Key Stats for HIMS Stock

- Past week’s performance: -11.5%

- 52-week range: $14 to $70

- Valuation model target price: $39

- Implied upside: 77.3% over 2.8 years

Value your favorite stocks like HIMS with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Hims & Hers Health (HIMS) stock fell 11.5% this week and closed at $22.02 on March 20. The pullback came after a volatile March, when the stock first surged on its Novo Nordisk deal and then gave back some of those gains. That pattern suggests investors are still weighing the value of broader access to branded GLP-1 drugs against a lower-margin mix and fresh regulatory scrutiny.

The biggest positive catalyst came on March 9, when Novo Nordisk said Hims would sell FDA-approved Wegovy and Ozempic on its platform and that Novo would drop its lawsuit. The stock jumped sharply on that news because the deal ended a legal dispute and expanded Hims’ access to branded obesity drugs. But analysts also expected branded GLP-1 sales to carry lower margins than compounded offerings, which helps explain why the early rally did not fully hold.

The tone then turned more mixed. On March 12, Eli Lilly warned about an impurity it found in certain compounded tirzepatide products, and that kept investor attention on safety and compliance across the compounded weight-loss market. Hims then said on March 18 that it would expand its platform to include Wegovy pills and injections and Ozempic injections, but that update did not fully offset the market’s concerns about how the GLP-1 transition could affect margins and demand mix.

The background to all of this is that Hims has become one of the market’s most visible consumer health platforms tied to the GLP-1 trade. The FDA warned telehealth firms in early March over misleading marketing of compounded GLP-1 drugs, and Hims had already been in the spotlight after its low-cost semaglutide pill launch and later retreat in February. So this week’s move looks less like a change in growth potential and more like investors repricing regulatory risk, product mix, and near-term margin expectations.

See analysts’ growth forecasts and price targets for HIMS (It’s free) >>>

Is HIMS Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 15.6%

- Operating Margins: 6.8%

- Exit P/E Multiple: 19.5x

Based on these inputs, the model estimates a target price of $39.05, implying 77.3% total upside from the current share price and a 22.8% annualized return over the next 2.8 years.

The valuation setup is more conservative than recent trading levels. The model assumes 15.6% revenue growth, 6.8% operating margins, and a 19.5x exit P/E, which is below the stock’s 1-year historical P/E of 37.1x shown in the valuation image. This means the implied upside does not depend on multiple expansions and instead relies more on continued execution.

The business has already transitioned into profitability. LTM revenue stands at $2.35 billion, with gross margins of 73.8% and EBIT margins of 5.2%, while fourth-quarter results showed $617.8 million in revenue and $66.3 million in adjusted EBITDA. The key question now is whether the company can maintain growth while shifting toward more regulated and potentially lower-margin products.

Management continues to emphasize scale and platform expansion. The company has highlighted that more than 2.5 million subscribers are on its platform and that it is expanding across additional conditions and geographies. That strategy supports long-term growth but may require continued investment.

What’s Driving the Stock Going Forward?

The next phase for Hims will depend on how effectively it transitions its weight-loss offering toward FDA-approved drugs. The company has indicated it will expand access to approved medications while limiting compounded semaglutide to specific clinical cases. This shift could reduce regulatory pressure but may also compress margins.

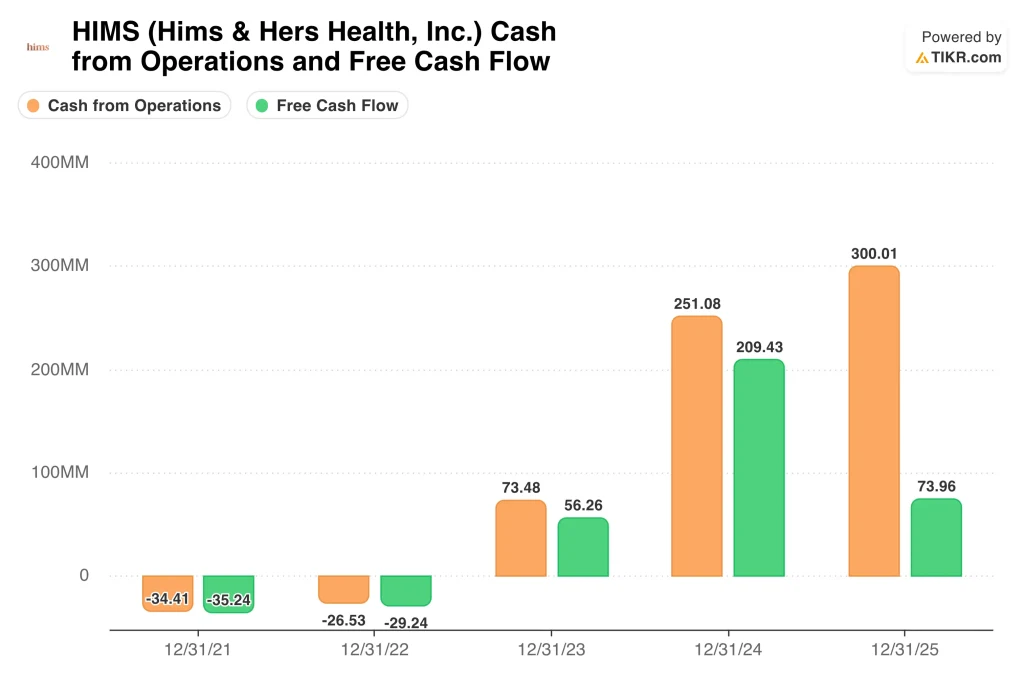

Cash flow and capital allocation are also important. The company generated $300.0 million in operating cash flow in 2025, but free cash flow declined to $74.0 million due to higher capital expenditures and acquisitions. At the same time, total debt increased to about $1.1 billion, with net debt at approximately $543.1 million, marking a shift from a prior net cash position.

Expansion beyond the U.S. remains another key driver. The planned acquisition of Eucalyptus, valued at up to $1.15 billion, highlights the company’s push into international markets. Recent results also showed strong growth in rest-of-world revenue, indicating early traction outside its core market.

The next major catalyst is the Q1 2026 earnings report expected on May 4. Investors will likely focus on revenue growth, adjusted EBITDA, subscriber trends, and commentary around GLP-1 demand, product mix, and regulatory developments. Until then, the stock is likely to remain sensitive to headlines tied to obesity drugs and telehealth regulation.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Hims & Hers Health, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HIMS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HIMS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Hims & Hers Health stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!