Aviva plc (AV.) posted another strong performance in the first half of 2025, marking continued progress in its turnaround. Operating profit rose 22% year-over-year to £1.07 billion, while IFRS profit climbed 25% to £819 million. Solvency II cover strengthened to 206%, reflecting robust capital generation and disciplined execution. With two-thirds of profit now coming from “capital-light” businesses, Aviva’s model is shifting toward more stable and higher-return operations as it integrates its latest acquisition, Direct Line Group.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)

Growth was broad-based across Aviva’s business lines. General insurance premiums rose 7% to £6.29 billion, while Wealth and Retirement sales climbed 9% to £21.5 billion. The Health segment also delivered strong results with in-force premiums up 14% to £1 billion. Management raised the interim dividend 10% to 13.1 pence per share, the tenth straight annual increase, underscoring confidence in the outlook. CEO Amanda Blanc says Aviva remains on track to reach £2 billion in operating profit by 2026, targeting cumulative cash remittances of more than £5.8 billion over 2024-2026.

After years of restructuring, Aviva now operates as a streamlined, diversified insurer focused on the UK, Ireland, and Canada. The addition of Direct Line, completed in July 2025, adds over four million new customers and strengthens Aviva’s presence in UK motor and home insurance. Integration is underway, and investors are watching closely for cost synergies and execution risk as the company works toward its next phase of profitable growth.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

The first half of 2025 demonstrated steady progress toward Aviva’s capital and earnings targets. Solvency II operating own funds generation rose 20% to £909 million, while IFRS return on equity climbed to 20.6% from 14.8% a year earlier. Cash remittances totaled £1.02 billion, up 7%, underlining the group’s balance sheet strength and cash conversion capacity. These results came despite continued pricing competition in UK motor insurance and softer new business volumes in bulk purchase annuities, both of which management addressed through disciplined pricing and capital allocation.

| Metric | H1 2025 | YoY Change | H1 2024 |

|---|---|---|---|

| Operating Profit | £1.07B | +22% | £875M |

| IFRS Profit | £819M | +25% | £654M |

| Solvency II Cover Ratio | 206% | +3 pp | 203% |

| Cash Remittances | £1.02B | +7% | £959M |

| General Insurance Premiums | £6.29B | +7% | £6.01B |

| Wealth & Retirement Sales | £21.5B | +9% | £19.7B |

| Interim Dividend | 13.1p | +10% | 11.9p |

Regionally, UK and Ireland general insurance premiums grew 9% to £4.14 billion, aided by strong commercial lines pricing and growth through intermediary channels like Aviva’s travel partnership with Nationwide. Canadian general insurance premiums increased 4% to £2.14 billion, reflecting robust demand in personal lines. Meanwhile, wealth net flows of £5.8 billion, equivalent to 16% year-over-year growth, underscored the resilience of Aviva’s long-term investment platform. Across all divisions, cost discipline and portfolio simplification supported profit expansion, helping offset short-term headwinds from inflation-linked claims costs.

The Direct Line acquisition adds both scale and complexity. Aviva plans to extract £100 million in annual run-rate profit synergies by 2026, supported by pricing efficiencies and technology consolidation. Management says integration is progressing smoothly, with no disruption to Direct Line’s core underwriting performance.

Motor policies rose 6% year-over-year to 3.7 million, and non-motor policies remained stable at 4.9 million. While the deal’s financial benefits won’t fully materialize until late 2026, it positions Aviva to capture a greater share in the UK’s £23 billion general insurance market and to deepen customer relationships across multiple product lines.

Look up Aviva’s full financial results & estimates (It’s free) >>>

1. Capital-Light Growth Strategy Gains Momentum

Aviva’s long-term shift toward capital-light businesses, including wealth, health, and protection, continues to deliver measurable returns. Two-thirds of group operating profit now originates from these segments, up from just half five years ago. This capital-light mix improves free cash generation and supports sustainable dividend growth, allowing Aviva to target cumulative cash remittances of over £5.8 billion through 2026. The strategy also cushions against capital volatility in annuities and bulk purchase agreements, giving Aviva more flexibility to reinvest in technology and growth.

At the same time, the company is maintaining discipline in underwriting-heavy segments, such as general insurance and bulk annuities, where pricing headwinds have intensified. While some analysts see risk of margin compression in the UK auto market, management’s focus on underwriting profitability, not volume, is paying off. The group’s combined operating ratio improved by 80 basis points year over year to 94.6%, signaling better risk selection and cost control.

2. Direct Line Integration: Strategic Upside with Execution Risks

The Direct Line acquisition, completed in July 2025, represents Aviva’s largest deal in a decade and one of the most transformative moves in the UK insurance landscape. The acquisition gives Aviva a market-leading position in UK motor and home insurance, alongside valuable brand equity and customer data. Integration efforts are progressing at speed, and early signs suggest minimal operational disruption. Direct Line’s net insurance margin improved 7.6 points to 9.4%, reflecting more disciplined pricing and expense control.

However, integration risk remains a key consideration. Aviva must align underwriting systems, distribution channels, and IT infrastructure across both entities while ensuring regulatory compliance and customer retention. CEO Amanda Blanc has emphasized that the deal’s full financial benefits, particularly £100 million in annual synergies, will be realized gradually, with meaningful uplift expected by late 2026. If successful, the combination could meaningfully expand Aviva’s scale and accelerate its capital-light trajectory.

Value stocks like Aviva in less than 60 seconds with TIKR (It’s free) >>>

3. Profitability and Outlook: Confidence Meets Execution Challenge

Aviva’s guidance to deliver £2 billion in operating profit by 2026 is ambitious but increasingly credible. The company’s return on equity has already surpassed 20%, and its capital position remains robust with a Solvency II cover ratio of 206%. Management’s focus on balancing growth with risk control is encouraging, particularly amid inflationary pressures on claims costs and volatile reinsurance markets. With strong momentum in wealth and health insurance and continued expansion in digital distribution, Aviva appears well-positioned to sustain mid-to-high single-digit earnings growth through 2026.

Still, investors will want to see progress in efficiency and cost reduction. The integration of Direct Line could create short-term expense pressure, and rising competition in UK insurance markets may limit margin expansion. Yet Aviva’s track record of delivering consistent profit growth and maintaining balance sheet strength offers reassurance. As Blanc put it, “Our ambition for the future remains undiminished, if anything, it has only grown stronger.”

The TIKR Takeaway

Aviva’s 2025 results reinforce the insurer’s comeback story. The group is executing on its capital-light strategy, maintaining healthy cash generation, and strengthening profitability across all major divisions. The Direct Line acquisition introduces short-term integration risk but offers long-term scale and cost synergies that could accelerate cash flow growth through 2026. With dividends rising and returns improving, Aviva is cementing its reputation as one of the UK’s most dependable financials.

For investors, the key question is not whether Aviva can maintain momentum, but how efficiently it can translate this growth into sustainable shareholder returns while absorbing the complexity of its new business mix.

Should You Buy, Sell, or Hold Aviva Stock in 2025?

Aviva’s solid 2025 performance, improving cash remittances, and attractive dividend trajectory make it a compelling long-term holding for income-focused investors. The £2 billion profit target for 2026 appears achievable if integration proceeds smoothly and market conditions remain stable. While short-term volatility is likely as Direct Line is absorbed, Aviva’s diversified model and disciplined execution support a bullish outlook, particularly for investors seeking steady compounding in the UK financial sector.

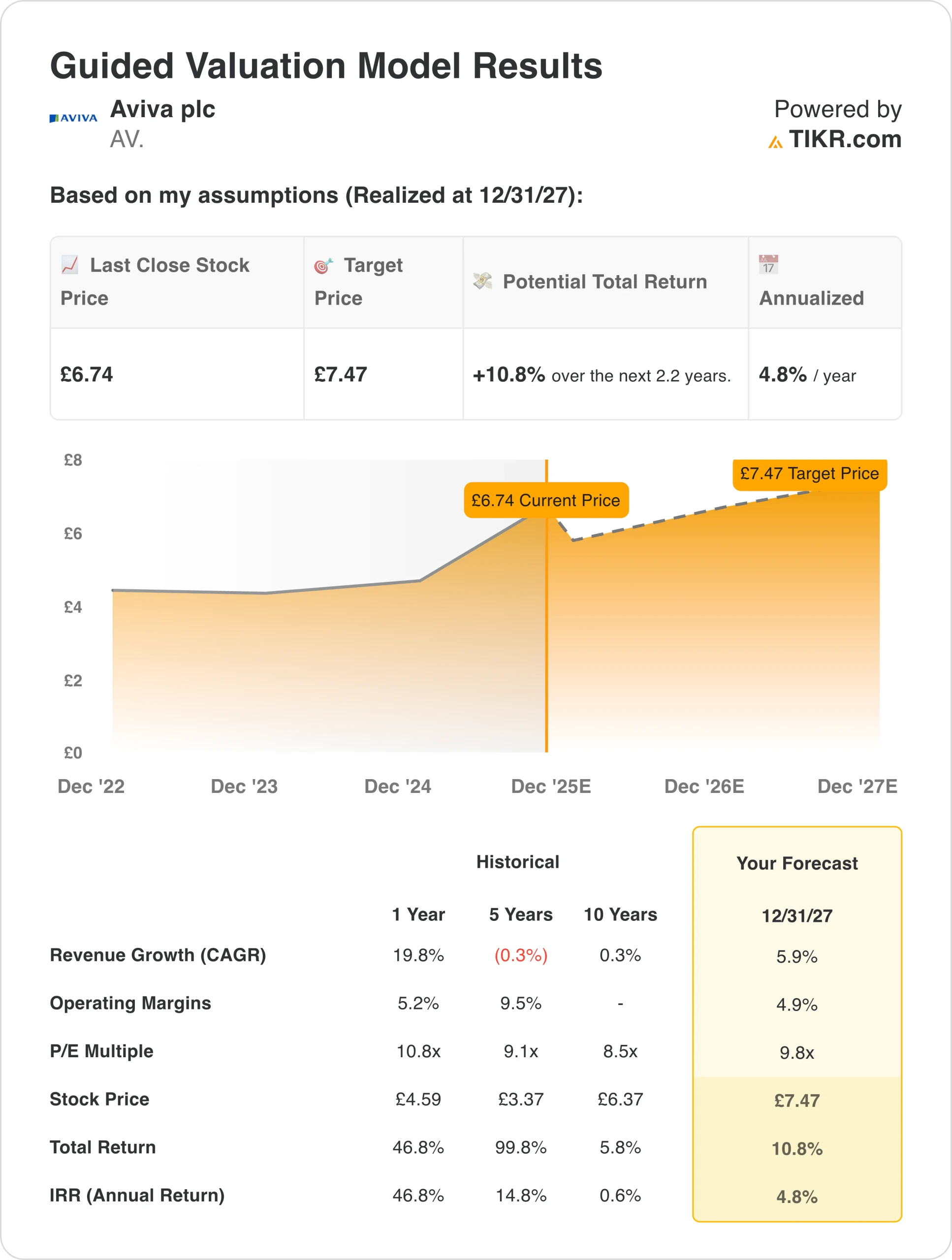

How Much Upside Does Aviva Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!