Key Stats for Roper Stock

- Past-Week Performance: +0.8%

- 52-Week Range: $313.1 to $594.3

- Current Price: $353.7

What Happened?

Roper Technologies (ROP), a diversified vertical market software compounder generating $7.9 billion in 2025 revenue, is that its stock now trades at $353.68, a 40% discount to its 52-week high of $594.25, even as the company posted 12% revenue growth, $3.1 billion in EBITDA at 39.8% margins, and $2.5 billion in free cash flow representing 31% of revenue.

At the January 27 Q4 2025 earnings call, CEO Neil Hunn and CFO Jason Conley reported full-year adjusted diluted earnings per share of $20.00, up 9% and at the top of guidance, while initiating 2026 guidance for 5% to 6% organic revenue growth and adjusted DEPS of $21.30 to $21.55, despite absorbing headwinds from three specific businesses: Deltek, its government contractor ERP software unit hit by DOGE disruptions and a federal shutdown; Neptune, its water meter hardware business squeezed by tariff-related surcharges; and Procare Solutions, its early childhood education software platform where implementation delays depressed payments revenue.

Beneath those three drags, Roper’s 21 vertical market software businesses delivered enterprise software bookings growth in the low double digits for the full year, with Application Software organic recurring revenue rising 7% and gross retention holding in the mid-90s, while CentralReach, its recently acquired autism therapy practice management software, accelerated from low-20s to high-20s revenue growth after deploying AI scheduling and billing tools that drove therapist attrition down from 85% to 40%.

Conley also stated at the Q4 2025 earnings call that “the companies that are farthest along in AI are growing the fastest in our portfolio,” directly referencing CentralReach’s win rate against its primary competitor rising from 75% to 100% in the second half of 2025.

Roper’s $6 billion-plus capital deployment capacity, a $2.5 billion remaining buyback authorization, and the second-half 2026 organic contribution from both CentralReach and Subsplash, its church management software platform, turning organic position the company to compound free cash flow per share at a mid-to-high-teens rate as AI monetization across 21 software businesses moves from product development in 2025 to commercialization in 2026.

Wall Street’s Take on ROP Stock

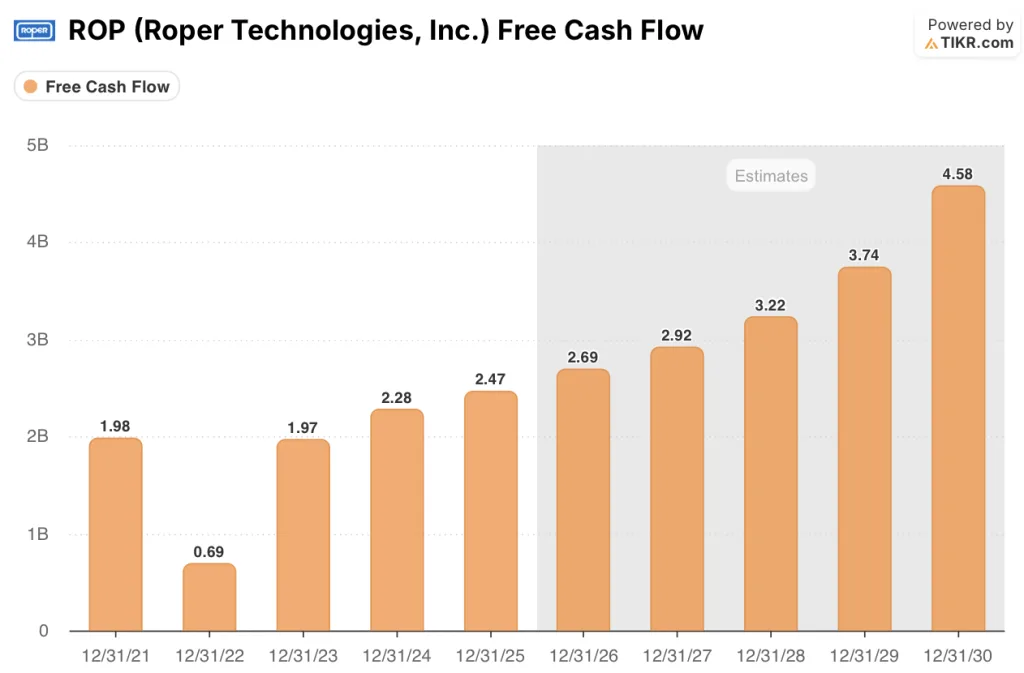

The valuation dislocation in Roper’s stock, which now trades at $353.68 despite generating $2.47 billion in free cash flow in 2025, directly sets up a 2026 rerating as three temporary headwinds, Deltek, Neptune, and Procare, begin to normalize against a durable 31%-plus free cash flow margin base.

TIKR estimates ROP’s project free cash flow rising from $2.47 billion in 2025 to $2.69 billion in 2026 and $2.92 billion in 2027, supported by CentralReach and Subsplash turning organic in the second half of 2026 and adding incremental recurring revenue to a portfolio already holding mid-90s gross retention.

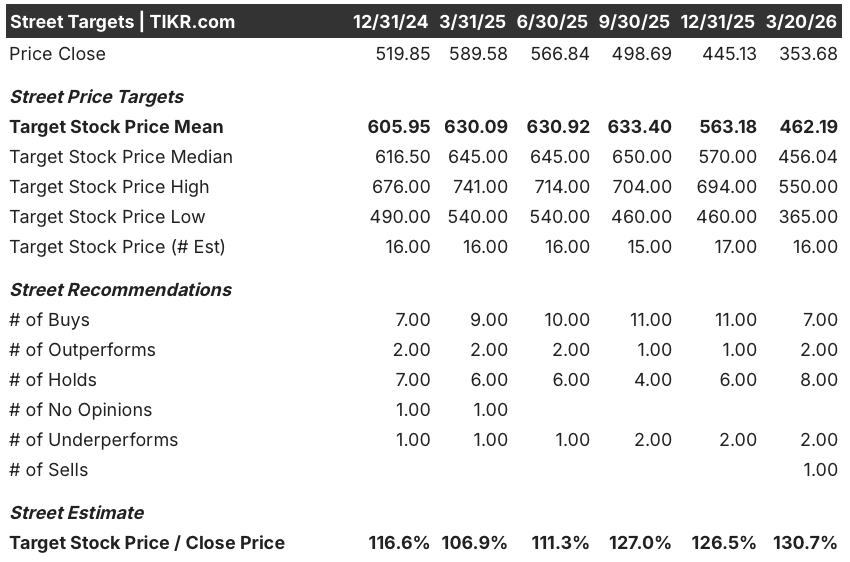

Moreover, fourteen of 19 analysts with active coverage rate ROP a buy or outperform, with a mean price target of $462.19 implying 30.7% upside from current levels, a spread that reflects Street conviction in the free cash flow compounding thesis even as the stock sits 40% below its 52-week high.

The gap between the $365.00 low target and $550.00 high target captures the binary at the core of this story: bears anchor to a prolonged Deltek GovCon freeze and continued Neptune volume weakness, while bulls price in the $6 billion-plus capital deployment capacity and second-half 2026 organic acceleration.

What Does the Valuation Model Say?

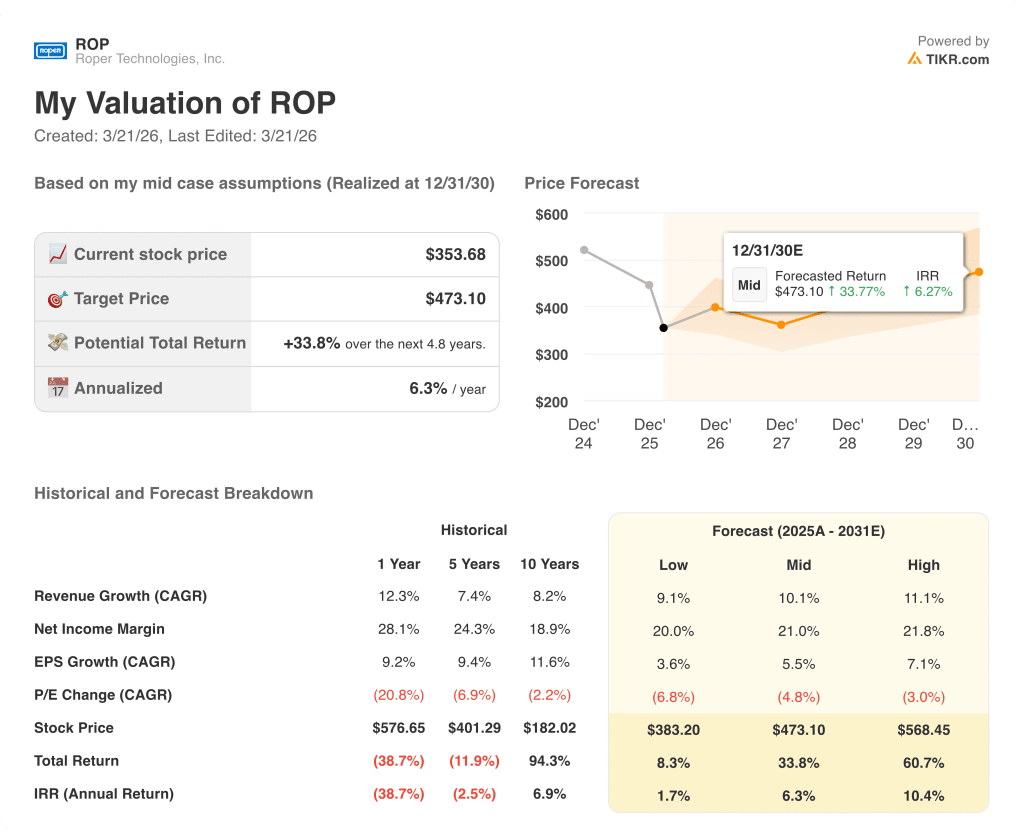

The TIKR mid-case model prices ROP at $473.10 by December 2030, assuming 10.1% revenue CAGR and 21.0% net income margins, both grounded in the combination of recurring software bookings growing low double digits in 2025 and AI monetization across 21 vertical businesses scaling through commercialization in 2026.

The market is treating three known, management-acknowledged headwinds as permanent impairments, but $2.47 billion in 2025 free cash flow at a 31.2% margin says otherwise.

Enterprise software bookings growing low double digits in 2025, with gross retention in the mid-90s and CentralReach already ahead of its deal model, directly supports the TIKR model’s 10.1% revenue CAGR; the mid-case price target of $473.10 reflects a business compounding steadily, not inflecting dramatically.

Management’s deployment of $1.8 billion in buybacks over five months at prices well above current levels signals that Roper’s own capital allocation team views $353.68 as a mispriced entry point, not a fair valuation.

If Deltek’s GovCon pipeline, which management described as encouraging despite slow signatures, fails to convert perpetual license deals in the first half, the TIKR model’s 5% to 6% organic growth assumption breaks, and the $473.10 target compresses toward the $383.20 low case.

Roper’s Q1 2026 earnings report is the first confirmation point: watch adjusted DEPS against the $4.95 to $5.00 guidance range and Application Software organic growth for evidence that the nonrecurring headwind is stabilizing as management projected.

Should You Invest in Roper Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ROP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Roper Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ROP stock on TIKR for Free →