Key Stats for Monolithic Power Stock

- Past-Week Performance: +1.5%

- 52-Week Range: $438.9 to $1,256.22

- Current Price: $1,068.9

What Happened?

Fourteen consecutive years of revenue growth culminated in a restatement filing on February 27 — Monolithic Power Systems (MPWR), a semiconductor company specializing in power management chips that regulate electricity across AI servers, electric vehicles, and data storage devices, posted $2.8 billion in FY2025 revenue, up 26.4%, even as its largest segment, Enterprise Data, shrank 2%, proving the breadth of its business model carries the stock near $1,069.

Q4 2025 revenue of $751.2 million beat the $739.9 million analyst consensus, and CFO Bernie Blegen raised the floor for Enterprise Data growth in 2026 to at least 50%, up from a prior range of 30% to 40%, driven by expanding backlog stretching into Q3 2026.

Non-Enterprise Data end markets, which include automotive power chips, storage, communications, and industrial segments, grew over 40% combined in 2025, with automotive up 43.1% and Storage and Computing up 46.0%, outpacing analog industry peers growing at roughly 10% to 15% annually by the company’s own historical benchmark.

MPS announced on February 5 that CFO Bernie Blegen would retire following the 2025 annual report, with Corporate Controller Rob Dean named interim CFO, while CEO Michael Hsing stated on the Q4 2025 earnings call that “we won many design wins across the board, not from one company, one large company, and we have multiple customers — they’re all very big,” directly referencing its hyperscaler customer base.

A 28% dividend increase to $2.00 per share payable April 15, a $493.4 million remaining buyback authorization, a first-to-sample 800-volt data center power solution, and fully integrated 48-volt automotive zonal controllers launching in 2026 together position MPS to extend its share gains across AI infrastructure, automotive electrification, and optical interconnects over the next three to five years.

Wall Street’s Take on MPWR Stock

Enterprise Data backlog extending into Q3 2026, combined with non-Enterprise Data markets growing over 40% in FY2025, directly supports TIKR’s estimate of 21.4% revenue growth in 2026, up from the 26.4% FY2025 base, as multiple demand streams compound simultaneously.

Normalized EPS, which strips out one-time tax charges like the $144.7 million H.R.1 Act impact that compressed reported FY2025 net income 61%, rises from $17.77 in FY2025 to an estimated $21.52 in 2026 (+21.1%) and $46.23 by 2030, supported by EBIT margins expanding from 35.2% to an estimated 38.3% as module and systems revenue, which carries higher average selling prices than discrete chips, grows as a share of the mix.

Twelve buys, three outperforms, one hold, and one underperform across 14 analysts point to a mean price target of $1,328.29, implying 24.3% upside from the March 20 close of $1,068.85, with consensus grounded in Enterprise Data re-acceleration to at least 50% growth and sustained automotive and storage momentum through 2026.

The $500 spread between the low analyst target of $1,000 and the high of $1,500 maps directly to two risks already in the story: the low reflects a scenario where the pending restatement of 2024 and 2025 financials, announced February 27, reveals a material earnings revision, while the high prices in full execution on the 50%-plus Enterprise Data growth floor CFO Blegen raised on February 5.

What Does the Valuation Model Say?

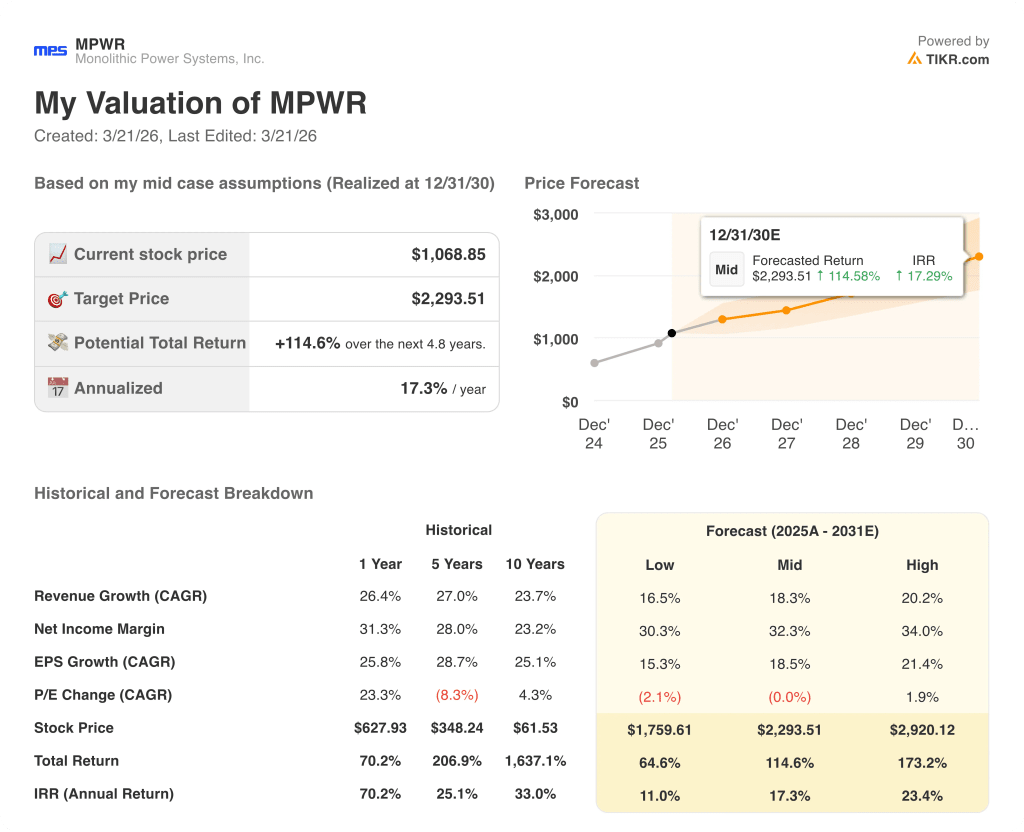

The TIKR mid-case target of $2,293.51, implying 114.6% total return over 4.8 years at a 17.3% annualized IRR, rests on an 18.3% revenue CAGR through 2030 and net income margins expanding from 30.8% in FY2025 to 32.3%, driven by the shift from selling individual power chips to higher-value modules and integrated systems that management has been executing since 2016.

The market prices MPWR at 55x forward earnings, but normalized EPS grows at an 18.5% CAGR through 2030, meaning the multiple compresses to roughly 23x on 2030 estimates without requiring any re-rating.

Design wins across hyperscalers, a backlog extending into Q3 2026, and $493.4 million in remaining buyback capacity collectively justify the TIKR target of $2,293.51 and the 18.3% revenue CAGR underpinning it.

CEO Michael Hsing stated on the February 5 earnings call that MPS holds design wins across all major hyperscalers simultaneously, a concentration of wins that analog peers have not publicly claimed at this scale.

The restatement of 2024 and 2025 financials, announced February 27 with no scope disclosed, breaks the TIKR model’s normalized EPS trajectory if it surfaces a revenue or margin restatement rather than a tax reclassification.

The Q1 2026 earnings call, expected in late April, confirms whether the $770 million to $790 million revenue guidance tracks and whether Enterprise Data growth is running at or above the 50% floor Blegen set on February 5.

Should You Invest in Monolithic Power Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MPWR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Monolithic Power Systems, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MPWR stock on TIKR for Free →