General Motors Company (NYSE: GM) has staged a strong recovery over the past year. The stock trades near $69/share, up sharply from around $45/share a year ago, reflecting optimism around cost discipline, steady truck demand, and improving margins. While the auto market remains competitive, GM’s execution in its core business and disciplined capital strategy have helped rebuild investor confidence.

Recently, GM reported stronger-than-expected third-quarter results, driven by solid performance in its truck and SUV lineup. The company raised its full-year earnings guidance as cost controls and resilient demand in North America supported profitability. However, its electric vehicle rollout remains behind schedule, with management acknowledging slower production ramp-up on the Ultium platform. Even so, GM reiterated its long-term EV goals and continued investing in battery and software development. The company also expanded its share repurchase program, reflecting confidence in its strong balance sheet and consistent cash flow generation.

This article explores where Wall Street analysts think GM could trade by 2027. We have compiled consensus targets and valuation models from TIKR to outline the company’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Limited Upside

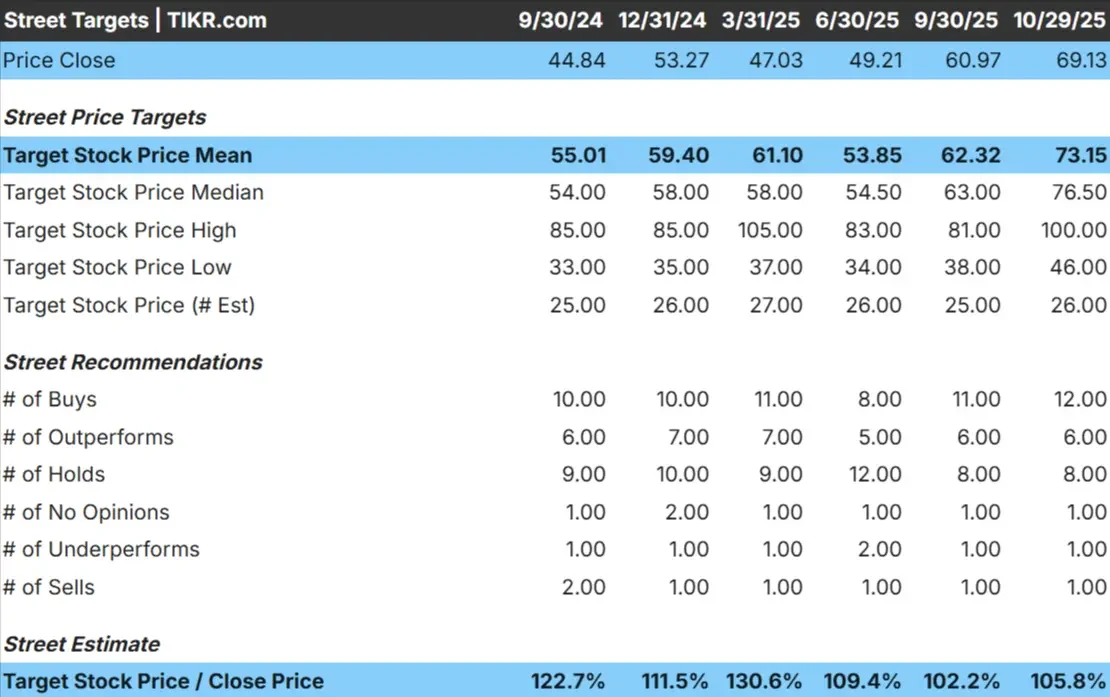

GM trades at about $69/share today. The average analyst price target is $73/share, which points to roughly 6% upside over the next 12 months. Forecasts show a modest range:

- High estimate: ~$100/share

- Low estimate: ~$46/share

- Median target: ~$77/share

- Ratings: 12 Buys, 6 Outperforms, 8 Holds, 1 Underperform, 1 Sell

Analysts see limited upside from here, suggesting most of the recovery story is already priced in. The spread between bullish and bearish estimates remains wide, reflecting uncertainty about GM’s ability to sustain profit growth as the EV market evolves. While cash generation and cost discipline are solid positives, further gains may depend on whether management can turn its EV investments into real earnings power over the next two years.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

GM: Growth Outlook and Valuation

GM’s fundamentals look steady but lack strong growth catalysts:

- Revenue is expected to remain roughly flat through 2027

- Operating margins are projected near 7%

- Shares trade around 15x forward earnings, close to historical averages

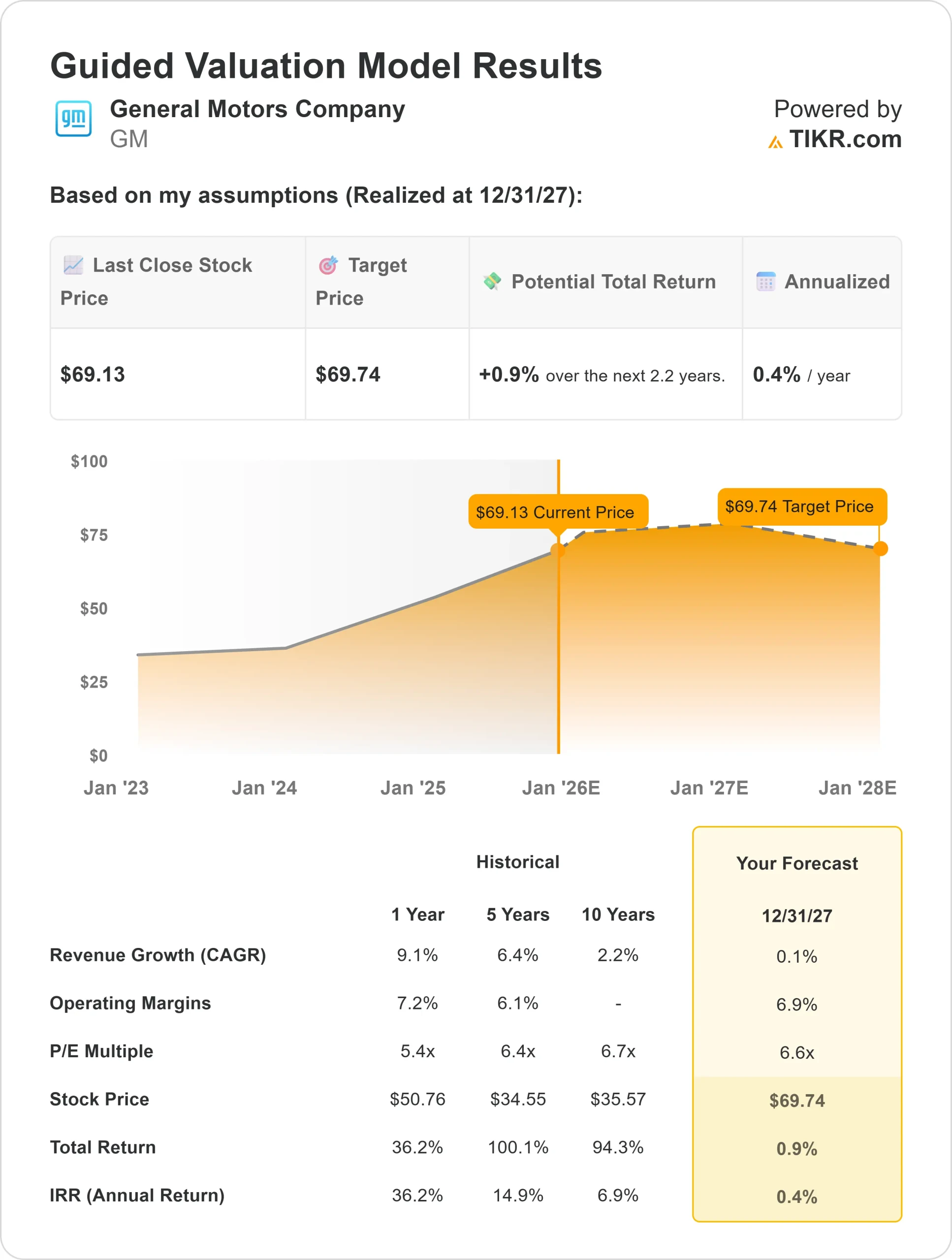

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 6.6x forward P/E suggests the stock could trade near $70/share by 2027

- That implies about 1% upside, or roughly 0.4% annualized returns

These estimates imply that GM is fairly valued at current levels. Strong operational execution and shareholder returns have supported the stock, but multiple expansion looks unlikely without a clearer path to earnings growth.

For investors, GM represents a dependable industrial name built on stable margins and strong cash flow. However, meaningful upside may only come if its EV transition gains momentum faster than analysts expect.

General Motors Guided Valuation Model Results

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

GM’s strong position in North America continues to anchor its profitability. Demand for high-margin trucks and SUVs remains resilient, while improved pricing discipline has supported steady margins despite softer unit volumes. The company’s cost controls, particularly around manufacturing efficiency and supply chain management, have helped stabilize earnings even through a slower auto cycle.

Management’s renewed focus on capital returns also stands out. GM recently resumed share buybacks and maintained a healthy dividend, signaling confidence in future cash flow. Meanwhile, production of Ultium-based electric vehicles is scaling up faster than expected, and new launches like the Chevrolet Equinox EV and Silverado EV could broaden the company’s reach in mass-market electrification.

For investors, these strengths suggest GM is executing well within a challenging environment. The balance between cost discipline, shareholder returns, and long-term EV strategy gives the company a credible foundation for steady performance through 2027.

Bear Case: Slow Growth and EV Uncertainty

Even with these positives, GM’s growth story still faces real challenges. Revenue trends have flattened, and the broader auto industry is becoming more competitive as legacy automakers and startups race for EV market share. If electric vehicle demand slows or battery costs remain elevated, margin expansion could prove difficult.

GM’s valuation also reflects a fair amount of optimism already. With the stock trading near its estimated fair value, investors may see limited upside unless earnings growth surprises to the upside. Rising interest rates and potential pricing pressure in the truck segment could further limit progress.

For investors, the main risk is that GM’s EV transition takes longer or proves less profitable than expected. Without a clear acceleration in revenue or margin growth, the stock could remain rangebound in the near term.

Outlook for 2027: What Could GM Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 6.6x forward P/E suggests GM could trade near $70/share by 2027. That implies around 1% upside from today’s price, or roughly 0.4% annualized returns.

While this projection highlights stability, it also shows how much of GM’s rebound has already been priced in. To unlock stronger gains, GM would need to deliver consistent EV volume growth and demonstrate that its electrification investments can sustain profitability without eroding its core business margins.

For investors, GM looks like a steady value play built on strong cash flow and disciplined execution. The path to outsized returns, however, depends on management proving that its EV strategy can translate into real long-term earnings growth.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>