Key Stats for Micron Stock

- Past week’s performance: -4.3%

- 52-week range: $62 to $471

- Valuation model target price: $589

- Implied upside: 39.3% over 2.4 years

Value your favorite stocks like Micron with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Micron Technology (MU) stock fell 4.3% this week, even after the company reported strong earnings and raised guidance. The reaction reflects how much expectations had already moved higher going into the print. After a large run into earnings, the bar was elevated, so even strong results were not enough to push the stock higher.

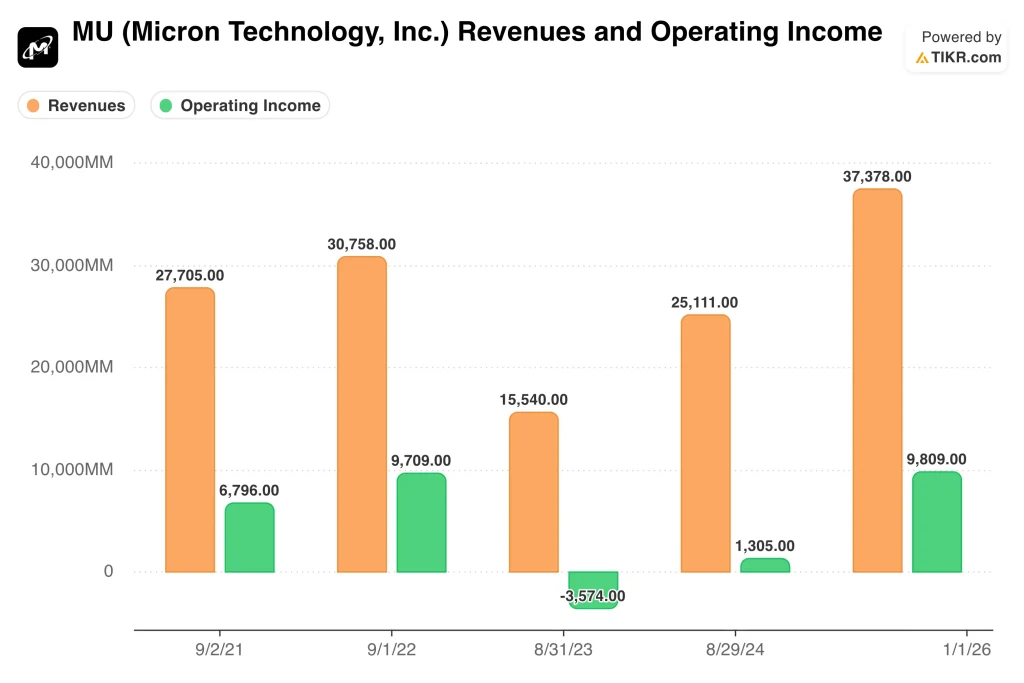

The company reported fiscal Q2 revenue of $23.86 billion and adjusted EPS of $12.20. Both came in well above expectations, and guidance also came in strong, with Q3 revenue expected to be around $33.5 billion. These results confirmed that demand tied to AI infrastructure continues to accelerate across the memory market.

That demand is being driven by data center buildouts and the increasing need for high-performance memory. DRAM and high-bandwidth memory remain the key products benefiting from this trend. As a result, Micron is seeing both stronger pricing and higher volumes, which is driving the sharp recovery in revenue and profitability.

However, the market focused on a different part of the story this week. Micron plans to increase fiscal 2026 capital expenditures by about $5 billion to more than $25 billion. That shift signals aggressive capacity expansion, and investors are now weighing how that additional supply could impact the cycle over time.

See analysts’ growth forecasts and price targets for Micron (It’s free) >>>

Is Micron Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 55%

- Operating margins: 85%

- Exit P/E multiple: 4.7x

Based on these inputs, the model estimates a target price of $589, implying 39.3% total upside from the current share price and a 14.5% annualized return over the next 2.4 years.

Business execution is the main driver behind those assumptions. Revenue has surged to about $58.1 billion over the last twelve months, which reflects a sharp recovery from the prior downcycle. The combination of higher demand and stronger pricing has driven one of the fastest growth periods Micron has seen in years.

Growth quality is closely tied to AI demand, especially in data center workloads. Memory is becoming a larger portion of total system cost, and that increases the value Micron can capture. As long as demand for AI infrastructure remains strong, revenue growth can stay elevated.

Margins are also a critical part of the story. Gross margins have expanded to about 58.4%, while operating margins have reached about 48.4%. That improvement reflects both pricing strength and a better mix of higher-value products, particularly high-bandwidth memory.

Capital intensity plays a key role as well. Micron is increasing spending to expand capacity, which is necessary to meet demand. However, this also introduces execution risk, because future supply growth needs to stay aligned with demand to maintain pricing power.

The balance sheet supports that strategy. The company is in a net cash position, which allows it to invest heavily while maintaining financial flexibility. That reduces risk compared to prior cycles where leverage was higher.

Valuation reflects both opportunity and expectations. The model assumes a lower exit multiple, which means the return profile depends more on sustained earnings growth. If margins and demand hold, the valuation can be supported, but any slowdown would matter.

What’s Driving the Stock Going Forward?

The next phase of the story depends on how supply and demand evolve. Management indicated that some customers are still not receiving full allocations, which shows supply remains constrained. That supports pricing in the near term and helps explain the current margin levels.

At the same time, Micron is entering a heavy investment phase. The company is expanding manufacturing capacity across multiple regions, including the U.S. and Taiwan. These investments are aimed at supporting long-term demand but will increase supply over time.

There is also a near-term catalyst with Micron being added to the S&P 100. That increases visibility and can drive incremental demand from institutional investors. While it does not change fundamentals, it reinforces Micron’s position as a major player in the semiconductor industry.

Broader semiconductor sentiment will also influence the stock. Micron has become closely tied to the AI narrative, so shifts in expectations around AI spending can drive volatility. This is especially true after a strong run, where positioning becomes more sensitive.

That is why the stock pulled back this week. The demand story remains strong, but investors are now focusing on sustainability. The next move will depend on whether Micron can continue converting AI demand into durable revenue growth and high margins.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Micron Technology, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Micron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Micron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Micron Technology stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!