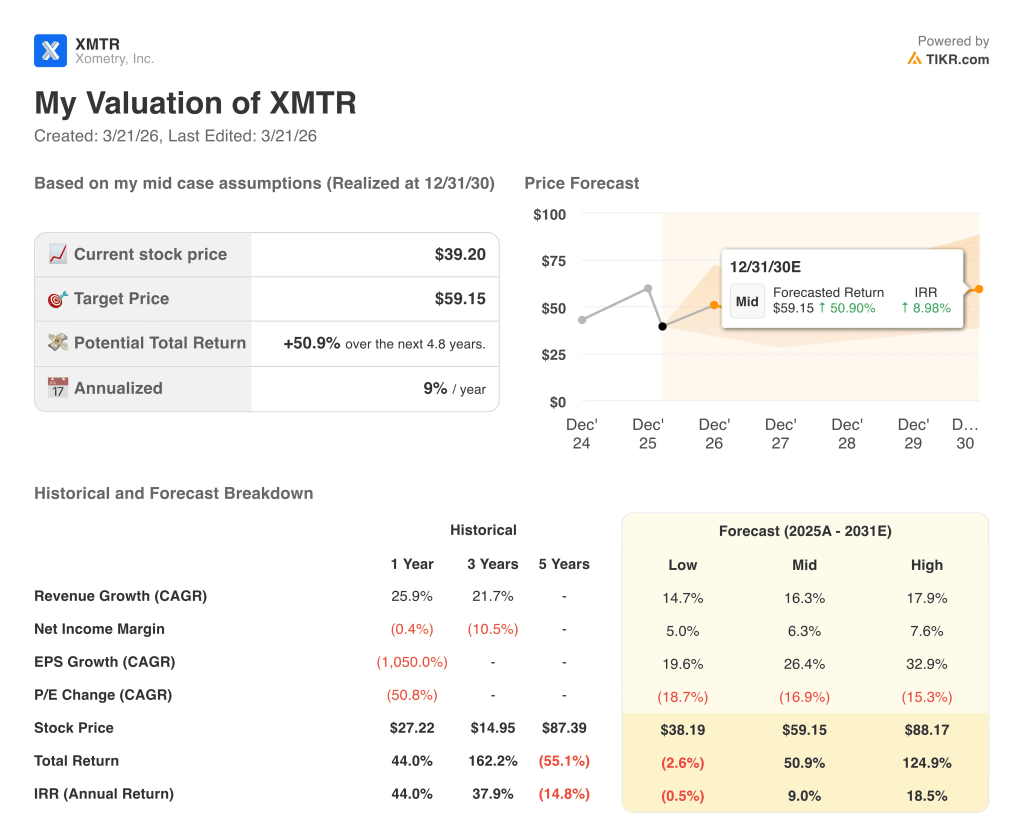

What Does the Valuation Model Say?

TIKR’s mid-case target of $59.15 implies 50.9% total return to December 2030 at a 9.0% IRR, anchored by a 16.3% revenue CAGR and net income margins recovering from -0.4% in FY2025 to 6.3% by the end of the forecast period, a trajectory justified by marketplace gross margin expanding steadily from 25% four years ago to 35.3% today.

The market prices XMTR as a pre-profit marketplace; marketplace gross margin has expanded 1,030 basis points over four years, proving the unit economics are structurally improving.

FCF turned positive at operating cash flow level in FY2025 at $6.1 million, and TIKR models full free cash flow turning positive by FY2027 as CapEx stabilizes around 6% of revenue, supporting the $59.15 target.

Sanjeev Singh Sahni’s July 1 CEO transition, paired with the March 3 product launch, signals leadership continuity rather than disruption; the number to watch in Q1 results is whether marketplace gross margin holds above 35%.

If enterprise accounts with $500,000-plus annual spend fail to grow beyond the current 140, incremental adjusted EBITDA leverage collapses and the TIKR model’s 16.3% revenue CAGR assumption breaks.

Q1 2026 earnings, expected in late April, will confirm whether the $187 to $189 million revenue guide and $6.5 to $7.5 million adjusted EBITDA target are tracking; marketplace gross margin above 35% is the single most important number to watch.

Should You Invest in Xometry, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up XMTR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Xometry, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze XMTR stock on TIKR for Free →