Lam Research Corporation (NASDAQ: LRCX) has surged over the past year, gaining more than 100% as AI-driven chip demand reignites confidence in semiconductor equipment makers. Shares now trade near $161, close to record highs, raising the question of whether there is still room for upside.

Recently, Lam reported strong quarterly results supported by continued strength in logic and foundry spending, as chipmakers ramp up investments in AI and advanced process nodes. The company also introduced its new Sense.i Pro etch platform, designed to improve wafer precision and energy efficiency, a key innovation as the industry transitions to next-generation 3D architectures. These updates show Lam’s technology leadership remains intact even in a highly competitive landscape.

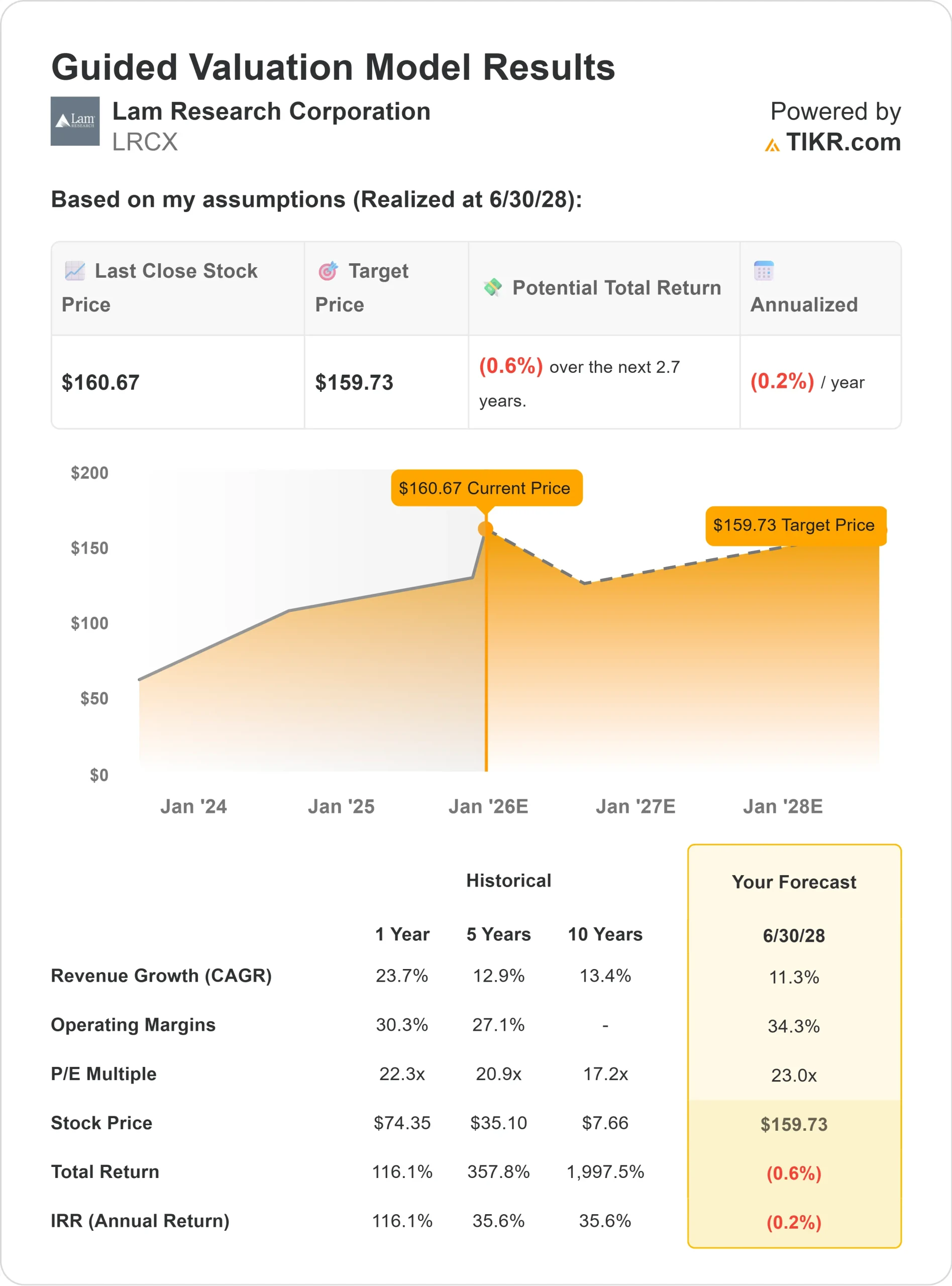

This article looks at what analysts expect for Lam by 2028 using TIKR’s Guided Valuation Model and consensus price targets. These figures reflect analyst estimates, not TIKR’s own forecasts.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest the Stock Is Fairly Valued

Lam Research trades near $161/share today. The average analyst price target is $158/share, which implies roughly 1% downside from current levels.

Forecast range:

- High estimate: ~$200/share

- Low estimate: ~$84/share

- Median target: ~$165/share

- Ratings: 21 Buys, 2 Outperforms, 10 Holds, 2 Sells

It looks like analysts see Lam as fairly valued after its strong rally. For investors, The current price already reflects optimism around AI and semiconductor growth. Unless a new wave of capital spending or stronger-than-expected chip demand emerges, Lam is likely to deliver steady rather than outsized returns from here.

Lam Research Analyst Price Target

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Lam Research: Growth Outlook and Valuation

Lam’s fundamentals remain strong and consistent:

- Revenue is expected to grow about 11% annually through 2028

- Operating margins should hold near 34%

- Shares trade around 23x forward earnings, roughly in line with historical averages

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23x forward P/E suggests ~$160/share by mid-2028

- That implies roughly flat total returns of about (0.6%) over the next few years

These projections indicate Lam can compound steadily, but major upside may already be priced in. For investors, Lam looks like a quality long-term hold with stable earnings power, though big gains will depend on another round of strong chip demand and AI infrastructure spending.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Lam’s expertise in wafer fabrication tools puts it at the center of the AI and data center expansion cycle. Strong demand from foundries and memory makers continues to support orders, and new etch and deposition platforms are helping the company capture more share in advanced chip processes.

For investors, These strengths suggest Lam is well positioned for structural semiconductor growth. If AI and memory spending stay robust, Lam could deliver more consistent returns than the broader equipment sector.

Bear Case: Cycles and Valuation Pressure

Even with these positives, Lam remains tied to the semiconductor cycle. A slowdown in wafer-fab equipment spending, export restrictions to China, or softer foundry investment could weigh on results. Some analysts note that parts of Lam’s recent growth may have been pulled forward from future years.

Valuation is another concern. With much of the optimism already reflected in the share price, any cooling in demand could cap returns. For investors, Lam is a high-quality company, but without a new upcycle, near-term upside appears limited.

Outlook for 2028: What Could Lam Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23x forward P/E suggests Lam could trade near $160/share by mid-2028.

Given today’s price of $161/share, that implies essentially flat potential upside (around 0%) over the next few years unless capital spending accelerates beyond current forecasts.

For investors, Lam looks like a stable hold with strong profitability and durable advantages, but not a high-flyer from here. To unlock meaningful upside, the company would need a fresh burst of demand such as a memory-capex ramp or broader foundry expansion.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>